Is The USA "Too Big to Fail"?

Level 2 - Value Investor

Welcome Avatar! Here we’re going to outline our general rationale around the US market. While paid subs know what we think on an annual basis, on a 20+ year time horizon, betting against the USA is a failed proposition. At this point, we’d argue that a massive crash would cause huge money printing not just from the USA but the Globe. Reason? Foreigners from around the world do everything they can to dump their money into the USA.

If you’re a wealthy foreigner? Many just park it in luxury real estate. If you just got your first “bag” ($30-50K in many countries is considered a bag), the first goal is to get that money into US based markets (NASDAQ/S&P etc).

Part 1: Big Picture

Ignoring the near-term (something everyone develops or cares about *after* they have made it), if we zoom out we can see the writing on the wall. There is just no way to get the budget to balance without a huge deleveraging crisis/mass layoffs at government level.

Good Luck Stopping This!

While the socialists argue that the rich “control too much”, you can just smile and nod. The Fed is quite literally printing trillions of dollars per year which is causing the amount of money to fly up in a vertical fashion. They could allow for a deleveraging event. Problem is it would be politically suicidal.

Financial Cobweb of Problems

That’s just the big picture part. There is also an underlying bond/equity problem as well. When foreigners get rich, they do not want to leave all their assets in their country. In fact, their goal is to get it out as fast as possible to invest in the USA.

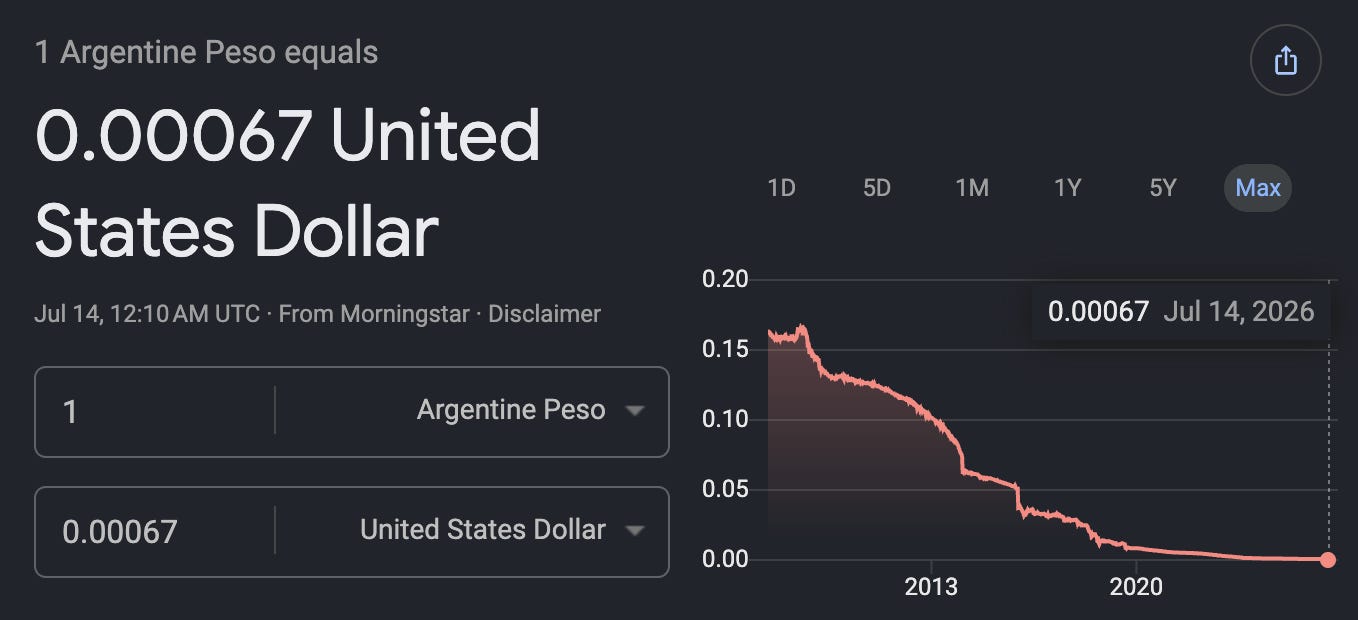

The ultra rich, they will buy stocks, bonds and of course those cash purchases of luxury real estate by the ocean. In addition, the recent come ups will take their $50,000 and try to move it to US markets as fast as possible. If you need any reminder of this Argentina is always the gold standard (Blue dollar rate, mass devaluation and a place where the Peso isn’t taken seriously in any business transaction).

