Basic Tax Saving Strategies as You Climb the Wealth Ladder

Level 2 - Value Investor

Welcome Avatar! Looks like its a good time to explain basic tax saving strategies. We’re appalled at the number of people who don’t understand how the law works. Absolutely no one with wealth is worried about inheritance taxes. We’re going to walk through a wide variety of ways to play by the law and reduce taxes owed 100% legally.

Since this all came up today for some strange reason there is no clear order on how we’re going to write it. Directionally, we’re going to try and make it go from low amounts to high amounts.

Part 1: Basic Gift Tax Exemption Rule

First Item: As of 2026, you can gift anyone you like $19,000. If you are married this would be $38,000 since you could gift someone $19K from husband and $19K from wife.

Before saying that the amount stops there, read the rules closely. It says you can gift $19,000 to one person, however, you can gift $19,000 to person number 2, 3, 4, 5, 6, 7, 8, 9, 10…. infinity. If you were to gift 10 different people $19,000 you would have given out $190,000 with no tax consequences.

Second Item: When you inherit stocks assumes no trust set up the cost basis is stepped up. If you had $500,000 in stocks and this ended up being $1,000,000 when you kick the bucket, the person who inherits the stock (son, daughter, grand kid whatever) will pay $0. They can sell it tomorrow, get $1,000,000 and owe $0 in tax.

Simple Bullets to Explain Why This is Valuable

Since everyone thinks $10M and $25M is not a lot of money on the internet, we realize this initial strategy seems meaningless. It is not meaningless at all.

If you think that your future net worth is going to be north of $15M as a single person or above $30M as a married couple, then you should start doing this basic one now.

Step 1 - Every Year Gift $19,000 to a ton of Recipients: Okay. We know that you can gift money to an unlimited number of people. Say you want to start moving money to your kids. You gift $19,000 to… grand dad (x2), Grandma (x2), Aunt/uncle (x2 each) and tow close friends. This gives you $190,000 to gift every single year.

Step 2 - Every year they dump it into an irrevocable trust or just a brokerage: The right way to do this is to dump the money into a trust. However. Since we’re dealing with a small amount of money, each person is simply going to open up a brokerage account. They will take the $19,000 they were gifted and dump it into the stock market (just say the S&P 500).

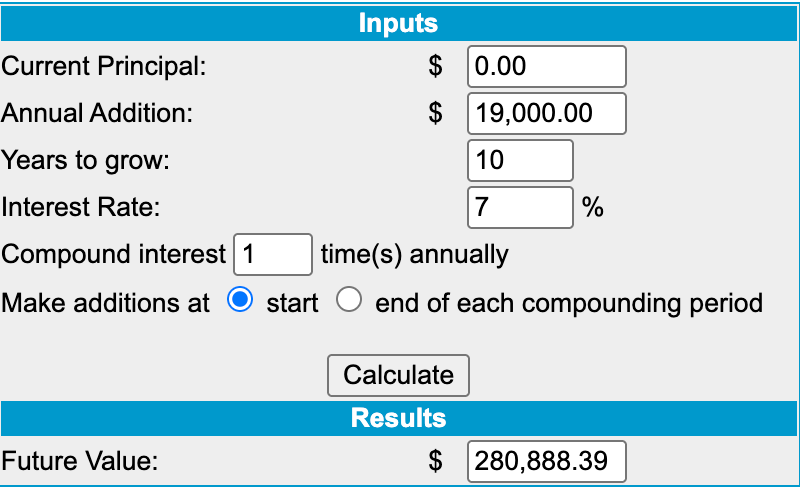

Step 3 - Click Fast Forward: After 10 years, you’ve contributed $1,900,000 into 10 brokerage accounts. Since each account is going to be invested in the stock market we’ll just use 7% return for the average. We’re well aware that returns are not guaranteed etc etc. This is just a basic framework.

After 10 years? You’re going to have 10 separate accounts owned by 10 different people with $280,888.39 in each account. Simply click “transfer on death” and put in the recipients name and social security number (all the legal jargon).

Step 4 - Hit By a Bus: Suddenly every single person dies. $280,888.39 is transferred to the son/grandson (whoever). 10 accounts worth a combined $2.8M are given and $0 in taxes are owed.

Step 5 - Bonus Maths: For those following along, if all the money is only going to one person you can grow the accounts to $14.99M each. All ten accounts can transfer $14.99M to one person. The person collects $149.99M. Total tax owed? $0.

Important Key Point

Where everyone gets messed up on this is that it is $15,000,000 per GIFTING person. Read that again. It is possible to have 100 people send down $14.99M each to one single person. It does not matter that the person received $1.49 Billion.

Part 2: Up a Level With Basic Trust Funds

Okay. So now we understand the lowest level of giving away money and having a step up basis. We can move onto structuring a trust. In the real world, you do not wake up one day and suddenly have $50,000,000 in a Schwab account.

Now lets say you have done nothing and are currently sitting on $10,000,000 liquid. Since this is not a lot of money according to X, everyone will find this useful as they have $10,000,000 and are under 35 years old.

