Next Issue a Squeeze vs a Crash?

Level 2 - Value Investor

Welcome Avatar! If you’ve been waiting for a crash, you might be a bit disappointed in this potential outcome. From what we’re seeing prices have gone up once again and employment opportunities haven’t improved to match the change in asset prices + general cost of living.

We’ll make an argument for a long-term squeeze vs. a sudden deflation/blow up.

Structural Squeeze?

In short, prices go up, people lower their standard of living but remain employed.

If this sounds crazy, Europe would represent a good example. Out there it is much more common for young people to live at home and the wages are worse than the USA (relative to cost of living). Housing is a great example of this.

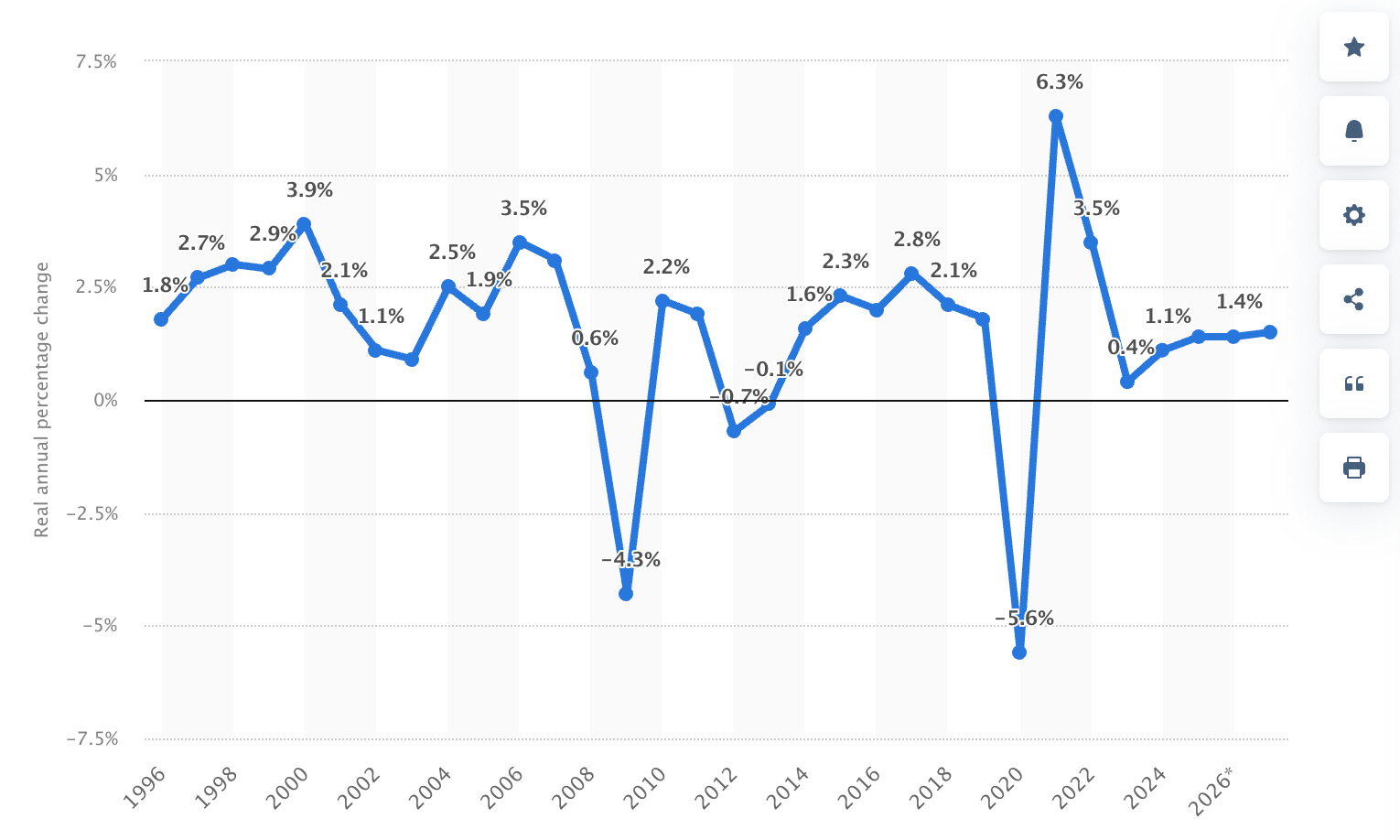

From the above you can see that it is possible for prices to go up even more (housing). This is because 10x median family income is much more severe than the USA (sitting at around 5-6x). Said differently, US median affordability is equivalent to the cheapest set up in Europe!

