How Money Changes Your Lifestyle: Each Step Function in $ Terms

Level 2 - Value Investor

Welcome Avatar! Every few months there is a new “how much is enough” conversation on X. The problem with this is that “enough” depends heavily on the individual. If you want to have two kids and live in Charlotte, that is massively different from two kids and living in Argentina or New York City/Hong Kong/Tokyo/Los Angeles/Mexico City… etc.

The right way to think about money? How does it impact your lifestyle.

Conceptually, someone with $9 million vs. $10 million (11.11% difference)? Largely the same despite having a large $1,000,000 nominal spread.

That same $1,000,000 vs. $100,000? Massive difference in lifestyle (900% spread)

One thing you probably noticed reading us over time is that we use a ton of percentages. This is because you’re forced to think this way over time. Just because you can make money off something doesn’t mean you should. You don’t see deca-millionaires waiting 1-3 hours for a free ice cream!

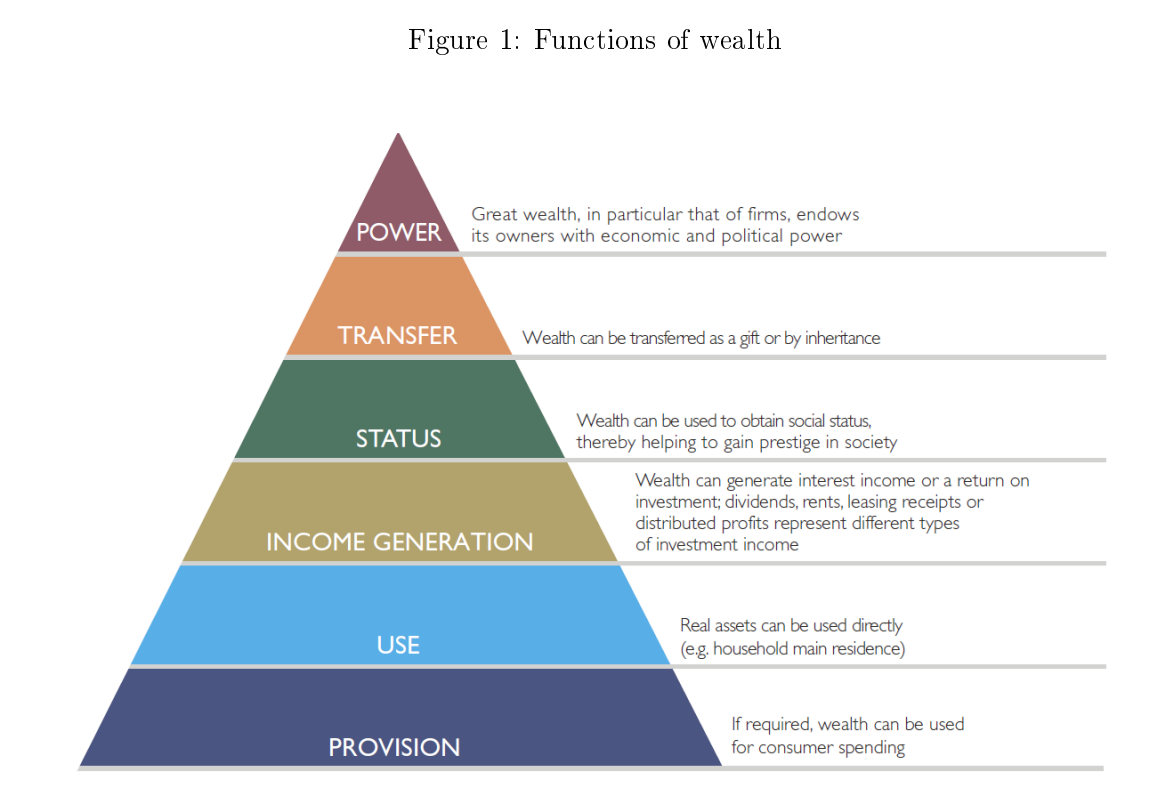

Important Concepts

Most people think improvement is linear. Some x = y perfect 1:1 line. Instead the real world is set up with exponentials. Lots of nothing, step function up, lots of nothing, step function up. The same actually applies to money as well. If you do a 20% gain from any wealth level, the lifestyle you have will not change. $10K to $12K? Basically the same. $1M to $1.2M basically the same.

