The American Dream Is Granted With Equity

Level 2 - Value Investor

Welcome Avatar! The American Dream is actually alive and well. The doomers are always wrong because of one simple reason: they are stuck in the past. Simplistically, you can tell that someone didn’t adapt by how desperately they want to roll the clock back 20, 40, 60 or 80 years. Deep nostalgia = missed every modern opportunity.

If you want the white picket fence, 2.5 kids and Simpsons-style life? It’s actually achievable. The path just doesn’t involve slogging away in a W-2. Squirreling away fractions of paychecks.

Low interest rate debt is also hard to come by. Guess what that means? You’re left with one painfully clear answer: Equity.

Part 1: SpaceX Equity Changed Thousands of Lives

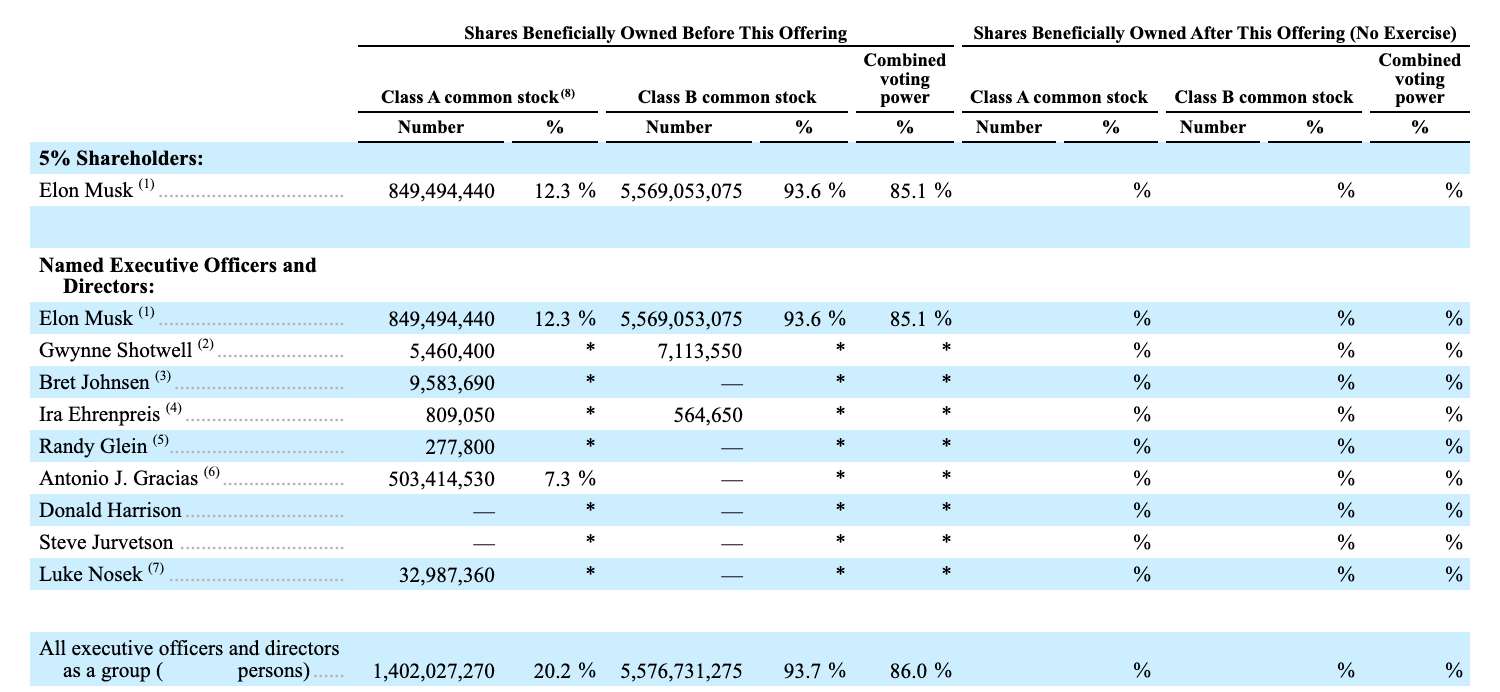

This is the IPO of the year (without a doubt) and thousands of people became millionaires. The estimate was around 4,000 new millionaires and 400 new centi-millionaires. However. That was assuming a rough IPO valuation of $135/share. It’s already trading at $200 so you can imagine that there are more millionaires out there. From a single stock (5,000-6,000 new people and likely 500+ centi-millionaires).