Incredible Minus 99.58% decline over the last 20 years

Real Estate: Already well known. There are two major factors there: 1) illegal immigrants and 2) ultra wealthy foreigners that buy up houses with cash to land bank. We’re not here to debate if its good or bad, just doesn’t matter. The USA works the way that it does.

With this set up, foreigners actually want US prices/US success. If you take the long-view, the rich foreigners buying the home here just means their country will likely support the USA (the rich have the most sway in any country politically - since they generated the most economic value 9/10 times from absurd risk and effort).

Knew All This? Yep It Gets Worse Though

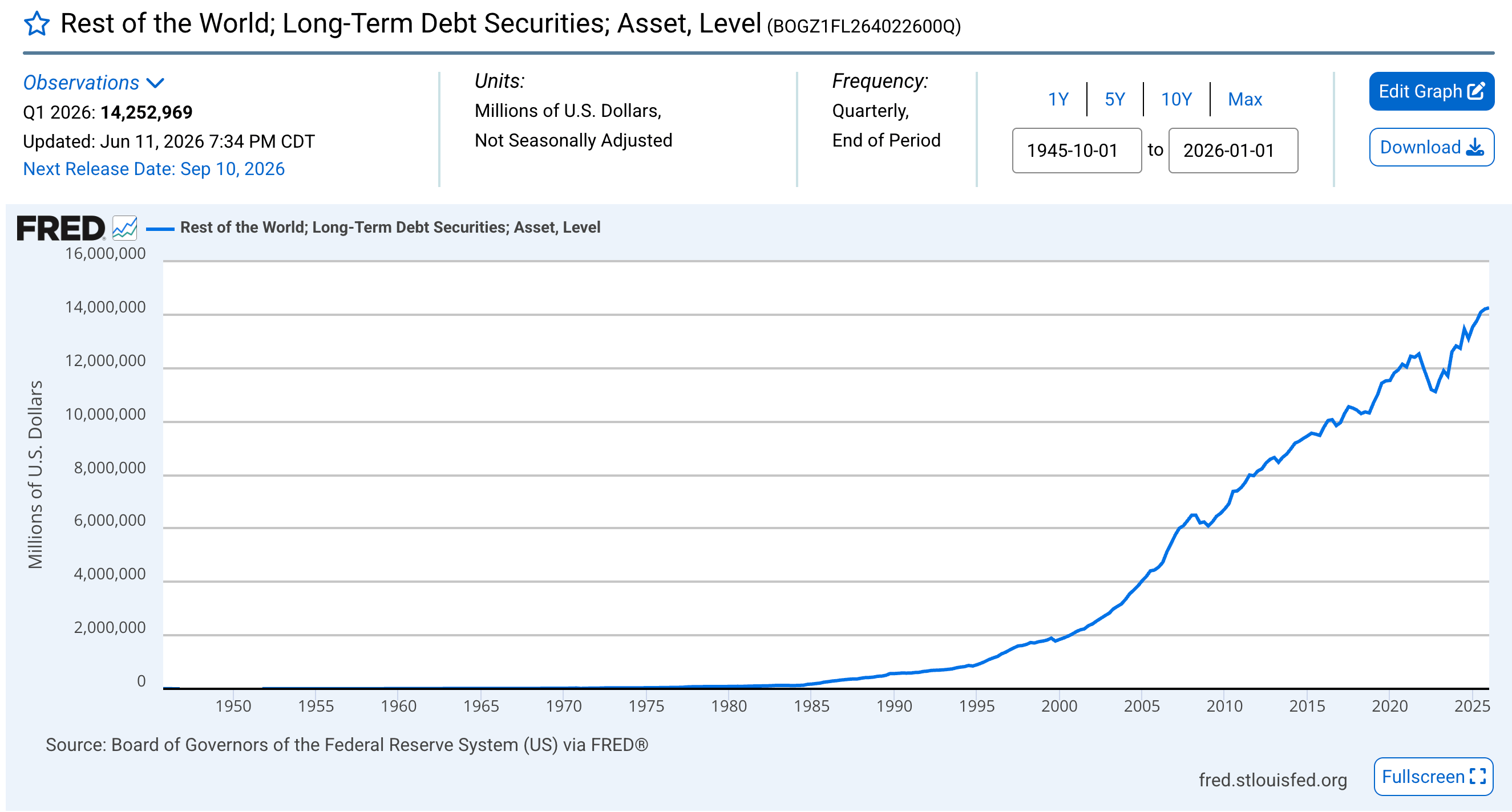

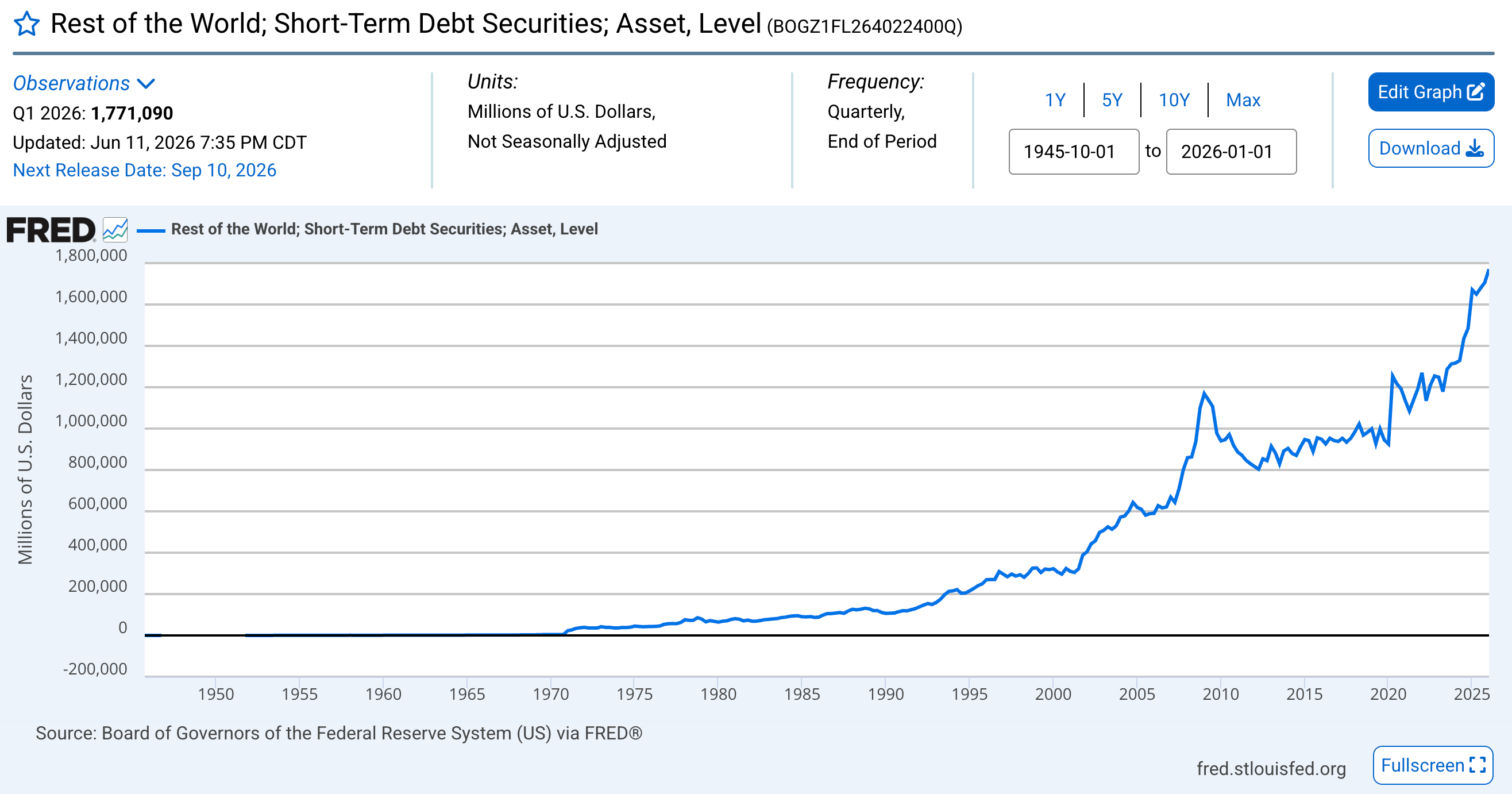

Lets say that the USA decided that it would print a bunch of money. Foreigners could potentially reinvest in their country. The problem is actually a lot bigger than most realize. The foreign market for bonds and stocks is ~25%. That’s right. A quarter of all purchases in the USA for bonds and stocks are being made by foreigners.

US Stock Market about $95T foreign holdings about 21.4%

US Bond Market about $61T foreign holdings about 26%

Once you do some quick math based on this, you realize that the wealthy across the globe lock up their money in the USA. 25% sounds “okay” since it is less than half. And. How many millionaires are available compared to the USA? Once you do that calculation it shows you the foreign rich are heavily exposed to US stocks and bonds.