Think about levels instead. Life is extremely similar to a video game.

Someone with $100K is not at the same level as someone with $1M. Similarly, $3M and $1M are completely different. $3M and $8-10M are also completely different. So on and so forth. Arguing about the exact dollar cut off isn’t relevant, it’s the rough percentage change needed to make the next level.

Most financial discussions burn time about the exact number. You should already know your number because it will be based on what type of lifestyle/level you want to retain. If you cannot see yourself spending more than $100K a year, there is no reason for you to aspire for more than $2.5M. Get to $2.5M and anything above that is gravy.

This also means that certain financial strategies are useless. If you want to get to $10M, skipping coffee isn’t a useful comment. If you want to get to $50M you should care more about tax havens than “tax loss harvesting” at the end of the year. On the lower end, if your goal is to get to $2-3M, you definitely don’t need fancy accountants or lawyers (a basic living trust will do just fine)

Income is Never Wealth

This is the last important item we separate out. Income has absolutely nothing to do with wealth. Nothing at all. If you make $1,000,000 a year but spend $999,999 a year, you’re broke. While making money helps create wealth, the point is the same.

“Rich” is defined by how much you could earn if you did nothing. (Spoiler, no one who gets to $5, $10, $20M+ is going to do absolutely nothing - too boring)

Level 1 - Mental Stability: You could survive about 6-9 months without working and without an unemployment check. If you’re below this, you’ve got serious issues. Absolutely all costs should be cut to zero, living in monk mode, getting to stability.

Level 2 - Skill Building Zone - $100,000: At this point you are not going to be homeless. As long as you’re not gambling it all on sports/casinos you’re going to be fine. All focus is on building skills/sources of income. WiFi Money, working an odd job, doing weird side hustles like flipping hot products, so on and so forth. At this point you’re looking to scale something else beyond the paycheck

Level 3 - Realize Time for Money Doesn’t work - $700,000 (7x needed): We’re not even going to a million. If you’re around this level you already know ***you will be a millionaire***. The main trap to avoid is buying far too much house or keeping up with appearances (draining cash flow)

Level 4 - Typically 2-3 forms of income - $3-4M (~5x needed): At this point you’re financial independence light. You are not rich in any tier 1 city (NYC, Miami, LA, SF etc.). In fact, you won’t feel rich at all. The reason you have low stress is because you *can* decide to move. If your income all drops to zero, you can pack your bags and live a nice life in 100+ different areas (Nevada, Abroad, Carolinas etc.)

Level 5 - Majority Small Biz Owners - $6-8M (~2x needed): This is our first level of actually being “rich”. $7,000,000. We get this number by assuming you have a paid off house (around $4-6M liquid earning about 5% - $200,000-$300,000 without moving a finger). Don’t care what all the LARPs say on X app. You’re perfectly fine in a Tier 1 city. You’re not the top dog by any means, but you’re set.

Level 6 - Low End Legacy - $15-20M (~2.5x needed): We’ve stated that $25M is the easy cut off for post economic wealth. Even at $20M, you’re generating $1,000,000+ even with boring government bonds. Absolutely no shot you’re struggling. Not in NYC, not in CA, nowhere.

Level 7 - Power and Influence - $100M+ (A huge 5x needed): This is where you have public influence. The exact threshold is impossible to know. That said at $100M you can certainly influence at a local, city and maybe even state level. You move the needle in every single room you walk into (except the illusive billionaire row where you’d likely get invited to the White House at least once).

Now that you have the seven levels, we can walk through how to get there, what is a waste of time and you can decide what is “rich enough” for you. Our definition of rich is level 5 since that is where we’ve seen a huge swath of people lose interest in talking about money. That’s a big sign in public settings. If the guy doesn’t care about career trajectory, investing ideas or starting a new business, he’s probably at or above the ~$7 million marker. He also exhibits next to no stress on his face. The biggest tell of them all.