The above paragraph makes Elon look good. Therefore everyone obsessed over the fact that he is a trillionaire. Crabs in a bucket. Anyone more successful has too much and got luck. Anyone less successful needs to work harder. Classic human ego problem.

The bigger picture is that *ownership/equity* just made thousands of millionaires at current prices. The people who owned a small sliver of the Company made more than people working for 10+ years in a time for money exchange.

To put a number on it, a smart employee who held 0.00005% of the Company got to $1,000,000. (1M divided 2T).

The high salary employee who took all cash at $200,000 with a 10% savings rate isn’t getting there any time soon. Their game is linear. Doesn’t work in the age of technology. Completely different convexity.

Don’t Even Get Us Started on The Executives!

What is a Salary For

We’ve said for ages that it is “the rock hammer to get out of Shawshank”. More specifically, you need to think of a paycheck as a survival tool.

The old school personal finance stuff talks about “emergency funds” and “cutting costs”. The reality is that this stuff will not work if your plan is to make it into the top 10%, 5% or 1%.

The salary is simply something you use to cover your cost of living. That’s about it. Once you have your cost of living covered + some amount to shove into a business, you are done with salary hopping. If you can pay all your bills + generate just enough to get a basic demand test/wifi biz up (about $20-30K all in cost), there is no real value in additional income. You need to either 1) build more equity with your own business or 2) get equity in the company you work for - RSUs, etc.

Autist Note: The exception to the rule is if you work for a dying company/industry. In that case you max out cash comp and look to leave for a Company that has secular growth.

This isn’t what most people want to hear. They want to hear “10% raise and you can make it if you keep scrimping by”. The reality is that the tax system doesn’t work in your favor. If you get $100,000 in stocks that grow to $1,000,000 you would owe long-term capital gains taxes on the sale. Or. You could borrow against that $1,000,000 with a SBLOC loan and make the amount even smaller. With a W-2? That entire $100K bonus per year is going to get cut in half in high tax states (NY/CA etc. - where majority of the money is anyway)

If you constantly use cash compensation, you will fight upstream: 1) higher tax bracket, 2) limited optionality and 3) no convexity in a bank account.

Part 2: Seeing How This Helps Home Purchases

“Well BowTiedBull I’m never going to get a $10,000,000 single stock IPO, how does this matter for me?”

It matters a ton. For some reason people think they need to create the next unicorn or manufacture some brand new amazing tech idea. In reality, if you have a couple small wins (say two sold companies for $500,000 then $1,000,000) you’d be in a position of strength.