The Next 9 Countries still don’t add up to the USA. China also has extreme controls to lock wealth in their country.

![The Countries With The Most Millionaires [Infographic]](https://substackcdn.com/image/fetch/$s_!58m0!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fb04654f5-4fd5-4cc6-9a6c-5806f15c1764_960x684.jpeg "The Countries With The Most Millionaires [Infographic]")

Proportionally, the wealthy foreigners will want to see the USA succeed as it is in their best interest. This should help explain why practically all the countries across the globe printed money during COVID, even the ones that didn’t really shut down to the extent that we did. Once the US moves, everyone follows.

Summary

While most just focus on the debt and real estate problem. The entire US market is intertwined globally at this point. You can click a few buttons and get access to US markets if you have basic tech savvy skills (hint: anyone rich will have access to the right tools/info globally even if they personally do not do all the managing themselves)

If we go through a downturn, the USA prints, the world prints and we get back to a baseline where people are not defaulting. Rough max length of pain seems to be 1-year based on what we saw in 2001/2008/COVID. For the doomers, your only real hope is that AI/robotics cause structural mass unemployment and UBI is rolled out. Our bet is that commerce just becomes more digital (IE. the work you do are not even named yet, similar to how we didn’t have a huge number of software/internet jobs in the 1980s, it didn’t really exist).