Level 1: Getting to Mental Stability - 6-9 Months Expenses

This is the only level where FIRE type mentality works. It’s actually a perfect phrase for this segment. FIRE is supposed to mean Financial Independence Retire Early. In our world view it just means fire. Your financial life is quite literally on fire.

If you’re in this camp: 1) no job pays too little, 2) no paid fun is allowed - enjoy the library and the outdoors and 3) legitimately coupon clip. Do whatever it takes.

We doubt any of our readers are in this group or even the second group, but for all of the extended family that needs tough love, there it is. Monk mode + trade time for money. You have no other choice.

Level 2: $100,000 - The First “Aha” Moment

Your mentality is to begin converting your income into equity. Read that 100 times if needed. Income needs to be converted into equity.

The second goal is to convert your earning into equity. This second one is reserved more for Level 3 but the idea begins to resonate here.

Cash is just a protective layer. Much like your skin. You just need a small amount of it to run the entire machine.

Trap 1: Most people start upgrading their lifestyle too early. Since they feel safe they think there is no real risk in upgrading immediately. The risk is that they become reliant on someone else. While you’re free to go out a couple times per week, the real risk is in bold italics. By upgrading your spending a bunch, you’re actually handing over your future to a middle aged manager running spread sheets all day. Hint: you’re not family to him.

Trap 2: The faster you can get away from time for money exchange the better. Conceptually this is extremely hard to understand until you live it. Your first online sale of $100 is going to hit like a kilogram of recreational drugs. You’ll realize that the sale came in while you were not working. Someone clicked on a link somewhere, went to your website and clicked buy. If you spend the next 1, 3, 5, 10 years renting out your time (doing consulting/odd jobs) you’re losing valuable copywriting and ad reps.

Trap 3: The big one is a psychological trap. You look at your income and savings rate. You decide that saving an extra 5% isn’t going to make a difference long-term. This is how you start spending instead “what is the point”. Guess what? You’re actually right. There is no point in trying to squeeze a few extra dollars out of a salary. That game has been maxed out already. Go find people who made it. You’ll find that none of them were trading time for dollars.

Level 3: $700,000 - Middle Class Trap

Yes. We’re saying around $700,000 in wealth is middle class still. Not because of the math but because of the lifestyle. Again. That is what wealth is really about. What type of life you can afford.

In this band you will get the vast majority of NPC talking points. They will be obsessed with dumping everything into the S&P and taking out a low rate mortgage. House Hacking, driving beater cars, etc.

The Vibe: Most people lever up for a simple reason “my net worth goes up but my freedom and quality of life isn’t changing”. Every year they are able to grow the digits on the screen. However. Each year they are eating the same stuff, taking the same vacation and driving the same car.

The real issue they face? They are still time trapped.

Majority at this level have no real control over their day to day lives. Someone else decides when they show up for work. When they can travel. When they have to be sent to a new city for a business meeting. So on and so forth.

In addition to this, due to their focus on retirement and NPC talking points, their wealth is typically illiquid: 1) house and 2) 401(K)/IRA/Retirement account.

On paper, you’re doing great. You’ll be fine in old age (60+). However it doesn’t feel like success.

Most blow it right here. They lever up buying the most house they can afford, the nicest car they can afford and simply ship their monthly spending into those two items + a retirement account.

Fine on paper, trapped due to being illiquid. Don’t be the purple bar on the left.

Your goal is to move that green portion of the bar chart. You already see that is the difference between the rich, ultra rich and the middle income section. You want to become business equity rich and cash poor (as a percent of wealth). You do not want to be house rich and cash poor.

You have no excuses when it comes to building equity and liquidity at this point. You’re not going to be on the streets. You’re going to be completely fine in retirement.

Time to graduate into the mental illness that is paid ads, tech stocks, crypto, performance based roles and scalability.

Level 4: $3-4M - First Significant Lifestyle Jump

Wait, wait, wait. BowtiedBull said there would be a lifestyle component to each level. Where is that? Guess what… it is exactly the same until level 4. The only difference is personal stress levels.

