Personal Finance Planning and Avoiding Mainstream Calculations

Level 1 - NGMI

Welcome Avatar! Today we’re in a bit of a personal financial planning mood. So. We’re going to outline some mainstream things that can get you into deep trouble. In particular, your 401K is not going to do much for you long-term (if your goal is to “make it”). Yes we’re well aware there are various other vehicles like ROTH products as well. This is simply nit-picking at the bigger picture which is this: you will need to plan over decades and do the opposite of your peers.

Part 1: Understand the Earnings “Bell Curve”

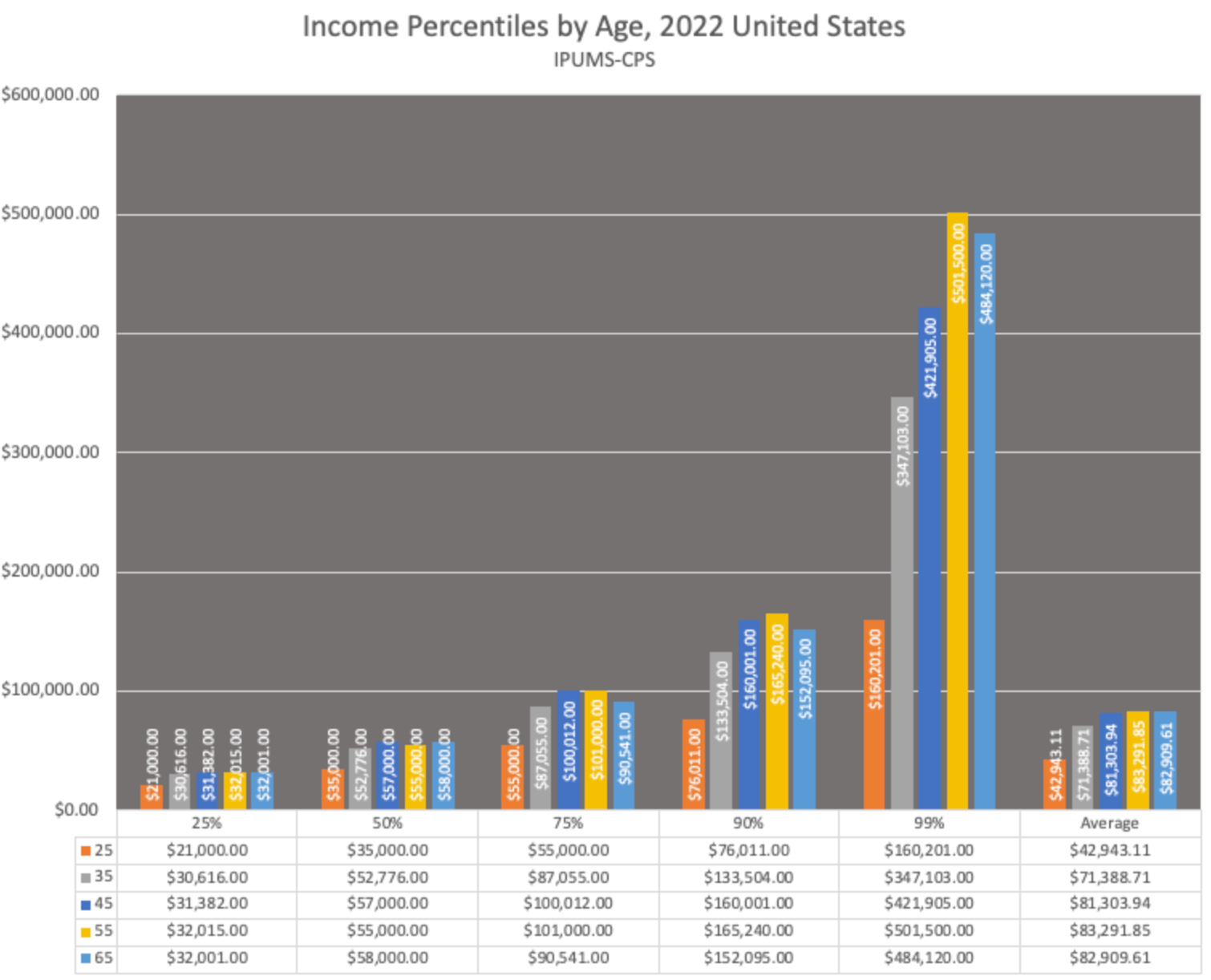

No this isn’t about the IQ meme on twitter. It is about the actual historical facts related to earnings. While our audience isn’t going to represent the average (far from it as it skews 2-3 standard deviations up while the masses are looking at lambos and celebrity gossip), the trend is the same.

Here is the rough direction in terms of money: 1) you will peak earnings 35-45 range, this even includes high earning people, 2) the lucky few who make more past 45 are extremely elite and likely tied to future exits at an earlier age - IE. income from a $10M exit at age 35 is going to generate significant earnings and 3) average length of life is around 76 years with 80 being a good benchmark if you’re taking good care of yourself (in the end a lot of life is luck - car crash, sudden illness undetected etc.).

