Lifestyle Inflation and High Cost of Living Explained

Level 2- NGMI

Welcome Avatar! You spent your time going to a Top University and think that $100,000+ a year is “balling”. This is a common belief amongst young people and frankly, don’t blame them. When you go from $2-3 shots at dive bars and getting plastered off of alcohol in a plastic bottle, this is a huge upgrade.

You can actually afford to live like a normal person!

The problem? Life costs escalate! Unless you plan on becoming a strange frugal person (See FIRE which doesn’t work well), the reality is that you’ll run the math and see how this happens in real time.

Once again, we assume you don’t have family money. If you’re from a rich family with $5-10M already… You don’t really have any risk in the first place.

Part 1: Realization Phase

After blowing through your sign on bonus and having fun, you will begin to realize how expensive life is when you get your first apartment/studio/condo rental. Even if you live with roommates you realize that the living situation immediately eats into your savings.

Note: While remote work lasted for a bit, the reality is still the same. The VAST majority of high paying careers are in high cost of living cities. If you’re the exception to the rule that is *fantastic*. It doesn’t change the reality for the majority (call it 80%+). Also. The hint here is that you should take those high paying careers in lower COL areas if you want to save/invest more.

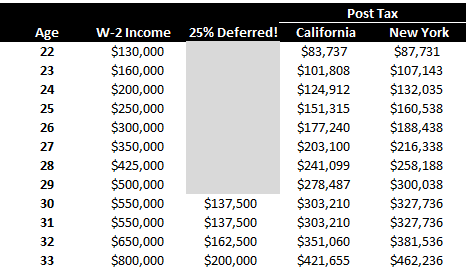

Quick Math First 1-3 years: If you work in investment banking, software, or tech sales you can probably assume you’ll make around $130,000 then $160,000 and $200,000. This is nothing to scoff at and certainly you can do better/worse than this.

The reason we’re keeping it simple is because it doesn’t matter. As you’ll see below the dollar amount you can put away is quite low.

Quick Math Year 4-7: We assume you don’t get laid off. At this point the incremental *percentage* change in income begins to decline. You get $250,000 then $300,000 then $350,000 then the bigger move to say $425,000. While these are $50,000-75,000 hikes, the percent move from $250 to $350K is not the same percent move.

Note: assumes no MBA no masters degree and no PHD!

Perfect Worker Year 8-12: Now you’re going to compete extremely hard for every penny put into your coffers. We’ll say you do *well* but you have a SINGLE flat year. For those that think flat years are impossible, go ask your local investment banking colleague about their year-end bonus in 2023 (hint it’ll be down big on *average*). 8) $500,000, 9) $550,000, 10) $550,000, 11) $650,000 and 12) $800,000.

You can see all these numbers below:

Hmm this all looks great! However. We haven’t even touched the cost side yet. Don’t get it twisted. If you could somehow save all of it since you’re from a rich family you’re set. Impossible game to lose unless you suffer from some sort of addiction.

Basic Housing: In NYC, the Median rent is around $4,000 to $5,000. To make this a fair competition we’ll say you’re willing to live with roommates for about 3 years. We’ll call it $2,500 a month. That is an average for 3 years. California and New York are where the majority of high paying jobs are (again if you’re in a low COL area you do much better if you can survive)

Annual Vacation: If you’re working 60+ hours a week… You’re not going to stay in the city for your 1-week or 2-week vacation. To keep it simple we’ll say you spend about $5,000 on an annual vacation to avoid going crazy. The length isn’t relevant. If you leave for 2-weeks you can go to a cheap location on $5,000 or you can go to a more expensive area for less time.

Food Expense: A good simple estimate is about half of what you spend on rent. Slightly more since you live in a high cost of living area. $1,500/month.

Regular Social Life: Since you don’t plan on being one of the frugal strange guys with no life experiences. Tack on about $750 a month just for going out. This will include drinks, dinners etc.

Other: Cell phones, dry cleaning, laundry, internet etc. Just add $500.

Here is what you get.

Hmm not looking too great. But… you’ll make up for it in years 4-8! So… you think!

Part 2: Alarm Bells Go Off

At this point, the people who made it by following the plan (high paying career → WiFi → Quit when 2x earnings —> Invest) have their lightbulb moment.

At age 26, it becomes a bit strange telling people “I live at home with my parents/roommates”. In other words, you’re starting to look incongruent. This is no different than the guy who is still going to clubs at age 38. Just looks terrible.

You can try to push it but being realistic, you will also realize how annoying it is to live like that.

You only make two changes: 1) you live by yourself and 2) you upgrade your food and social costs because you just don’t enjoy eating lower quality stuff.

Rent Goes to $4,000 and Food/Social go to $2,000 and $1,417 a month (Used a strange number to solve for $100K as that is about right)

Okay how are you doing so far? We can check in on how much you’re really saving/investing.

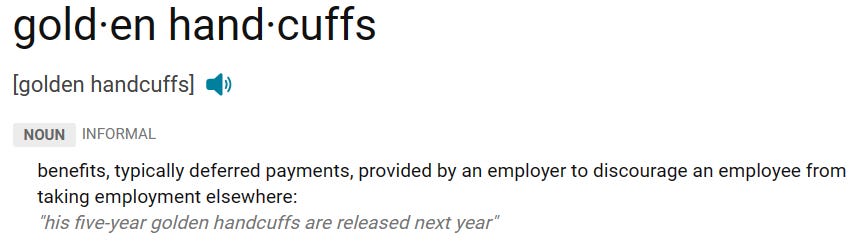

“Woah!”: Most stop here and say wow, with perfect savings and no down investment years you can be in the high-6 figures. The problem? You are officially near the cuffs.