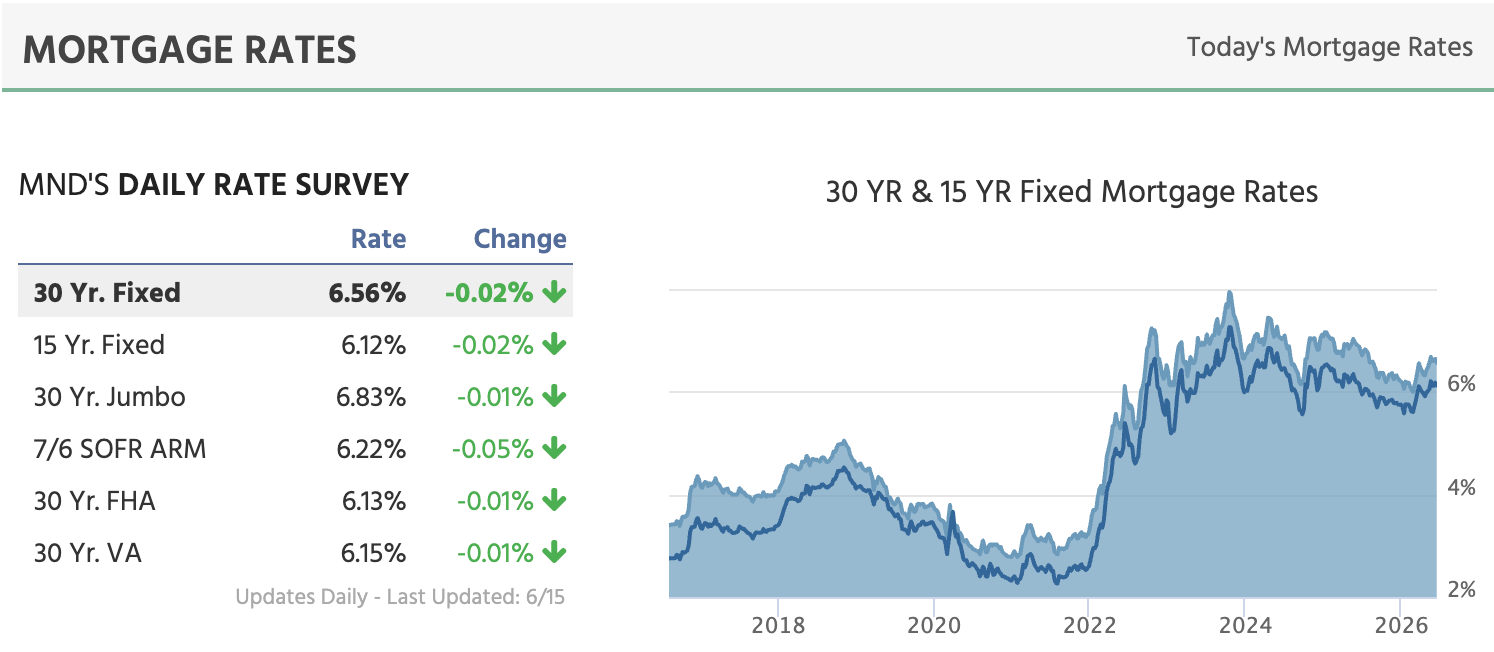

Simple example: You try to look at mortgage rates and see this.

Looks pretty ugly. At 6.5% every dollar you borrow = $1.28 over a 30 year loan. If you borrowed $300K you’re going to pay $380K+ (just interest payments)

Initially, you think, maybe i just sell all of my stocks and cash purchase the house.

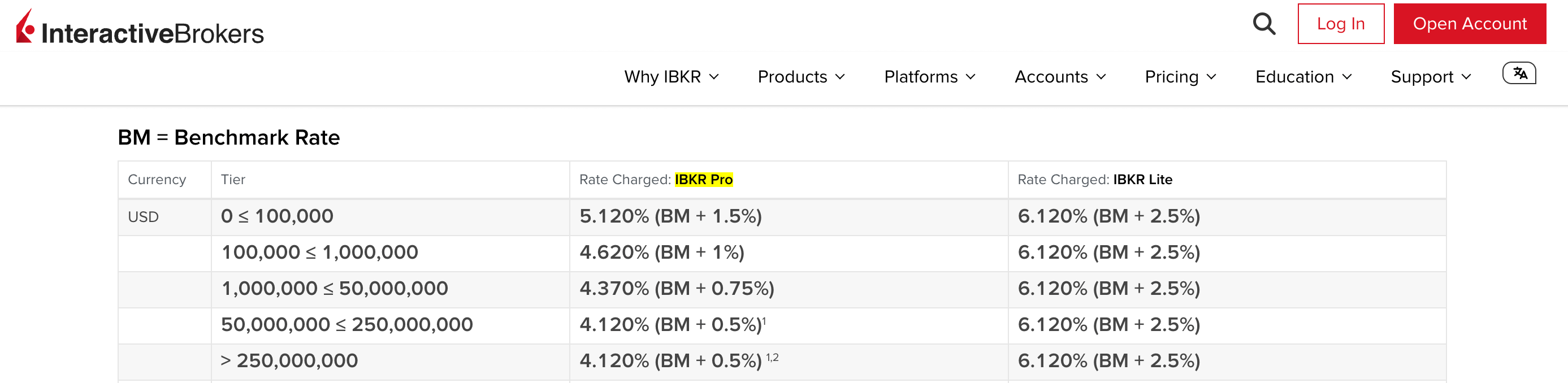

Just before you click sell (and incur massive capital gains taxes), you login to Interactive Brokers and check the interest rate there.

Well you are in the $1,000,000 to under $50,000,000 camp. Looks like you can get about 4.37%. Since you sold a couple small companies, nothing Herculean, your $1.5M is sitting in pretty safe stuff (S&P, QQQ etc.)

Drum Roll: Instead of going to your local bank and getting cooked with a 6.5% rate, you decide to get a bit creative.

Instead of getting a large mortgage, instead of selling everything to cash purchase you do the classic “50/50”. You sell enough to put $250,000 into the house and then you borrow $250,000 against your portfolio at 4.37%.

Now remember. If you borrow that money is still working for you. Take 2026 as the example. If you bought the house at the start of 2026 with a stock based loan, you would owe 4.37% of interest on $250,000, however, that $250,000 in the S&P 500 is up 10%

What if Stocks Go Down: This is the fair and reasonable counter argument, if and only if, you borrow a ton. If you are borrowing $250K against $1.5M, the chances of the stock market going down 66% in a single year is pretty low (puts you at $500K vs. $250K loan). Even if there is a down year (of say 10%), you’d just pay the interest and wait for the market to recover.