Back Story: The rich dad or rich mom sold some small company and came into $10,000,000 post tax. In addition to that, they happen to be extremely young (35 years old in this case).

Well now you do have a problem. If you let that grow for 35 years you’re looking at $100,000,000+. This is way over the $30,000,000 mark for married people ($15,000,000 if single).

Enter Basic Planning: You do some basic math and realize you don’t even need more than $5,000,000 under your name. You already have a good income and you recognize the huge compounding that will occur. By the time your kids Henry the 17th and Evelyn the 24th are adults, you’ll be over the inheritance tax.

Set Up a Basic Trust

You set up an irrevocable trust. You take the $5M and toss it into the fund. At this point you’ve used $5M of your total gift allowance. Read that closely. If you are married or single you’d still have access to another $10M or $25M of gifting.

Step 1 - Send in the $5M: You write the check. The irrevocable trust now has $5M and owns a bunch of stocks growing at 7% per year. You can’t touch them the money is gone.

Step 2 - Die a Tad Early: The parents die a tad early. Under their name they have $25M. This gets sent to the kids. In addition to that the entire trust fund is outside the inheritance. It was already gifted away at $5M valuation. Even though the trust fund value has ballooned to $25M it does not matter.

Step 3 - Henry and Evelyn devolve into partying and hedonism if the vest isn’t set up correctly!

Important Key Point

The lifetime gift tax exemption needs to be used intelligently. If you give it away early you can reduce your headaches dramatically. If you try to do it last second you will likely pay a lot more in taxes than you should have.

The Five Key Points: 1) you want to find an asset that will grow without a ton of income being spit out - QQQ is a decent idea since the dividend yield is minimal, 2) transfer it early, if you transfer late you will just eat into you $15M or $30M of gift exemption, 3) appreciation outside of the estate is clear and 4) for the final touch - you want to make sure it is a true transfer where you cannot use the assets. A common set up is an irrevocable grantor trust.

Part 3: Reducing Business Income Tax

We do not know what your business is. We do not know how big time you will get. We have an outrageous range here with people who clipped their first exit for $200,000 to people who are already in the 8-figure club. Frankly, we don’t even care where you are at this point. If you understand that you must start a business to really make it, we’re thrilled you’re here. Our first $100 online was the most exciting feeling in the world (even more so than making the first million because it proved that the sky was the limit)

As a W-2: There is not much you can do. You get taxed before you even get paid. The business world is the opposite. You receive revenue, you deduct expenses, you deduct interest, then you have a income line that is taxed.

As a Business Owner: We’re skipping over S-Corp, C-corp, LLC etc. It is too hard to tell you which one makes the most sense. If you are serious about making money off of it and think it’ll exit for 8-figures then you should definitely look into QSBS before we discuss some simple income statement moves:

Using the Tax Code for Income Adjustments

Once again. Everyone on X is rich so we assume that you’re making millions in operating income. Several million.

You look down at your tax bill and you owe 50%. This is because you’re in the pico top tax rate with a incorrectly structured entity that you can’t get out of. Option 1 is to cry. Option 2 is to just play the game. We’ll choose option 2.

Current Income: Before taxes are paid you are showing $2,000,000 in taxable income. This means you would see a net payout of $1M if your tax rate was at 50%.

Step 1 - Borrow Some Money: Since interest is deductible you are going to borrow some money. You get a loan for $10,000,000 at 6% (we’re just making this up to make it easy to follow).

Step 2 - You Pay $600,000: Now you have taxable income of $1.4M. Assume the same tax rate of 50% and you collect $700,000. This is of course lower than $1,000,000 so it seems foolish until…

Step 3 - Put the $10,000,000 into Real Estate: You do some basic research and find some low risk real estate. You can generate a 6% return but this is before deductions: accelerated depreciation. You end up with limited net income, call it zero to keep it simple (tons of mom and pop shops show no income)

Add this up… Now you make $700,000 + 6% return on $10M in real estate that doesn’t get taxed due to deductions. $700K+$600K = $1.3M

Note: Yes this is an example. We’re not going to go into the weeds and if you’re sharp you’ll realize that you can game this quite hard if you are running a large entity.

Part 4: Big Time Problems

As they say more money more problems.

If you really run into big numbers and need to reduce the tax basis you really have three options: 1) you move to Puerto Rico for Act 60, 2) you renounce citizenship and move to a tax haven or 3) you go with buy, borrow, die.

Option 1: You already know if you’re in this camp. You don’t want to give up US citizenship so you simply pack your bags and move to Puerto Rico for 183 days out of the year. This gives you 0% capital gains tax and if you run an export services business a 4% total tax rate. You can make $1M or $1B and the tax rate will be 4%. (Note: depending on what city you live in, there is a small additional tax of around 0.5%, just call it 5% if you want to be safe with the annual filings, accounting, basic legal fees etc.)