Outside of the money printing in 2021, 1-2% growth isn’t doing much for anyone

How This All Happens

If you were around for the 2008 financial crisis, you remember how bad it got in Europe. The bond market was blowing up and they even came up with a nickname for the next country to potentially go full Zimbabwe. They called it the “PIGS” which was an acronym for Portugal, Italy, Greece and Spain.

Since GDP stalls out and the government continues to print money, it leads to consistent asset inflation and wages that don’t keep pace. This is also known as stagflation (assuming unemployment creeps up due to AI or other macro factors like Oil prices).

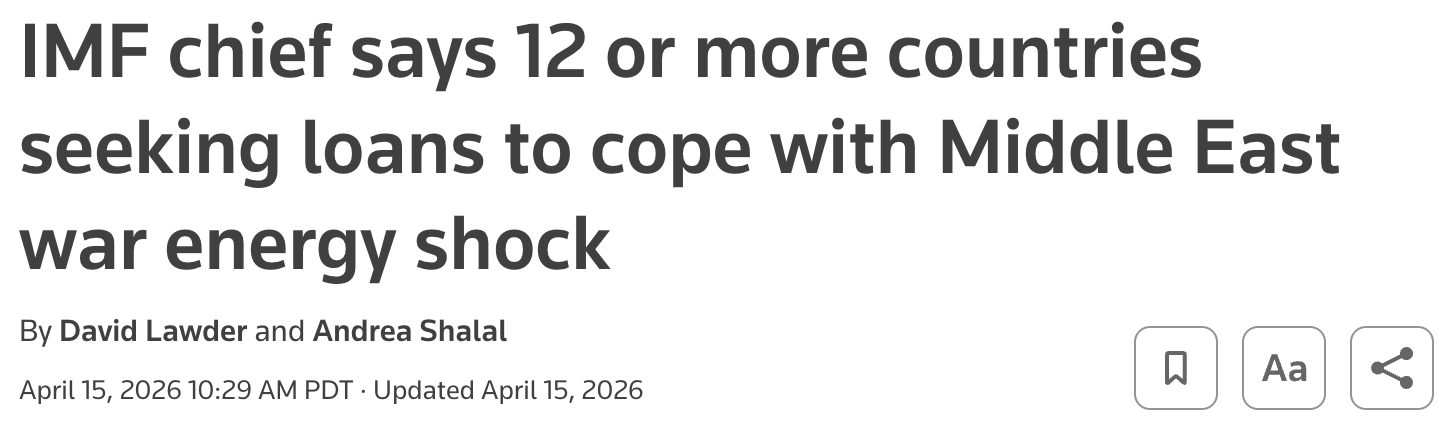

The IMF is already suggesting that pressure is mounting.

Debt issues are not solved, war won’t pay for itself

Add in oil price shock and prices go up

Middle class/upper middle class see a savings rate decline ← extremely important

Asset owners win as people are barely surviving and saving less. They still need to spend to survive and those profits go to the same people

For those that are new here, wealth is always relative. If everyone in the USA is gifted $1,000,000 it means that the median American would have ~$1,200,000. This would also mean that the quality of life for the median American is unchanged.

Put That All Together: If the typical upper middle class person was saving say $20,000 a year which was 10% of their income. If prices go up across the board and they are saving $10,000, it means their savings rate is now 5% which represents a 50% reduction. If that same person had a net worth of $200,000, it means their net worth only increased by 5% instead of 10% (saving $10K instead of $20K).

On paper they have “more savings” but with inflation at 3-4% they have realistically stagnated (pun intended). Working a full year only to be in the same spot on a relative basis.

What Happens Next

At this point debt becomes the decision maker. Rates are too high to push off payments (where they don’t hurt spending) and the interest impacts purchasing decisions.

