Frozen American Dreams: High W-2 Earners Can't Buy a House

Level 2- Value Investor

Welcome Avatar! If you haven’t noticed, the housing market is frozen. In fact activity is so low that upper-middle class neighborhoods are not moving. This is because the DINK (dual income no kids) and HENRY (High Earning Nor Rich Yet) types are doing the math. It isn’t feasible to buy in the nice area since they will be fighting with the truly rich (business owners who don’t even need mortgages).

If two high-income W-2 earners can’t get the white picket fence house? It means the old model to get rich is broken. Not just broken. Structurally changed.

Part 1: What Your Parents Said to Do

If you’re in generation X or younger, you already know the drill. Get a good paying job, save money, get max house you can afford and slowly climb up the corporate ladder. The standard advice was doctor, lawyer, banker and later on engineer/top FAANG company.

Post COVID a major changed occurred. Still people don’t seem to get it. They quite literally printed $10 trillion dollars. This means that ownership/equity/assets went up in astronomical fashion. The new normal is set and the Fed has explicitly stated they want to see 2% inflation not deflation (where we go back to 2020 pricing).

Before people get upset. Yes. The 2 standard deviations above average still exists. Some small portion of society will be the unicorn employees. They climb the ranks to millions. This is called statistics. The vast majority of the people who make it will be business owners/asset holders.

Part 2: $300,000 a Year is the New $100,000 a Year

Back in the 1990s it was impressive to “make six figures”. You’re free to calculate the exact value based on “CPI” however, we can hopefully agree that the vast majority have a primary financial dream of being a homeowner. This is why we can make a clean argument that $300,000 today is the new $100,000 from the 1990s.