If someone has $100,000 or $700,000 the quality of life isn’t going to budge much at all. You know this intuitively because places like Miami have tens of thousands of BMWs. Some of them are being driven by millionaires while others are being driven by people who make $50,000 a year. The naked eye cannot tell the difference.

In fact, you could psyop anyone into thinking you’re a millionaire.

What Happens at $3-4M? Well you start living a life that is not possible to fake. The YouTubers try to fake being multi-millionaires (Larping in clubs, daytime activities etc.). It doesn’t work. This is because a person with around $3-4M is consistent.

Since you know you can pull in about $150,000 - $200,000 while doing nothing, you’re simply going to change your daily routine. You’re going to eat out more. You’re going to go to the nicer places more. The frequency is impossible to fake. Instead of taking a bunch of photos at Cote in Miami, you’re simply going there on a weekly basis.

The most common phrase is this one:

“Celebrating something special tonight?” vs. “Oh hey (name) how have you been!”

Does not take any social skill to realize the second person is playing a different game entirely.

You are 90% Location Agnostic: Yes we made 90% up. The concept is the same. You can basically live a high quality life in 90% of the cities in the world. With $3-4M, you’re not living it up in NYC. However, you are certainly living it up in Tier 3 cities and below.

Anything Outside of These Major Metros and You’re Living Large

You Have Bought a Lot of Freedom: You no longer need to work a job you hate. You don’t need to grind long hours if you don’t want to. You’ve cracked open the door to the main event. You’ve basically got the nose bleed seats to the superbowl. You got in but you’re not in the lime light.

The only real trap here is pretending you’re bigger than you are. Overspending on luxury travel, buying a McMansion, wild private schools that don’t even have great results. So on and so forth. These are all related to social/status games. Avoid status games.

Your entire focus is on optimizing your equity and time for equity ratio. You have too much talent and too much experience to do nothing. May as well use it for maximum ROI on everything you do.

9/10 times you will have at least three sources of income. Example being: 1) a couple rental properties, 2) your main wifi biz cash flow machine and 3) a hobby consulting/W2 set up.

Per usual, if you don’t believe us, LARP as a rich guy needing to talk to a wealth management firm in your city. Ask what their typical client profile is. They will heavily lean to small business owners and some real estate!

Level 5: $6-8M - You Are Rich

This isn’t video game money where you can spend and not care. You’re not flying private. You’re not rubbing shoulders with politicians. You are time rich (can do what you like when you like) with no regard for variable expenses. Variable would be food, transportation, concert tickets, baby sitters, house cleaning, dry cleaning etc. All of this stuff doesn’t move the needle on your annual burn.

You do not need an alarm clock. That’s the level of freedom you get in this band.

In addition to that? You’re officially Location Agnostic.

List of Lifestyle Benefits: 1) you can live in any city you like, 2) the next generation - unless you have a full puppy litter of kids - is set for life and 3) all of your income is now discretionary - you can start any business you like and quit any business you don’t like.

You are in a structurally different world from the people in the $3-4M band who are in a completely different world than people with ~$1M or less.

To top it all off? Even if you have a small family, you don’t need to make any quality of life trade offs.

Traps: The main traps are Ladies, Liquor and Leverage. Essentially hedonism and greed. We would typically list “keeping up with the Jones’s”, however, most people who get to this level have no interest in that game anymore. They spend on some luxuries here and there but they already went through the trial and error of realizing a massive fixed cost base is no different than debt. A massive stress inducer and liability

Opportunities?

We’re confident that a ton of people who read us will be at this threshold in about 3-5 years. If you think about it the long-term readers are somewhere in the $2-3M range already. Layer in some more work, some investment returns and you can see that easily getting to this band.

The game changes to the following discussions: Tax planning, estate planning, asset protection and volatility of portfolio.

Tax Planning: Deciding if tax havens make logical sense. Moving to a no-state tax area. Should you start a new company as a S-Corp, C-corp etc. These decisions now matter.

Estate Planning: Living trust? Yep. Now need to look into irrevocable trusts and blind trusts in certain circumstances.