Part 3: The Deferred Stock, Mortgage and More!

At this point you’re entering your 30s. Yes, we realize many people don’t want kids. We realize that many people want to party forever. Reality though is the following issues begin to arise: 1) your ability to go out starts to decline by 30 and certainly by 35+ you shouldn’t be hitting clubs getting blacked out, 2) you’re going to get tired of living in that studio or one bedroom apartment and 3) the vast majority settle down.

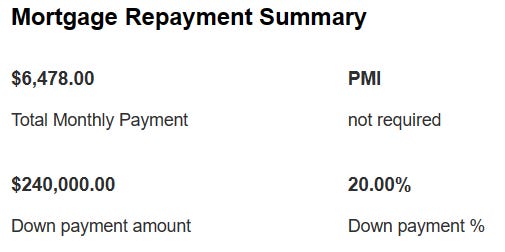

Only Three Changes: 1) we assume you buy a place worth $1.2M, 2) we assume your vacation cost goes to $12,000 a year and 3) *Surprise* we assume all your regular costs go up by 20% since we’ve assumed zero inflation for a decade.

Hint! The $240,000 has to come out of your savings/investing! So, we remove that.

How Does this Look at Age 33? Well, here you go.

Ruh Roh!

Part 4: Gotcha Cuffed.

You are now in your mid-30s. We’ve assumed you did not live a crazy life. You lived with roommates. You then took $5K vacations and then $10K+ vacations a *decade* later. We did not include any of the following: 1) furniture all free, 2) appliances all free, 3) no car/transportation cost, 4) you never get laid off, 5) you never have a bad investment year and 6) you never go entirely crazy and make even one financial mistake.

While $4K on social + food sounds like a lot to people *outside* of major cities. This is easily the case as a dinner will run you $200+ for two people. In the end an extra $25K on $1M is only 2.5% anyway. You don’t get “rich”

Deferred Compensation: Your boss does not want to lose a top employee. Therefore, they start deferring your compensation. Before people say we should count it as income we simply leave it aside. This is because you might work at Lehman or Credit Suisse. You also might work at the next Tesla. Who knows. All you really know is that deferred money is *not* in your bank account and typically has a 4 year vesting period.

Part 5: “Living the Dream”

This is a tongue in cheek expression on Wall Street. This is because it’s a way of outwardly admitting you didn’t expect to be in this position.

No, you’re not struggling. No, you’re not well “respected” either.

In fact, no one really cares that you’re worth a million bucks and are in your mid 30s. You will find that this is quite common amongst a wide array of high paying positions.

The problem is this. How do you expect to catch up to the top 1% wealth when they make more than $400,000 on dividends/interest alone (top 1% wealth is $10M earning 4-5% in bonds/dividends = $400,000-$500,000.

Now that you’ve seen the math you can decide if this is glamorous or not. Life is a lot more expensive than most think especially if you plan on living in major cities. If you get laid off at any point, the $6,478 mortgage is not going to pay for itself. Also. As mentioned, the vast majority end up having kids or having more severe lifestyle inflation (assumed no clothing purchases and no furniture somehow).

Business: Living the Dream")

You decide!

Autist Note: For those that are young, we believed the same thing! $100K was “set for life”. How wrong that thinking was. In the end though, by the time you’re 25 you’ll see reality for what it is. Microsoft excel doesn’t lie.

Disclaimer: None of this is to be deemed legal or financial advice of any kind. These are *opinions* written by an anonymous group of Ex-Wall Street Tech Bankers and software engineers who moved into affiliate marketing and e-commerce. We’re an advisor for Synapse Protocol 2022-2024E.

2017-2020 Old Books: Are available by clicking here for paid subs. Don’t support scammers selling our old stuff

Crypto: The DeFi Team built a full course on crypto that will get you up to speed (Click Here)

Security: Our official views on how to store Crypto correctly (Click Here)

Social Media: Check out our Instagram in case we get banned for lifestyle type stuff. Twitter will be for money. At 20,000+ instagram follows we will publish some city guides ranking each region we’ve been to

I thought $100k a year was the “made it” number, man life sure gave a smack in the face on that one, this was average salary in area ($50k) + another $50k in business income

It feels like a lot on paper, feels like nothing in reality, rather easy to “paycheck to paycheck” that even in a low cost of living location.

Easy to call into the trap of “I made it” & let expenses run rampant.

Hence, business income is crucial, if only for the lower tax threshold with expenses (write offs), not even considering earnings multiples.

I’ve always liked to assume I’m broke & use all that spare money to make more money to ensure “brokeness” never happens again.

(Yes I read all this in 3-5 minutes lol)

Good stuff. Where were you 10 years ago when I was in my mid-30s with 6 kids and they tried to put the golden handcuffs on me? I did give them the middle finger and start my own gig for awhile, but didn’t *commit*. After a decade of 14+ hour days (and, you know, 6 kids), was too burned out. Long story short: even without the golden handcuffs, a lot harder to do this stuff if you don’t do it in your 20s.