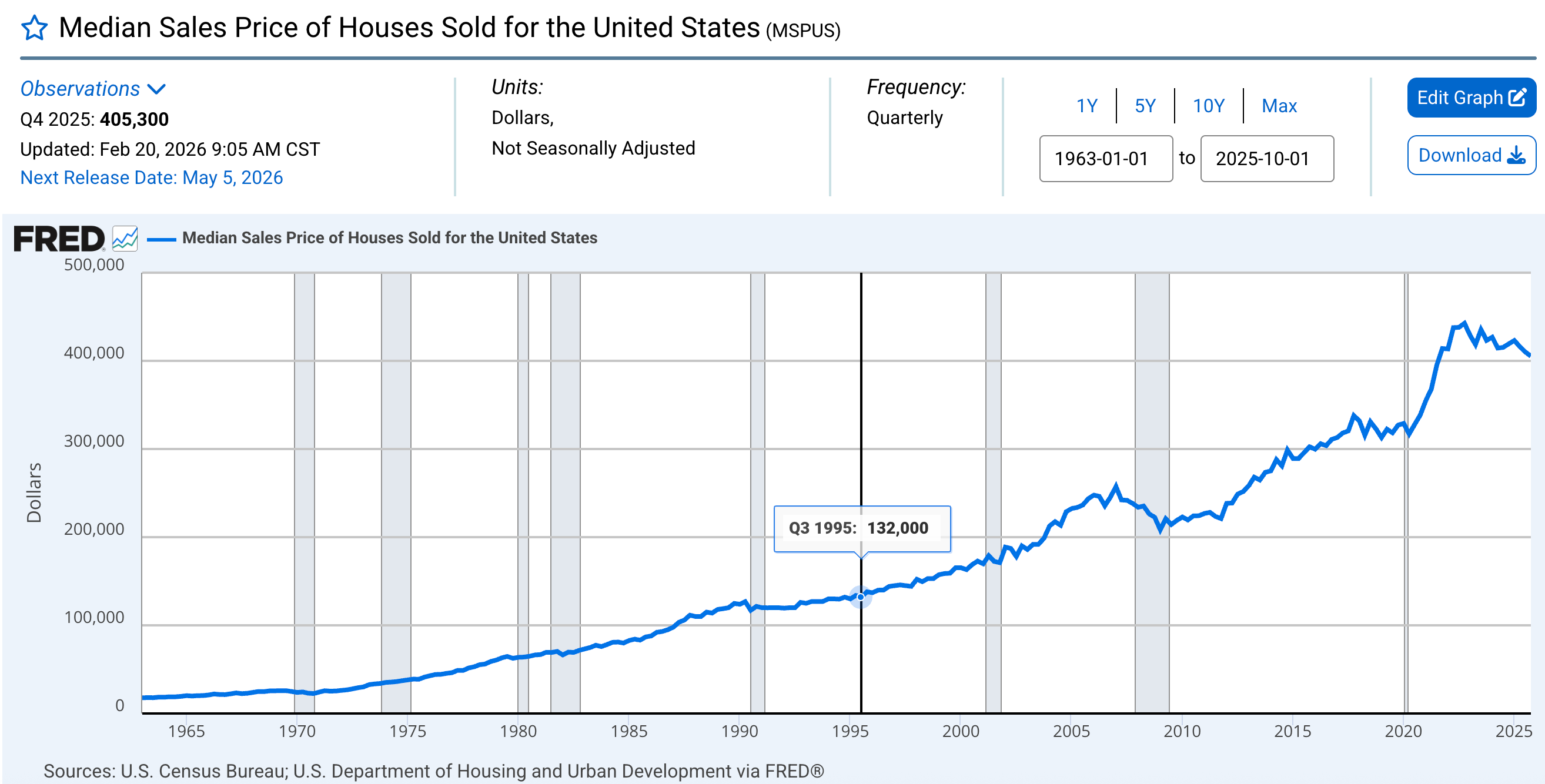

Back in 1995 a home was $132K. If you triple that, you get around $400,000 (just below). That lands you practically on top of the median priced home $405,000.

Think about it. If you understand that the money printing will never stop, you should not measure your net worth based on dollars in a checking account. Your net worth should be measured based on what you can purchase. If you were worth $1.3M in 1995, you could buy 10 houses. In 2026 you could buy 3 and have 5-figures in a checking account. That’s it. A ~70% difference.

