Sequence of Returns and Investor Psychology Insights

Level 2 - Value Investor

Welcome Avatar! If you’re interested in maximizing your quality of life, this post is for you. We know all the mainstream stuff about 4% withdrawal rates (blah blah blah 7-8% compound blah blah). That said, sequence of returns matter a lot. You can also use this to manufacture the best outcome when you exit the W-2 world. While this will apply to older generations, it does apply to younger ones if you’re close to the classic ***2x W-2 net income = biz income*** resignation point.

Part 1: What is Sequence of Returns

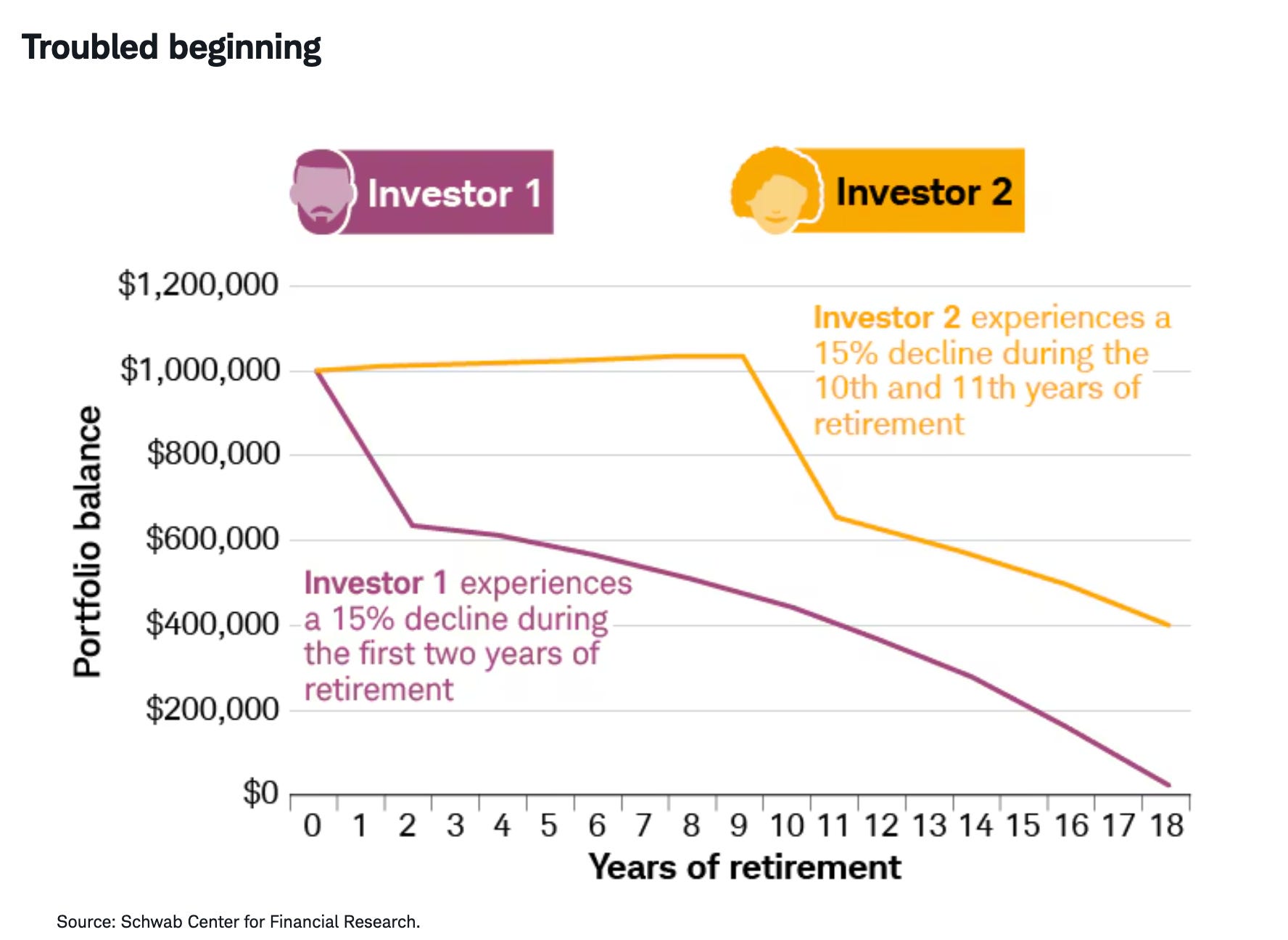

Simple Explainer: Sequence of Returns represents the risk that you stop working and suddenly there is a big drawdown. As you can see from the above image from Schwab, it can significantly impact your future, looking at years of pain. This is because a 15% decline would take a 17.65% return just to get back to break even. The problem with living off portfolio returns alone is that you are still selling to cover living costs.