Most people will stop there and conclude that “okay I should prepare for flat to down years after age 40s since my priorities will change to focusing on kids and other life events”

Fortunately, you’re on this side of the web so you can go ahead and look at the second derivative or second order effects. The first one being, LTV of earnings.

Life Time Value (LTV) of Earnings

As long as you’re putting in the time/hours to improve your skills/talents/customer base you don’t have to worry too much about increasing earnings from your 20s to 30s. It is extremely unlikely that you go down in terms of earnings power. The part that maters? Elongating the tail.

If you are a high earning person in your mid 30s you should start to think “okay as I begin to peak how do I prevent the curve from going in the wrong direction. Or. Potentially to zero due to standard corporate downsizing”

First work strategy. You need to be a *high ROI* person at the firm. Most people still work W-2 positions and everyone has to start somewhere. The trick is to avoid the following: 1) don’t leave the profit center and 2) don’t worry about fighting for an extra 5% on your bonus.

While this is counter intuitive as your co-workers will beg and plead to get a boost, they are lowering their operating profit to the firm. If you are making the firm $1M per year and suddenly you’re making them $900K then $800K, you’re digging your own grave. Eventually, you will generate say 15% operating margins to the firm who is printing 25% margins on their quarterly earnings calls. Guess what? You can still get cut and get cut quickly if you are not meeting corporate margins. Not a smart long-term strategy.

For business. If you run a profitable business and you’re starting to see the revenue flat line, it is time to think through your options. 1) you can significantly elongate the LTV by keeping costs flat - this means you don’t raise price and you don’t lower price. This signals stability and it signals “overdelivering” which prevents people from buying the competing eye-liner product that is 5% cheaper. 2) if you still have the energy and resources, you can expand horizontally. Not through acquisition - rarely works - but through your own branded product into a new category that is most asked about. And. 3) spend *more* on marketing in down turns and spend less in up-turns. We know this sounds crazy since no one does it. That’s why it works.

By capturing market share in a downturn, you retain brand awareness and when the tide shifts in your favor you will collect more than your fair share of the market

Play the attrition game. This applies to both a W-2 and to anything online. Whoever stays in the game the longest wins. Every business is the same. If you simply survive you end up towards the championship table (poker analogy) where even if you’re the #5 finisher you make wayyyyyyyyyyyy more than if you were out 4-5 tables before (even if you only show up to the final table with a few scraps left)

Expand the Investment Percent if You Can

The second major conclusion is that lifestyle inflation is an absolute killer. You will be poor forever if you spend your annual raise on “new stuff” since your savings from the prior year will mean nothing.

Put some math behind it. If you’re earning $100,000 and saving $20,000. That’s 20% and you’re doing just fine.

You go and get a raise to $150,000. And. You continue to save $20,000. That is 13.3% and now you’re saving *LESS* than you were last year on a percentage basis.

In short, you got a raise but you’ve made it harder to keep up with your lifestyle to the tune of ~8 years

What is the solution here? Like most complicated answers in life there are really no solutions that are easy. The one we came up with stood the test of time: 1) get a career in Tech/Wall St./Enterprise Sales, 2) spin up wifi and 3) scale and sell.

Looking deeper into that strategy, the implied message is that it forces you to slowly scale up the savings percentage.

There are now 50+ people earning their entire annual spending online as cartoons (ranging from BowTiedOx to BowTiedPickle to BowTiedDevil). What this means is that they can have a 50%+ re-investment rate while they build their long-term exit plan. Think that through.

We don’t really care if your goal is to live off $5K a month or $50K a month. Being able to save a year for every single year you work = pulls in decades of effort.

Scale Scale Scale: As you can see the game is rapid scale. If you’re moving the percentages fast and stay calm during the up-turn you’re getting decades back. Not a year or two but an entire decade or more without having to clock in for the ole’ W-2 ever again.

Save Those Big Years

We’ve written this for years now. If you have a big year (exit of $500K for example) or you have a big year earning say 2-3x what you usually make in a year… You better save every single cent.

While you will *likely* have good years in the future, the probability declines the older you get. Generally, you will have your big earning years in age 35-45. Call it about 5 years will be “banner” years earning you more than you imagined possible.

Note: before getting hyped up about this. Around 10% of people will earn top 1% income for a few years in their life. That’s right. They get to the top tier earnings but the vast majority do not SUSTAIN. This is why you have to stay humble if you have a couple of good years.

As a bonus, even though this has been a clear message for years, there is no chance anyone listens. Some sort of simulation game where everyone has to learn the hard way and go through max hedonism and bad decision making at least once.

Plug in the Lump Sum: Say you have a big year and were previously making $200K and suddenly make $1M. This is a huge 5x. If you swallow the ego and were previously saving $100K a year, you could save $900K (using everything post tax to make it simple)

Ta Da! We’ve now now gone from 36-44 years of working. To 16 years with a side hustle (being a smart person in the Jungle is good enough) to now… 9 years assuming you have *ONE* success. Just one.