Part 2: Digging Deeper Into the Mechanisms

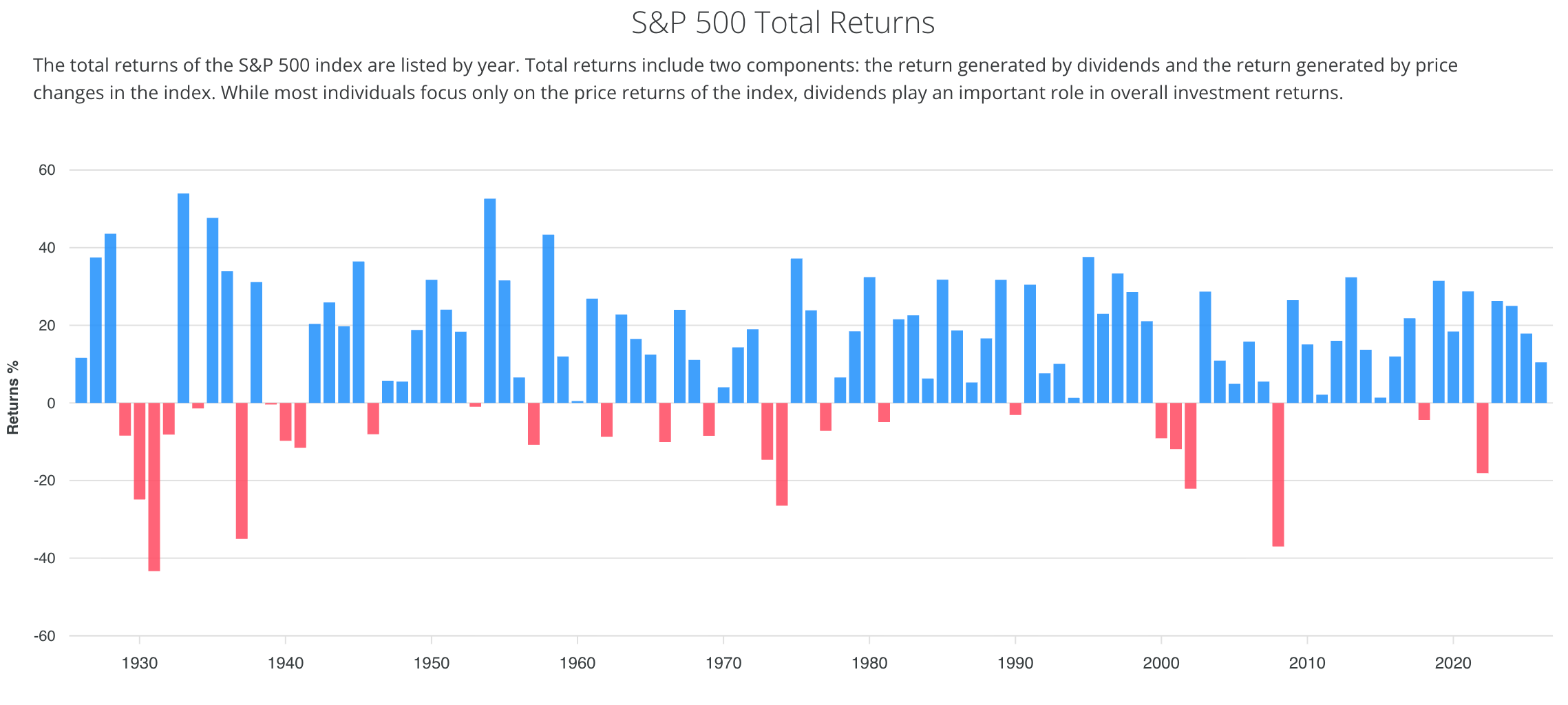

If you’ve read us for a long time, you know that for about 15+ years we’ve said that S&P/QQQ is basically a savings account. Unless you’re planning on retiring soon, you should just assume that is is a savings vehicle that will compound for decades (beating or keeping up with inflation)

That has largely panned out. The difference is that the main stream now believes the same thing. As more and more people pile into stocks/S&P they will begin worrying more about a "equity collapse” similar to the olden days “run on a bank” worries.

The Trump Accounts are highlighting this publicly as the only investment option is the S&P 500.

Thesis: S&P 500 is moving from “stock market” to the USA’s retirement plan, savings account, economic indicator and fundraising for the entire country (attracting foreign money). If we’re right on this, it means the government would not want to see a sustained stock market crash for longer than a year or so (print to save).

Now for Some Numbers

As of today, the US retirement system has ~$48 trillion, with ~$10 trillion in 401K accounts. All of this money is becoming more concentrated as well. The top 10 S&P 500 companies are about 36% of the entire index.

If you have 401K passive bids, new IRA passive bids, new children account passive bids and you have all this looped with a company match + general brokerage accounts it creates a self fulfilling cycle. Stocks go up, weights go up, contributions go up and more money goes to indexes vs. savings accounts.

This is stable unless you have a catastrophic event (deleveraging, COVID type downturn, a dystopian AI issue or an extreme War/Act of God).