Concept for W-2s as Well: Outside of starting your own biz, if you’re going to keep a career for the long-term you want the math to work where you retire/get let go during the first round of cuts (in a bear). This is because most high-end white collar work will pay you out around a year of income if you had long tenure and played the politics game well.

Mathematically, a single year of income is probably more than 2 years of income. You’d see a drop in living costs, market is down but you don’t even need to touch the portfolio.

Big Picture, no matter who you are you want the numbers to math out when markets are in a down year, not a big up year. Most do the opposite and psychologically anchor to their peak net worth, end up taking more risk. And. Blow up!

Markets Are Not Linear

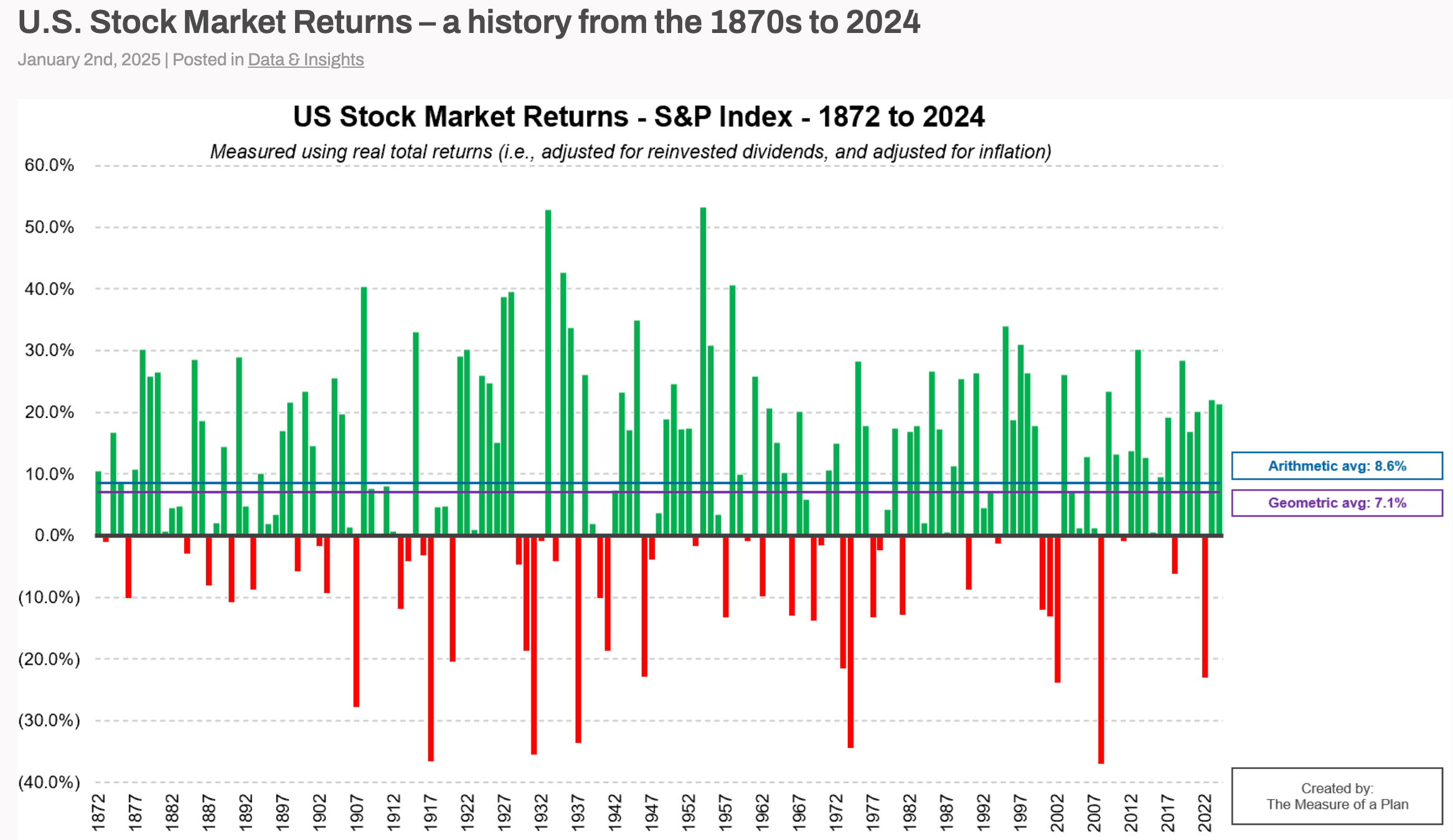

Since birth you were trained to think linearly. 4 years high school, 4 years college, 3 years investment banking analyst, 3-4 years associate, 3 years VP…. so on and so forth. This isn’t how the real world works and isn’t how markets work either. From the above you can see there are always big down years over a decade.