Conclusion

For those of you in peak earnings (mid 30s to late 40s rough range) start to think about elongating the tail. If you’re earning a ton it makes more sense to manage the top-line vs. pressing for more and more (once again this is playing the probabilities)

Your raise is *not* a raise if the percentage of total earnings declines. IE. if you earn $200K then $400K but you save $100K each year, you’re rolling the ball back *down* the hill. Not up the hill.

If you have a banner year, save every penny for the first one. Banner years come 3-5 times in a lifespan for 99.99% of people. Feel free to point out the pro-athletes, celebrities, Jeff Bezos etc. of the world. They are not the probabilities.

In the end, 99% of people will still blow the money since we’ve never seen a single person avoid the hedonism stage

Part 2: Mainstream Calculations are Wrong

As always. The mainstream is run by major corporations. Major corporations want to drain all of the value out of every single employee. “No basis point left behind” on the net margin!

Retirement Calculation: When you look at all the calculations we put in there, the biggest misunderstanding is the “now” value. If you get $3M now that is not the same as $3M in 2053. Not even close.

However. The Mainstream will tell you that you need $3M to retire. Uhh that is based on 2023 values. 2023 values are not going to buy you the same stuff in 2053. The only way it would is if we live through 0% inflation for the next 30 years straight.

Highly unlikely.

Retirement is Usually Taxable: No one knows where tax rates are going to go. Taxes become big portions of your planning as you get older due to: 1) estate planning, 2) trusts and 3) state/federal tax etc.

We’re not going to go through all of the issues but you can all but guarantee that your 401K or even roth 401K has “tax risk”. The rules could change and the tax rates could change. Just assume that the money is worth less than the number you see in your account on a day to day basis.

Your Home Isn’t Net Worth: This is going to absolutely enrage anyone involved with real estate in the lower bands of wealth since the majority of their wealth is in their home. There is just one problem with housing, where else are you going to live?

You can become homeless like us and live in a tent but for most that is simply not a viable option. Instead of viewing your *personal* residence as part of your net worth view it as a “return” profile on your savings.

Example: Joe owns a $500K home outright, he would be spending $3K a month on rent for the same place but instead he pays $500 due to taxes and maintaining the property. That means $2.5K*12 = $30K. $30K/$500K = 6%. Since the risk free rate is 4-5% it is practically impossible to lose money on this deal *long-term* if you stay for a decade plus.

Example 2: Kevin pays $6K a month on his mortgage and $6K would have gone to rent. This means the only value he is getting is the equity accrual on each month. Since the mortgage is 30-years this means it will take about 16 years just to get 1/3 of the principal paid down!

If Kevin loses his job/income he is in a dire situation. If Joe loses his income, he’s still good to go for a long time.

Additional Nuance: If you have kids and say you live in a 4 bedroom place, you can certainly say about half the value is part of your net worth. After they leave and live on their own, you can easily downsize to a 2bed and 2bath place.

In that situation, it’d be fair to say *part* of the Equity has value since you’re going to downsize.

Note: before the fight begins, notice that most wealth surveys tell you *don’t* include your primary residence. This is because those reports recognize that the rental properties net you actual income while your primary residence is just a lower expense outlay. In the end, it still costs you money in tax, insurance and maintenance.

Ready for the Flame Thrower

Now that we’ve certainly stirred the pot with how the mainstream teaches you to be locked into place (heavy mortgage and inflated net worth predicated on the 401K), it’s up to you to decide how you want to plan out the future.

You can either start building an income now to offset your living expenses or play the 1/100 odds you move up quickly in the corporate game to a 1% income for 10+ years.

Best of luck anon.

Disclaimer: None of this is to be deemed legal or financial advice of any kind. These are *opinions* written by an anonymous group of Ex-Wall Street Tech Bankers and software engineers who moved into affiliate marketing and e-commerce. We’re an advisor for Synapse Protocol 2022-2024E.

2017-2020 Old Books: Are available by clicking here for paid subs. Don’t support scammers selling our old stuff

Crypto: The DeFi Team built a full course on crypto that will get you up to speed (Click Here)

Security: Our official views on how to store Crypto correctly (Click Here)

Social Media: Check out our Instagram in case we get banned for lifestyle type stuff. Twitter will be for money. At 10,000+ Instagram follows we will publish some city guides ranking each region we’ve been to.

I consider the idea of “done by 40” as more of a “the snowball should be well on its way, giving you flexibility” not “must hit number by then, never going to make another dime after that point.” In fact, seems like if you’re doing things right, the likelihood of real hockey stick moments occurring after 40 are high.

But all of that is predicated on 1) having built the foundation, skills, networks up to that point and 2) the fact that you won’t be serving gelato in a beach town somewhere

Thank you Bull, its nice to hear that the best is still to come. Been stressting over scaling my wifi biz and getting frustrated but its nice to know that good times are *likely* ahead