While the Government can’t go in there and market buy S&P 500 every single day. They could easily pump money into the debt markets to create a floor on the decline (IE. stop the bleeding while making it look like they didn’t interfere with the stock market)

We’ve already seen a multitude of bullets fired. They can do any of the follows: 1) cut interest rates, 2) aggressive buying of securities for the Assets on the balance sheet, 3) flood system with money via dealer and repo market, 4) back money market funds, 5) choose certain industries to support (bank bailout, airline bailout) and 6) emergency facilities/stimulus.

All of this would get turned on to restore the stock market. It would be labeled as “saving the common person’s retirement” extremely easy sell.

Instead of directly saving the S&P, they would back stop the credit/plumbing system that prevents the S&P from dropping too low.

S&P is Systemic Now

Take a doom scenario of a -50%. This is possible and has happened before. It didn’t last a full year but it did cause max pain for a short period of time. If this were to happen today it would lead to: 1) backlash from retired community, 2) pension funds, 3) fundraising freeze, 4) RSUs blowing up, 5) Bank collateral disasters - Retail is now doing stock based loans and 6) significant decline in spending due to negative wealth effect. Oddly, even the billionaires care if their net worth says $1B instead of $2B.

Even Before This Huge Wave, it was rare to see more than 2 years of calendar year negative returns. Usually one and done.