If you have to ask, it isn’t for you. What happens is the guy does the math, realizes he can pull in decades of work within a few years. Tells his close friends “hey moving to PR”. Everyone else fills in the blank.

Option 2: You renounce US citizenship and move to a tax haven. You have to pay an exit tax and you better be sure you want to live where you’re going! Not going to bother much with this one since we doubt anyone cares much about it.

Option 3: This is the most common amongst the truly rich. Zuckerberg doesn’t care about income taxes because his salary is irrelevant. They just pay whatever they owe on the basic salary and move on.

Step 1: You have real money. Not $2M in S&P 500 money. You have say $100,000,000. Nice round number.

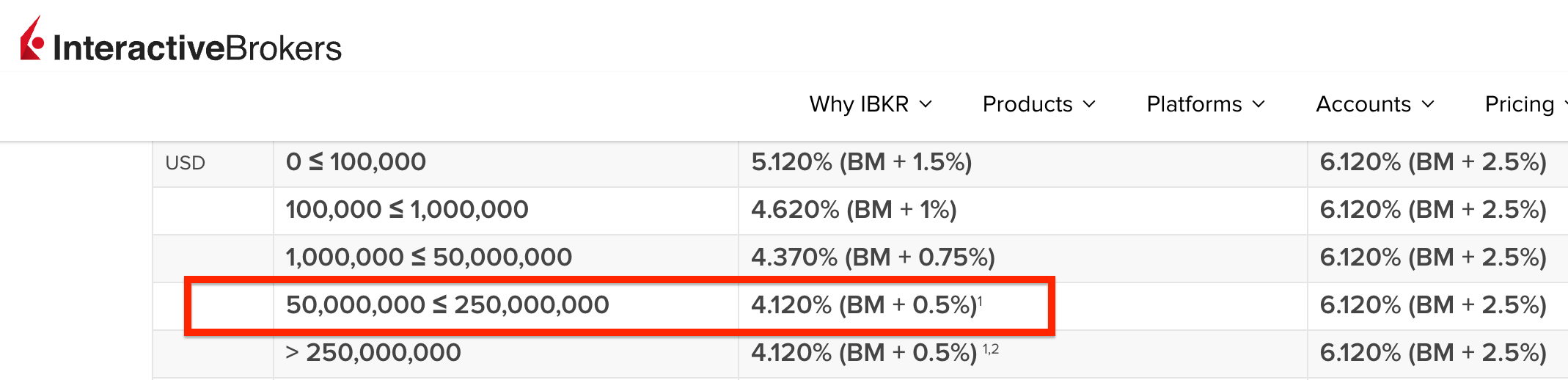

Step 2: You go and get a loan against this stock portfolio of say $1,000,000. Since you are only borrowing $1,000,000 against a $100,000,000 portfolio the interest rate is tiny. You go to interactive brokers and borrow this $1M at 4.12% (current rate as of this writing, source)

Step 3 - Let the Loan Grow Slowly Rack Up Debt: You borrowed $1M you didn’t sell a single stock. Say you have $100M and it is going to go up 5% a year on average. By year two you have $105M and you now owe $1M + $41,200 in interest.

Step 4 - Basic Logic: Does it make sense to pay the loan at all? Nope. You just let it accumulate interest and never pay it off until you’re in grave.

After 10 years, your portfolio is reading $131M. Even if you borrow $1M a year, your debt + interest owed is not even $15M. You’ve spent $10M, paid no taxes legally and your net worth went up!

Important Key Points

The chances of you waking up with $100,000,000 in your account is basically zero. One lottery winner per year or so.

If you find yourself in this position, you are simply going to borrow against the account instead of selling any positions. As Felix Dennis said: “reduction of any asset to cash very often leads to the imposition of capital gains tax - the equivalent of the Black Death to the truly rich”

Summary

As usual, there is no point in evading taxes. You should always pay them, just pay what you owe legally and use the rules intelligently.

You do not owe anyone additional money for being inefficient. Do things correct and you’ll find that your real tax burden goes down a cliff if you are a business owner/equity owner vs. W-2 employee.

There are a lot more complicated items to go over but this is good enough.

If you have questions on this we’re always around on the paid side. None of this is legal or financial advice, DYOR and we’re confident you’ll find what you’re looking for.

Ain’t no one rich worried about inheritance taxes or income taxes. It’s all wealth, capital gains, deductions and debt. By the book

Disclaimer: None of this is to be deemed legal or financial advice of any kind. These are *opinions* written by an anonymous group of Ex-Wall Street Tech Bankers and software engineers who moved into affiliate marketing and e-commerce.

Old Books: Are available by clicking here for paid subs. Don’t support scammers selling our old stuff

How ETH is Staked: Covered (here)

Crypto: The DeFi Team built a full course on crypto that will get you up to speed (Click Here)

Crypto Taxes: We have a suggested Tax Partner and 25% discount code, for information see this post.

Security: Our official views on how to store Crypto correctly (Click Here)

Social Media: Check out our Instagram in case we get banned for lifestyle type stuff. Twitter will be for money