Where it Shows Up: At a company level, you’d see this at the profit margin line for any non-essential company. Coca-cola and Costco are not going to see much of a change. People need to eat and drink.

However, if you see profit margins slimming out for automotive, apparel and non-essential services slimming out? It means that we’re officially in a period of prolonged stagflation.

As of April, this isn’t really showing up. Oil prices have only shot up recently and much like any commodity price increase, it’ll show up after a full quarter or more of pricing pain (majority of major companies have hedges in place)

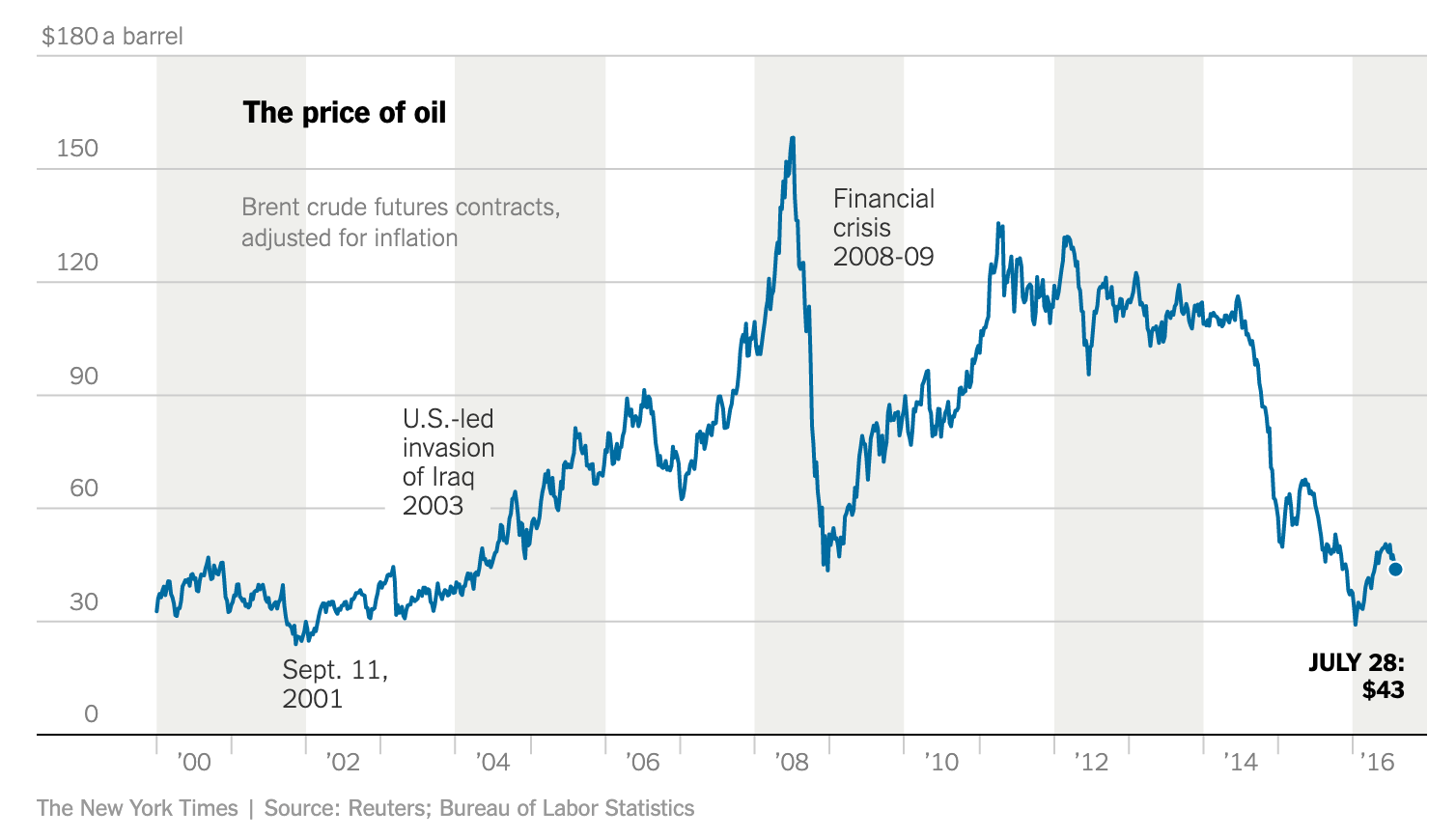

From the chart above, you can see how quickly a big price rise can impact the broader economy (especially the levered companies/individuals)