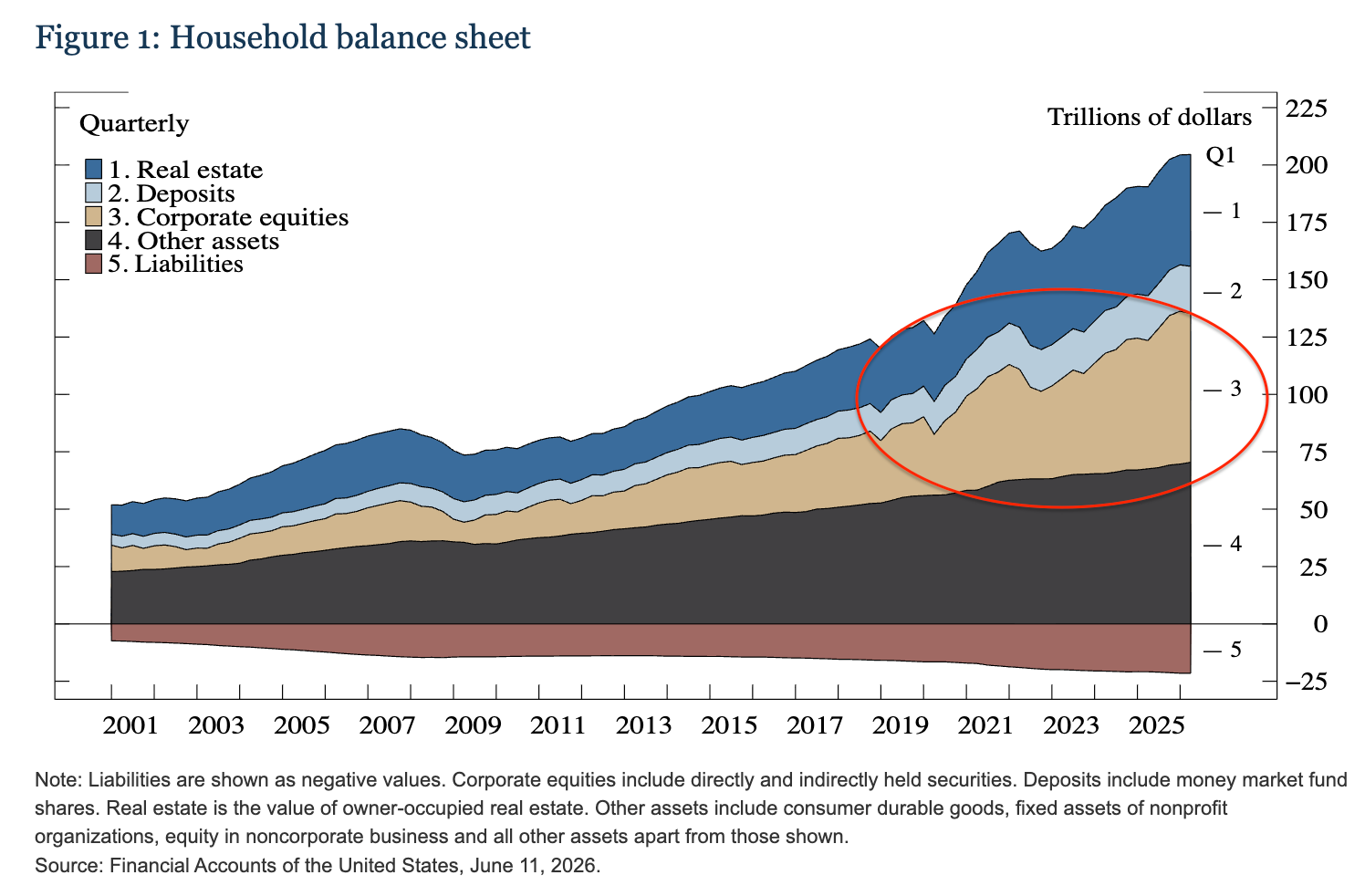

If the Fed was worried about a crash in 2020, take a look a the actual balance sheet of the typical household. The rapid rise in stocks as a percent of wealth is enormous when compared to just 7-10 years ago. In a sentence, economy and stocks are going to become increasingly correlated once people view it as “savings”.

Perhaps we’re biased, however, this seems to line up with our general long-term view of needing to be: 1) niche or 2) scaled up mega company. If there is a large passive bid, the biggest players (top 10 companies) just become larger and a bigger percent of the index.

Since people believe that the bailout will come no matter what, they will just click buy and perpetuate the cycle. Index becomes a savings account because investors believe it will be protected even if there is a one year ugly drawdown.

Summary

If you believe this then the conclusion is that you should only really actively manage a S&P/QQQ account if investing is your primary source of income. We’ll write that again. Unless investing is your primary source of income, S&P/QQQ sell offs shouldn’t be relevant to you.

If you’re at a point where investing returns are 2-3x your earned income, then you should pay attention to potential down years. Other than that, it does not matter for 99% of the population.

The second takeaway is that you really don’t need much more than ~2 years of living expenses at any time. If you have that in cash/liquid bonds/something similar, it will be “good enough”. If the market actually goes down 25% twice in a row, you’d survive it without being forced to sell near lows.

Part 3: Land of Opportunity Premium

The main competitive edge the USA has beyond controlling the money supply is controlling the global socio economic & cultural stage. Travel abroad and you quickly learn that foreigners listen to a ton of the same songs that you do. They just don’t understand them. They can recite it and sing along with zero knowledge of what it means.