You don’t need to anchor to “quit in a -30%” however, quitting in a minus -10-15% is much safer.

People in this situation: 1) they didn’t fail to invest, 2) they didn’t invest in vapor, 3) they didn’t take massive risk. They didn’t think of sequence of returns. Average returns are largely a meme because your time horizon is no longer “60+ years” it is shorter “a couple of decades”.

Another way to think about it. If you’re grinding through the down years, you’re buying tons of shares that lower your cost basis. The years markets are up big? You’re actually raising them. Structural problem.

Would you rather die rich to create trust fund babies or worry about last second medical bills?

Time Based Thinking

Beyond the emotional structure of investing (the most important), learning to think in terms of time frames is much more valuable. Looking at averages is lazy. If you see multiple -10%, -20% or even -30% when looking across decades, that means there are +20%, +30% years as well (to get the average 7-8%).

“If I pull 4% per year, I’m fine.” This only works if you’re exiting at the middle, not at the top or bottom.

Quick Example

Someone ends up with $4,000,000 and plans to pull $160,000/year

On paper, looks reasonable. Now the market drops 25% in the first two years. A million has vanished when they ***should*** to be up “$320,000”.

They must sell to cover costs and they are gone forever

If markets recover the next year at +20%, it doesn’t matter. The units are gone

Now your baseline 4% goal of $160,000 is gone likely a minimum double digit decline

When you’re living on earned income “stable” paychecks, the crashes are a gift. Exact opposite happens once you go solo. Mike Tyson punch of declining asset values and selling pressure.

The wild part in all this, is you don’t need to plan that far ahead. Just look at asset prices and ask if it has been up for about 5 years. If that’s the case and we didn’t just get out of a downturn, you’re better off playing the time game and manufacturing that 1-2 year of additional buffer.

Create Economic Flexibility

Want a yacht? A Super Car? Cool, best to just rent.

The math will help you a lot. If you plan on going a stretch of time (retirement, sold a company etc.) without earning a lot, you want more variable expenses than fixed overhead. Skip the vacation home and you don’t have a recurring tax, insurance, maintenance, utilities overhead. You probably want flexibility in where you go anyway.

Boats, vacation homes, luxury cars = Rent

Buy = primary forever home, reliable car

Spend out of bond/utilties/boring stock portfolio - adds even less pain in down years as they are down less

Flexible spend comes out of stocks, crypto and rental income from properties (rentals mainly due to tax benefits)

Behavior matters. Allocation matters. Time frame matters. If assets have ripped matters. Overhead matters. The rest is actually much easier to ignore vs. the boring “i’m good at X% withdrawal rate”.

Think About Changing the System

When you’re in growth mode you don’t care much about downturns. No one building a company, jumping up the corporate ladder or living life on full blast has any interest in prices today. The old system was “maximize long-term returns” in the new system you’re looking at “probabilities of survival”. How many ugly years can you survive vs. how many decades of compounding do you have.

Structure It As Follows:

If you took a random dead beat job, how much of the “safe” withdrawal can you offset. You already have the numbers, if you could survive about 20% of the stated withdrawal that’s healthy

How many uncorrelated income streams do you have built in: real estate, stocks, tech stocks, crypto, bonds and anything else you own that isn’t in those five main buckets

How much is variable spending baked into your costs? Higher is better. If half your costs are actually variable and unnecessary, you’re 2x as safe as you think

Instead of worrying about average/median returns, think more about time based returns. It’ll serve you well considering economic cycles are 7-10 years in length.

Part 2: Now Onto Application of This At Any Age

We’re guessing a large chunk of you are saying “doesn’t matter i’m not retiring soon” or “I haven’t sold a company yet”. While that might be true, you can figure out a way to manage your own cash position intelligently.

Each Year Increase Percent to Cash: This served us well back in the 2010s. If you’re in a bull market and know it, what you can do is slowly increase the cash position. We’re not saying that you go all out or all in every 7 years.

Instead you can create a smoother return line.

If a bull market started this year (it isn’t) but if it did, think about it like this.