How to Prepare

If you think this is a viable “slow grind” headwind, then you’d want to focus a lot more on creating a variable expense structure + unlevered portfolio. The way to do that is to keep a much higher percentage of your spending tied to things you can control. Not the time for a large mortgage, car note or fixed expense line.

While that one is easy to see, the opportunities will also be missed by 99% of people.

Opportunities Pop Up: You’ve seen all the headlines. People aren’t drinking as much. Looksmaxxing is a new mega trend. Big dispersion in have and have nots. The signal amongst the noise? Will show up in the middle to second half of this year. You are already seeing the search results trend and it’s up to you to capitalize. Examples in this post:

BTC Quantum Drama, Niche Brand E-com Economy and More

Welcome Avatar! We’re guessing the majority of you guys are tired from doing all your taxes. This post is written in a way that it can be read later. If you’re filing just before the deadline we don’t blame you. This year seems to be going a lot slower due to all the geo-political stuff that has happened. Our guess is things are more interesting late su…

As usual, none of this is a guarantee. Although we do think a period of stagflation is more likely than a period where prices suddenly drop 50%. We had that chance (of a deleveraging) during COVID and learned that the government prefers to just print money.

Investor Psychology + Repeated Thinking

One of the interesting things we noticed over the past few years is the concept of “history repeating”. After we got out of the lock-down (COVID) people were fear mongering for another pandemic in 2023 and 2024. This makes no sense statistically as a pandemic typically occurs once every 100 years or so. Repeating it again within 24 months makes no logical sense but it was a common belief.

This is similar to real estate prices crashing after a major natural disaster (earthquake, huge storm etc.). The chances are massively lowered once the event has passed since it is a one in 20, 30, 40 years event.

What People Think Now

Right now the vast majority are in two camps: 1) some sort of massive deleveraging issue where real estate goes down 50% again like in 2008 - unlikely due to locked in low interest debt + completely different guard rails against bad loans and 2) some extreme money printing environment where everything goes up in some massive Zimbabwe/Argentina up only 50% move. In this case you want to own risky junk like the scooter company craze in 2021.

Masses Are Typically Wrong

While there is always a chance they are right, the vast majority of the time they are incorrect. You can see this as they underperform basic index funds and consistently get emotional (in the wrong way).

If you read between the lines? Then it would create a scenario where both parties are wrong. The group that says we’re going back to the stone ages with a -50%? Not happening. The people who think alt season is coming (despite no ETH ATH in sight) are also wrong.

Leaves you with a in-between solution. Prices go up slightly but not enough money gets sent into the middle class to spend money. It gets consolidated into the winners. Good assets that are needed go up in value. Middle gets squeezed. Deleveraging only seen in low quality over levered industries.

In that scenario the masses get cooked, asset owners win, people who take advantage of the spending shift make millions and you’ve got a deeper K-shape spread in 1-2 years.