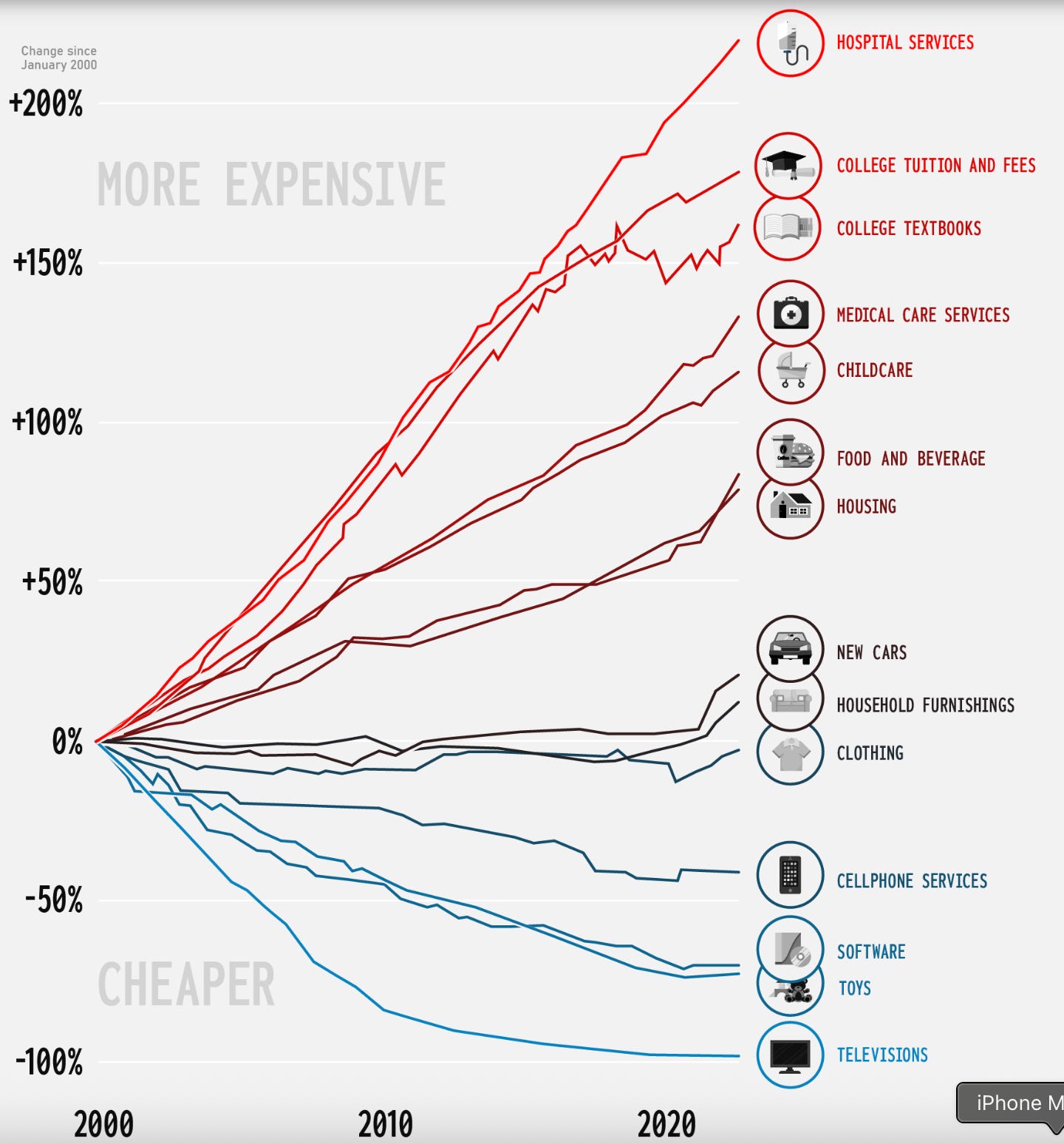

The craziest part? Housing went up the least relative to the other things you need to survive. Can’t eat your television unfortunately.

Part 3: Supply Side Broken Down

With the inflation topic out of the way, not only did they hand out actual dollars (stimulus), they also allowed people to get 3% mortgages.

The main problem with the 3% mortgages isn’t the rate. It is the fact that it isn’t portable and real estate people always obsess over buying “the max you can afford”.

So the spiral started. If you have a mortgage note in the 3% range and the next one would come in at 6.5%, that would be a ~40% increase in monthly payments for the exact same loan amount. Add on a second problem. Prices went up around 20-40% depending on where you are located. Realistically, you would need to increase your mortgage payment by at least 70% to move into a better home.

Simplistically 53% of the market unlikely moves

The government can change the laws (make mortgages portable, incentive shift to primary residence only etc.). Problem? Banking on someone else isn’t a great strategy!

Part 4: Prices Won’t Crash 50%

This gets a lot of headlines. Not because it is true but because people want it to be true. Even if we saw a large drop in home prices, there are too many wealthy people who would swoop in and buy it all up. A simple search of cash positions by major players like Berkshire would make this clear as day. If you’ve got hundreds of billions sitting in cash and the chance to buy homes at -25% (let alone -50%) comes along… the buyers are going to be the billionaires not the middle class person. Why? The middle class person would likely be laid off if the entire housing market declined by 50% in the first place. Also. People will take cash offers over debt due to faster closing and no loan origination risk.