Year 1 you’re putting $5K a year into cash

Year 2 you’re putting $10K into cash

Year 3 you’re putting $17K into cash

Year 4 you’re putting $25K into cash

Year 5 you’re putting $35K into cash

Year 6 you’re putting $45K into cash

Year 7 you’re putting $50K into cash

Flat-line here and wait for bear

If you do that, then you simply set yourself up to actually buy the dip. Since we know that every single up year = chances of buying the top, that means you’re changing your cost basis slightly. Then you see a -10-20% year and you have a double win: 1) you can lump sum buy more than you were in years 4-5 and 2) you have an amount you were already buying every month anyway.

Congrats. Simple solution to hit singles and doubles without a complicated sequence of return risk in your net worth.

If the market hits 100 (just a number) and you see -20%, that means you’re getting significantly more shares. Likely more than you were getting in year 4. Roughly speaking, you’ve purchased shares in the past (that’s the concept)

Each Year Test More in Downturns: On the income side of the equation, you should actually test more of your ideas in a weaker economy

Several reasons for this: 1) ad costs likely lower, 2) people quit opening up more market share and 3) if you’re making your first $100K a year in a downturn, what happens when things go up again and you’re the new shiny product? You guessed it, likely making $200K off your idea

Most don’t do this. They think it’s a good idea to start something when things are hot. Makes little sense. When things are hot consumers do no look for new alternatives/products. They stick to whatever they were doing since it “doesn’t matter”.

Downturn = market share shift. If you have a product that fills a gap in the market, you’ll make multiples when it turns.