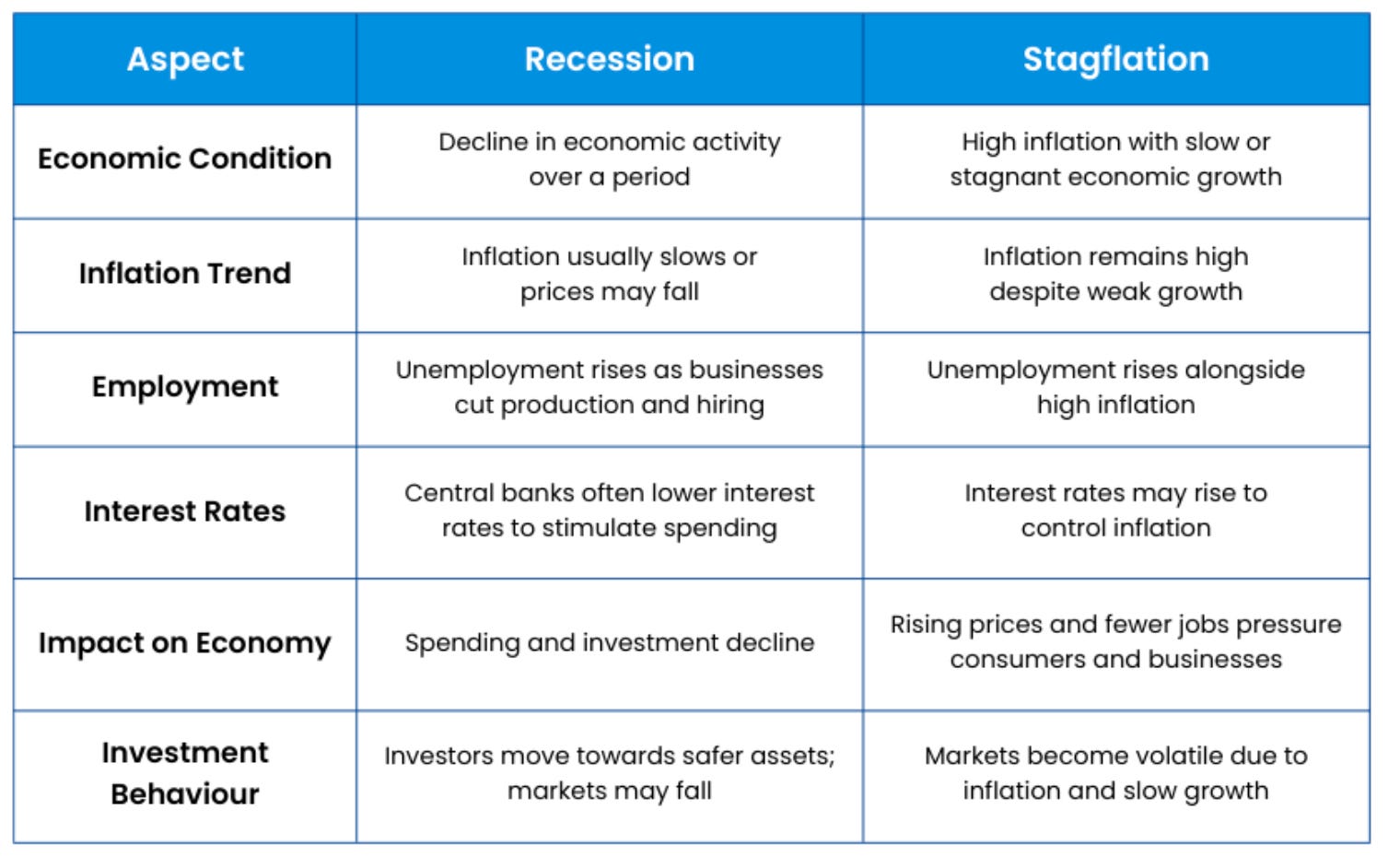

Good comparison chart to decide what environment you think we’re in.

Summary

A slow squeeze is looking more likely if people can hold onto their low interest rate debt (people locked into <4% mortgage notes). It also becomes more likely if inflation remains in the 3-4% range.

Fortunately, you live in the best time in history to be alive. All you’re going to do is follow all the social search trends and figure out what products people are shifting to. If they are trading product A for product B, you’ll know at least 3-6 months in advance.

Meanwhile? 99% of society won’t even try to spin up an LLC. Not once.

Disclaimer: None of this is to be deemed legal or financial advice of any kind. These are *opinions* written by an anonymous group of Ex-Wall Street Tech Bankers and software engineers who moved into affiliate marketing and e-commerce.

Old Books: Are available by clicking here for paid subs. Don’t support scammers selling our old stuff

How ETH is Staked: Covered (here)

Crypto: The DeFi Team built a full course on crypto that will get you up to speed (Click Here)

Crypto Taxes: We have a suggested Tax Partner and 25% discount code, for information see this post.

Security: Our official views on how to store Crypto correctly (Click Here)

Social Media: Check out our Instagram in case we get banned for lifestyle type stuff. Twitter will be for money