Key concept: much like a mortgage you wouldn’t borrow an amount that would make you a forced seller.

Crash Bros Ignore Equity

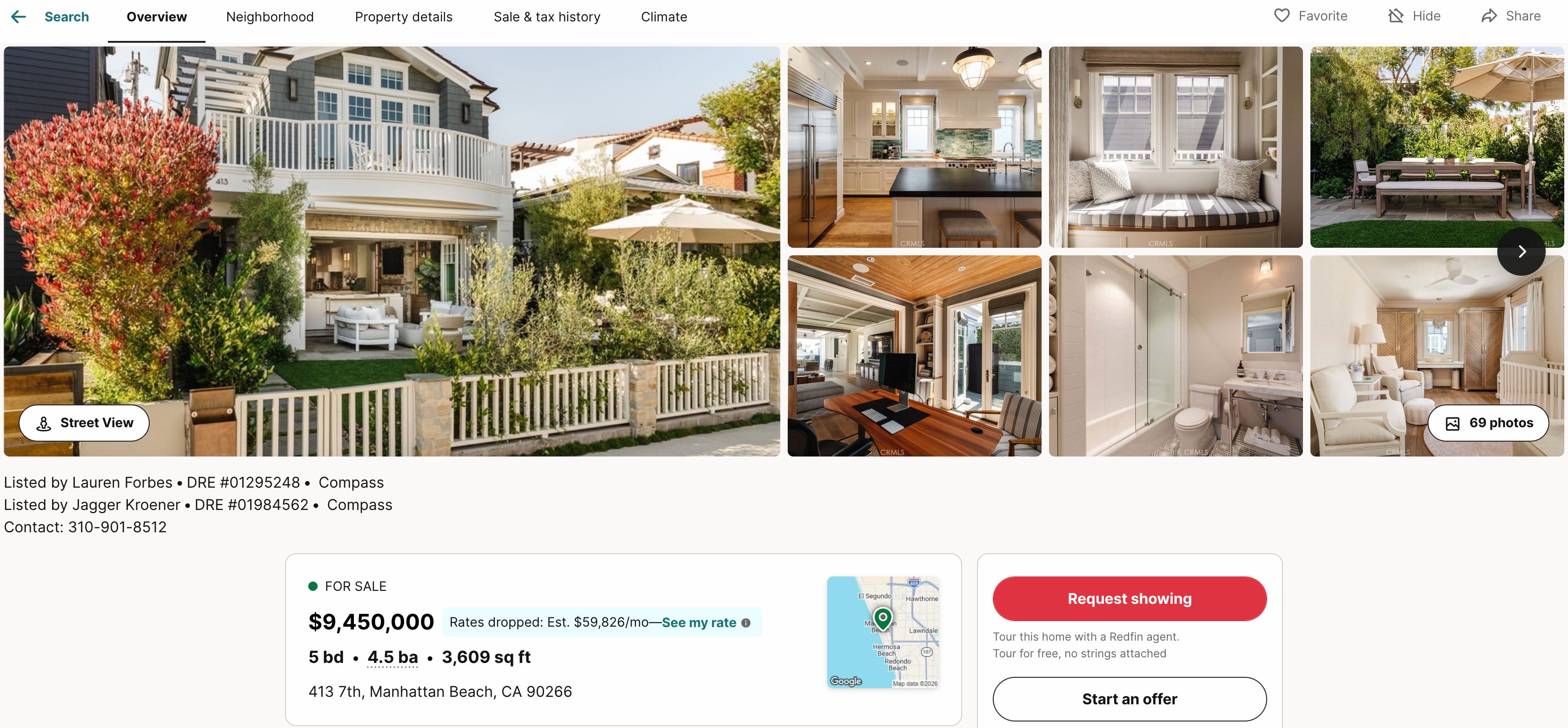

If you want to build on the SpaceX IPO concept, do you believe the Top Tier engineer out in Hawthorne California is going to buy this $9.45M beach house with a 6.5% mortgage from Bank of America? Don’t think so!

Part 3: The Dream Just Has a New Map

Vast majority of people don’t need to create the next Trillion Dollar company. Vast majority will be beyond thrilled with a paid off home and $3-5M liquid.

The irony is that the people who get there (paid home and few million liquid) will over-shoot huge. They end up becoming serial entrepreneurs and create fake games in their head “oh i need more because of 0.00000000000001% tail event of a tsunami in Nevada”

Instead of viewing your “net worth” by a bank statement, you need to come up with an asset statement: Stocks, Vesting RSUs, Options, Business ownership percent, real estate, Crypto and anything else that should go up in the future. The only way to fight off inflation + constant regulation is with assets.