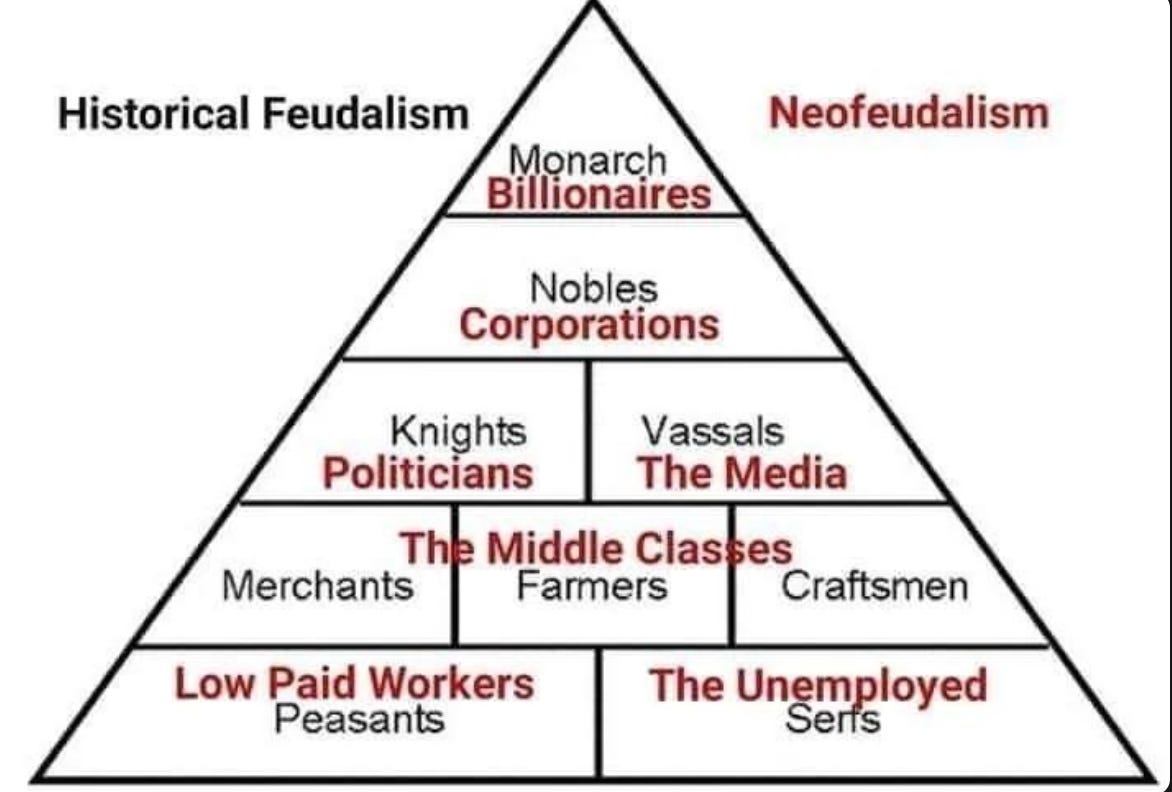

Part 4: New Age Feudalism

Summary so far: 1) People who own assets are much further ahead, 2) first time buyers are less likely, 3) upper middle and above is dominated by business owners and 4) socio-economic mobility declines and becomes more dramatic [you make it or don’t’].

This general trend is starting to mirror nepotism, gated communities and an emphasis on ending where you started. If born into the right family. You’re set. If not? Going to take a metric ton of effort/luck/skill to make it.

Part 5: The Next 3–5 Years

We picked out the prior image on purpose. There is a huge gap today. What prevents you from becoming a corporation? That’s right. You, Inc.

Absolutely nothing. In fact, that would land you somewhere in the Nobles part of the pyramid. Honestly good enough. From what we’ve seen the pico top ends up having more problems than benefits. Hard core depraved people with massive mental health issues.

First On Housing for You Inc: Since we used that as the starting point, guess what? There are solutions. In fact there are three of them. 1) you build your own house which we’re doing a walk through of in real time with real numbers - source, 2) you can go through and flip your first house to reduce risk + help the asset accumulation games - source and 3) you can go full WiFi money - our recommended path with numerous public success stories (example) and simply jump to the front of the line buying luxury.