Asset Protection: You care a lot more about insurance and big blow up risk. Anyone here needs an umbrella insurance policy for freak accidents.

Volatility of Portfolio: You begin to care a lot less about the exact return and care more about the total portfolio swing. You begin matching the volatility (expected worst case down draw) to your annual earned income. If you can put away $600,000 a year and your liquid portfolio is around $5,000,000, you’d want to have a rough volatility around 10-15%. If everything goes bad and you’re down 10-15%, your general earned income makes you flat anyway (you just buy more shares, more bonds etc.).

This allows you to continue to build wealth without being in some ugly situation where you income goes to zero and your investments are down 80-90%.

In short complexity is a real issue around this level. At $1M and below, asking for an accountant, lawyer, tax strategy, complex estate? Just a waste of time that should be spent on increasing equity

Level 6: $15-20M - Post Economic

None of your important decisions are based on digits increasing. Most of your important decisions are related to your personal life. You can even fly private on occasion and ignore the sticker price on any vacation.

Fancy Opportunities: Most of them are frauds. Instead of friends and family showing up to ask for a “$10K loan because it is nothing to you”, the real scaled up scams show up. Suddenly you get calls from private wealth manager, private equity managers and various cap tables that are home runs.

If you’re wondering why so many celebrities and athletes go broke, this is one of them. Ship out 20-30% of net worth into a single bad private deal and you’re setting yourself behind by 3, 5, or even 7 years.

Major Differences: Unlike the prior level, you do have access to the top level of spending. Private flights are certainly doable if you absolutely need them.

The big issue is that security becomes a bigger dilemma and you need to become more guarded. No dopamine based investments. No private pitch decks. No massively concentrated bets that were given to you by someone else. You should only have heavy exposure to things you fully control (such as your own business).

Waiting Around for Lady Luck: At this point it is basically up to her. If you are going to get to $100M+ or not. If there was some sort of magical step by step map, everyone would talk about it. The truth is that you need luck.

Money doesn’t make a good business. In fact money could make your business worse. Trying to use cash to solve any problem that comes up “just hire a new designer” “just switch to a new manufacturing company” “just spend more money on a new angle”. Money doesn’t make you more talented or capable. Not in the slightest

Level 7: $100M+ - Walking Institution

If you find yourself in this position, you’re a walking public company. Seriously. The amount you’re in charge of could be a small family office. In fact that’s where you’re going to go.

No one in this level is worried about inheritance taxes or gift taxes. They are busy setting up family offices for succession planning. Trust structures and security are now priority number one.

You can get to Level 6 rich by being a cut throat and intense business owner. However. To get to $100M+ you are 9/10 times commercialized. If you mention your company, someone within any 30 person room will know the name. Can’t hide if your product is sitting on a shelf in Costco, that’s for sure.

What to do at this point? Well Felix Dennis gave it all out years ago. In paraphrased terms:

“Get to $30M or so (post economic), then spend time doing things he liked poetry, planting trees, being entirely location agnostic. In the end, the goal of wealth is to buy time not toys”

Summary

People obsess over exact numbers so we gave them out in this post. This is as of 2026. Just remember that inflation will change all of this in 5, 10 or 20 years. The amount of money that allows you to free up all your time is the first level of rich. In the future that might be $10M, in another decade or two it could be $20M!

Being rich is all about how much you can do if you don’t work. This is because you’ve removed time from being a constraint on your life.

Disclaimer: None of this is to be deemed legal or financial advice of any kind. These are *opinions* written by an anonymous group of Ex-Wall Street Tech Bankers and software engineers who moved into affiliate marketing and e-commerce.

Old Books: Are available by clicking here for paid subs. Don’t support scammers selling our old stuff

How ETH is Staked: Covered (here)

Crypto: The DeFi Team built a full course on crypto that will get you up to speed (Click Here)

Crypto Taxes: We have a suggested Tax Partner and 25% discount code, for information see this post.

Security: Our official views on how to store Crypto correctly (Click Here)

Social Media: Check out our Instagram in case we get banned for lifestyle type stuff. Twitter will be for money