American Dream Is Brighter in Many Ways

You can achieve the classic American dream much faster (completely free of office commute by middle age at minimum). This is due to immense opportunity and wealth in the USA. If you can’t make it here. You can’t make it anywhere. We’re serious.

We know a lot of people who grew up in various countries and the avenues to getting rich in the USA are unmatched. Europe, Asia and little brother Canada have nothing to offer compared to the opportunites in the USA.

The only real downside is that you need to be ruthlessly self aware and laser focused on the next 10-15 years. If you choose the wrong map (going into low margin high competition restaurant businesses for example), you will be playing a much harder game.

Make your long term predictions and stick to them. Ours is on digital immersion, glued to screens, degeneracy, long-tech and talented people having multiple businesses/income streams in the 2030s.

We’ll roll with the Mike Tyson punches as they come. Sure beats following the old path that practically guarantees you end up on the wrong side of the wealth divide.

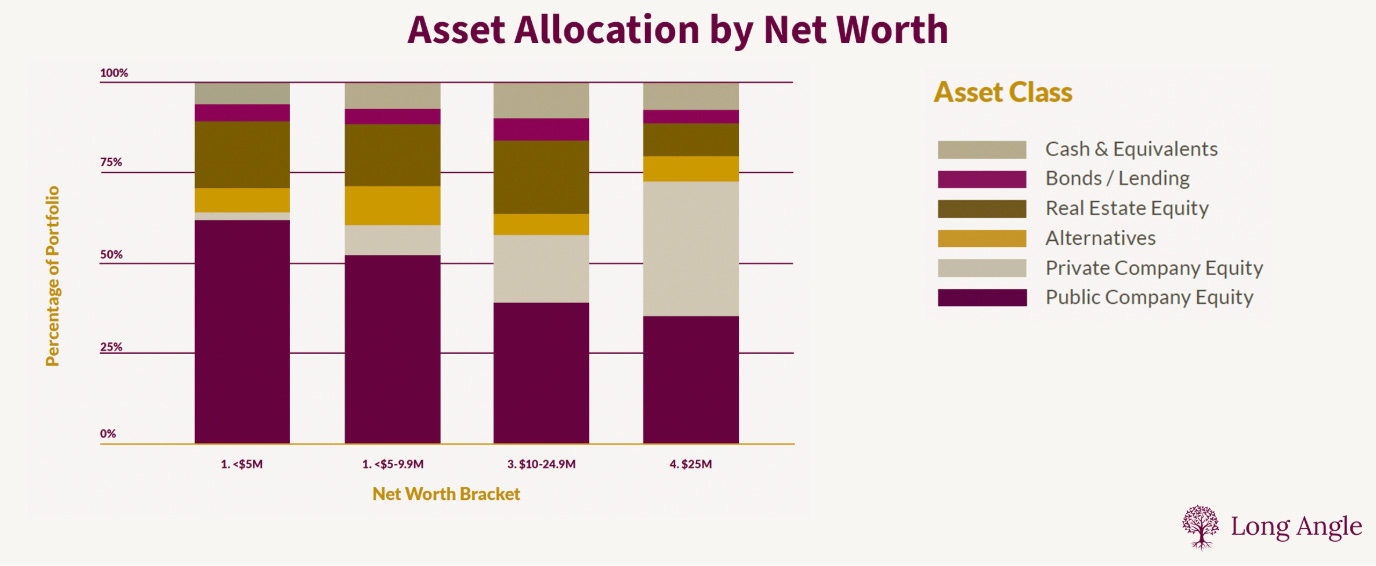

While Everyone Looks at the Hot IPO, Always Look at the Grey Area… Stats are Stats!

Disclaimer: None of this is to be deemed legal or financial advice of any kind. These are *opinions* written by an anonymous group of Ex-Wall Street Tech Bankers and software engineers who moved into affiliate marketing and e-commerce.

Old Books: Are available by clicking here for paid subs. Don’t support scammers selling our old stuff

How ETH is Staked: Covered (here)

Crypto: The DeFi Team built a full course on crypto that will get you up to speed (Click Here)

Crypto Taxes: We have a suggested Tax Partner and 25% discount code, for information see this post.

Security: Our official views on how to store Crypto correctly (Click Here)

Social Media: Check out our Instagram in case we get banned for lifestyle type stuff. Twitter will be for money