Anchor to Percentages and Fixed Costs - Diminishing Sensitivity

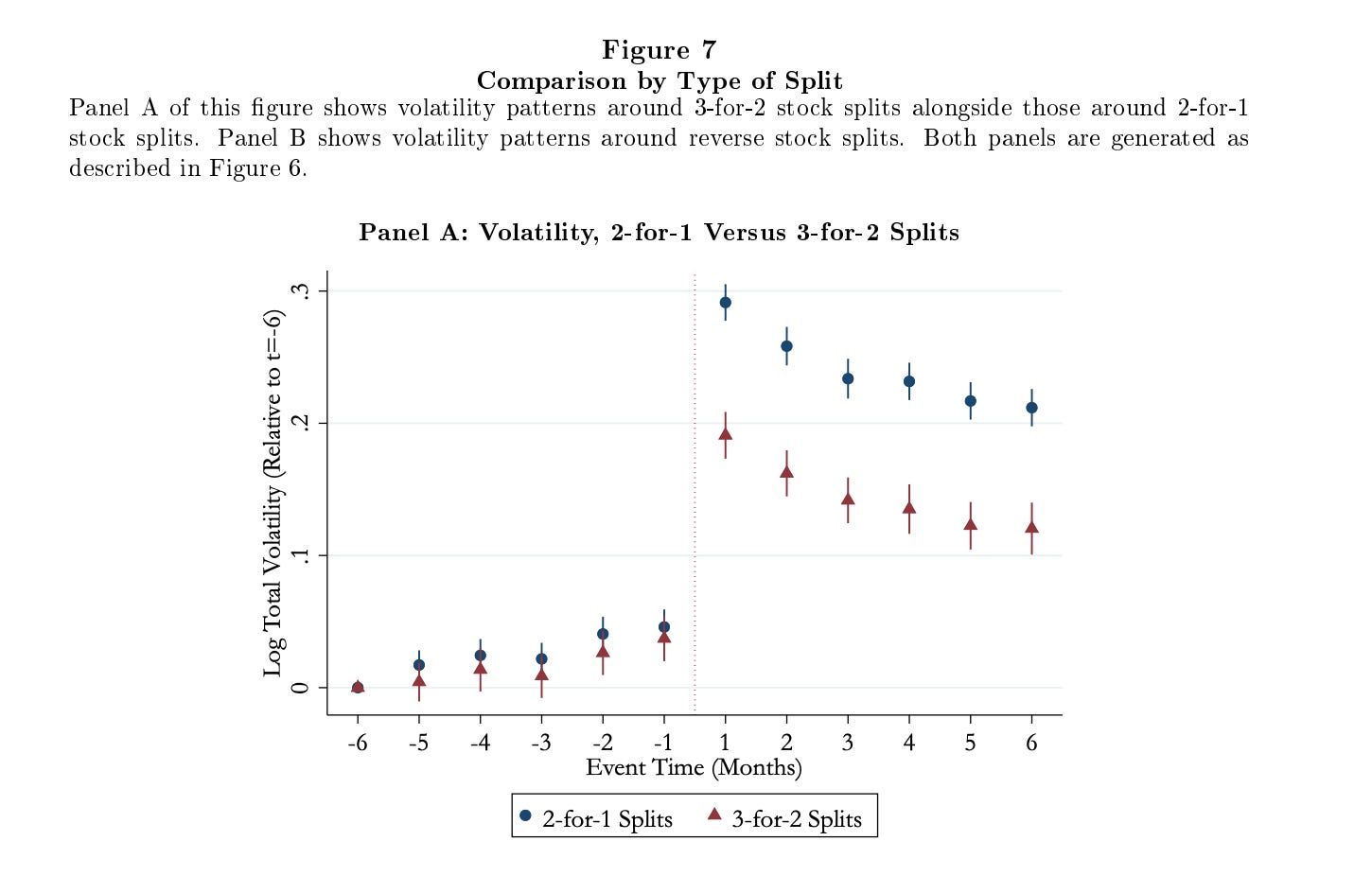

“Can the Market Multiply and Divide? Non-Proportional Thinking in Financial Markets” - Kelly Shue (source)

This isn’t a study made by a famous investor. However, it’s a good one to read if you have the time for it.

Summarizing it, the vast majority think in dollars, net worth and nominal changes. This is why one of more infamous comments “wealth is relative” makes people so upset. All these calculations for $1,000,000 without considering what it’ll buy later and what it means to be “rich”. Rich is more of a percentile game in net worth not income or dollars. (Again. Top 1% wealth can generate top 1% income without working!)

You actually see this in markets as the paper shows that low priced stocks react bigger to news vs. high prices stocks even if you control for market cap! It is massive. If the price doubles (nominal, not market cap fully diluted etc) the volatility actually drops!

If the majority of people thought in percentage terms, the moves would be similar. In fact, they went as far as to show that reverse splits caused percentage changes to go down, IE. clear indicator that nominal is what drives the typical human.

Apply This Today: This is one of the major reasons we stated many times publicly that we need to change the denominator for Bitcoin and crypto in general. If we came up with a new name for a Bitcoin such as “hBTC” (move the decimal twice) it would lead to $704 per coin. The upside and downside here is clear. It would swing more on the downside in bears and swing more on the upside in bull markets.

If you’re young, you want volatility and this would help a ton.

Other Odd Benefit: If you want to lighten up your percentage swings, you would buy assets with higher stock prices (not market cap) during the peaks and you want to buy smaller stock prices (not market cap) during the down years.

This is what the data shows and also explains **part** of the reason for high-beta stocks coming with lower nominal numbers

Extra Bonus: Gotta hand one W out for the bankers on this one. Stock splits actually do help. If your goal is to drive up volatility, split the stock price!

Summary Put It All Together

To put all these seemingly unrelated comments into practice you can actually create better performance as follows.

First, you quit/retire etc during a bear. You want to collect a severance/layoff package at the lows and you want to anchor to percentage declines not net worth if the duration is long

Second, you would want to create a larger nominal cash position every year there is an up stock market year (increasing the nominal every year the market is up)

Third, you can make this even more intense by looking at the actual stock prices. You’d buy more of Berkshire in 2021/2025 than you would of the QQQ simply because the price of Berkshire is huge and is largely a market indicator

Fourth, you would reverse this. Look at beat up tech names in the bear and actually put slightly more money into the lower nominal value stocks - even though it does not make sense

Fifth, when stocks splits happen, volatility will pick up. IE. Options pricing will likely change

And of course the standard: Test more of your WiFi/E-com/SaaS/any biz during ***downturns***. This is when market shares shift and if you’re up vs market in a bear, you’ll be up huge in the bull

Hope this was useful to you guys and again, we suggest reading that study if you have the time. We’re sure the majority will just AI the document but its worth scanning at minimum. Good intro to investor psychology if you can are really jammed for time, then at least go through the appendix such as the figure below!

“Can the Market Multiply and Divide? Non-Proportional Thinking in Financial Markets” - Kelly Shue (source)

Disclaimer: None of this is to be deemed legal or financial advice of any kind. These are *opinions* written by an anonymous group of Ex-Wall Street Tech Bankers and software engineers who moved into affiliate marketing and e-commerce.

Old Books: Are available by clicking here for paid subs. Don’t support scammers selling our old stuff

How ETH is Staked: Covered (here)

Crypto: The DeFi Team built a full course on crypto that will get you up to speed (Click Here)

Crypto Taxes: We have a suggested Tax Partner and 25% discount code, for information see this post.

Security: Our official views on how to store Crypto correctly (Click Here)

Social Media: Check out our Instagram in case we get banned for lifestyle type stuff. Twitter will be for money