Second - Only Asset/Equity/Ownership: Stop thinking about net worth in dollars. We’re guilty of this as well. We’ve stated that as of 2026 you really want around $3-4M and a paid off home to feel set for life. This is achievable. The main problem with using this? In 30 years $3-4M is not going to cut it. From 1995 to 2025 the cost of a home did a 3x. This means ins 2056 (assuming the same inflation we’ve seen), you’re looking at $1.2M for a median home (wild!)

You should create a spread sheet. You will track units instead. How many shares of stocks, crypto, homes, business ventures and any other asset that goes up with inflation (generally). This way when you update it once a year, you can see if your income is actually keeping pace with inflation/assets or not. If you were buying 100 shares of VOO last year and buy 90 this year… That means you’re losing to assets. Makes the game a lot harder and forces you to think long-term (planning 3-5 years ahead).

Third - Run Your Own Race: If you understand the game of building assets you know that it is extremely lumpy. One year you might make more than you made the last 15 years. The next couple years may be a struggle where you make less than you did 2-3 years ago. Name of the game.

The only reason that people are fine with this? They stuck out the 3 years. It takes about 3 years of truly going 100% all out. After this the majority have their first big win and are addicted to building. They are fine with having a down year because they’ve already seen the story before. No need to worry. Just the standard lull followed by an eventual spike. IF they never take their foot off the gas.

This is a big IF. From what we’ve seen 90% of people don’t even try. Of the ones that do, another 90% give up or lose focus. Once momentum is lost, you gave up an entire year or more. Any time you give up, start a new idea or stop giving it your all? Think of it as a big reset button. Like in a video game you’re sent right back to the start.

In a funny way, the gambling addicts would likely be well equipped to start businesses if they channeled that energy into the right venture. Going out on your own is an outrageous roller coaster of emotions. No different than the ups and downs if you put $20 on a random game or horse for the entertainment. Only difference is the outcome is in your favor (if you actually try - see point 3 most don’t)

Part 6: Everyone Else Getting Left Behind

One of the issues? You better choose your friend group wisely. If you find yourself hearing the same old stuff that worked 30-years ago and is no longer applicable? It’s time to change your contacts. If you meet 100 people running the old playbook from top universities? Maybe three of them make it out (statistical norm)

Most don’t adapt. For some reason humans are wired to follow the herd despite the typical person having no success in life. Unless you want to be in the same camp, best to find a different location.

The New American Dream: The new one? Its basically anything you like. Unlike the past, if you succeed with the new blue print it creates an entirely different world you never knew existed. Going to the beach at 11am on a weekday. Having no alarm clock. Choosing when you grind out the hours. Complete freedom to hang out with your family, kids, friends etc.

White picket fence + 2.5 kids + dog? Still achievable.

The map changed. The treasure at the end got bigger. Less people pick up the map in the first place!

Not as bad as the doomers make it out to be!

On that note we’re going to consistently follow new trends and look for ways to gain assets in bull, bear and neutral markets. Everyone else? Well they can look forward to their 3% merit increase when inflation registers at 3.3%. “They got it all figured out”

Disclaimer: None of this is to be deemed legal or financial advice of any kind. These are *opinions* written by an anonymous group of Ex-Wall Street Tech Bankers and software engineers who moved into affiliate marketing and e-commerce.

Old Books: Are available by clicking here for paid subs. Don’t support scammers selling our old stuff

How ETH is Staked: Covered (here)

Crypto: The DeFi Team built a full course on crypto that will get you up to speed (Click Here)

Crypto Taxes: We have a suggested Tax Partner and 25% discount code, for information see this post.

Security: Our official views on how to store Crypto correctly (Click Here)

Social Media: Check out our Instagram in case we get banned for lifestyle type stuff. Twitter will be for money