While this is glossed over it is actually pretty important. As long as people believe the highest options will come from the USA, we’ll continue to poach the greats from other countries. We’re not even relevant in Soccer, yet Lionel Messi now lives in the USA (Fort Lauderdale).

If you look at the top CEOs in the USA, a large chunk are immigrants (Musk, Huang, Pichai, Nadella, Xu, Roman… the list goes on and on). They could have created companies outside the USA but as long as they think their chances of success are higher here (they are), they will continue to come in droves. ~12% of the S&P 500 CEOs are immigrants (also kills the whole idea that it’s impossible to make it in the USA if 88% are domestic).

On that note, if the USA is turning the S&P 500 into a savings account, we’re unsure how clear the message can get. Either learn to be an owner/operator and investor or join the crabs in a bucket chat around the company water cooler.

Disclaimer: None of this is to be deemed legal or financial advice of any kind. These are *opinions* written by an anonymous group of Ex-Wall Street Tech Bankers and software engineers who moved into affiliate marketing and e-commerce.

Old Books: Are available by clicking here for paid subs. Don’t support scammers selling our old stuff

How ETH is Staked: Covered (here)

Crypto: The DeFi Team built a full course on crypto that will get you up to speed (Click Here)

Crypto Taxes: We have a suggested Tax Partner and 25% discount code, for information see this post.

Security: Our official views on how to store Crypto correctly (Click Here)

Social Media: Check out our Instagram in case we get banned for lifestyle type stuff. Twitter will be for money