The Price of Insecurity: Salary Didn’t Make You Rich. It Made You Easier to Trap

Level 4 - Turbo Autist

Welcome Avatar! As we work through the latest rounds of cuts in big tech and Wall Street “Driven by AI”, you’ll learn that a lot of these individuals didn’t have a back up plan. No. We don’t mean WiFi money. Even worse. They were saving small percentages of their income due to high living costs. This means they believed their careers would extend into their 50s despite all the evidence in front of them (just look at your own office!) suggesting that the majority do not survive for multiple decades.

Part 1: Lifestyle Creep Happens Quickly

Most mainstream advice says “save 10% of your income for life and you’re good”. This is dated. Careers do not extend into your 60s. Highly competitive fields typically die off in middle age (40s). And. It does a poor job accounting for layoffs, one time events, life events and of course inflation.

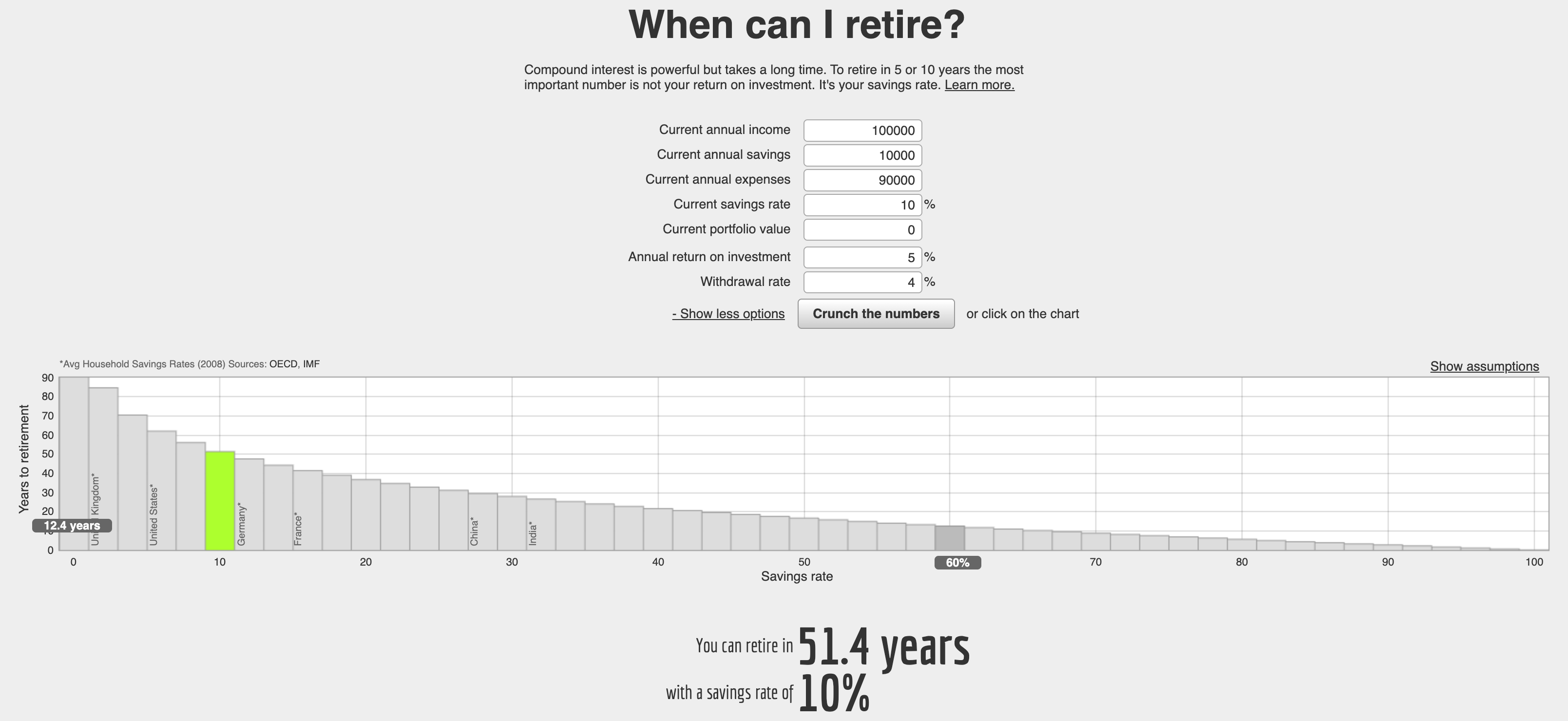

Frugality Guys Get a Kick Out of the Website (Source)

In the new world order, you need an exit event or a high earning WiFi money secondary income stream. Please do not fall down the trap of trying to live on lentils and tap water. Life is far too short. If you’re willing to suffer to that level, you’re better off earning more money and working much harder.

There is a limit to cost cutting. There is no ceiling to earning more.

How the Creep Starts

Now that you understand the standard NPC belief “Save 10-20% in S&P 500 and spend the rest for life”. You can see how the initial life style spending trap begins.

A good phrase for this is “luxury peasant” or “white collar slavery”

In this context a peasant is someone who is entirely controlled by someone else. If someone is entirely reliant on a single entity for money, that’s a one way street. Instead of realizing this, they start purchasing items that make them more entrenched and dependent on the system: 1) luxury car, 2) expensive vacations, 3) private school, 4) expensive watch, 5) country club, 6) luxury hotels, 7) business class flights and 8) anything else that creates ***external validation*** of “making it”

This is a high-stress lifestyle with minimal resiliency. If your burn rate continues to increase net worth remains flat, freedom actually goes down and expectations go up. Not a great combination.

The entire system is set up like this by design. Higher wage/income increases in your 20s. They know most people settle down around 30s. Then they put on the handcuffs as you’re locked down with mortgage, auto and student loan debt (or other types of debt/lifestyle expenses).

Goal of company is complete. Income went up but lifestyle ate it all up. Results in limited savings. That treadmill just went from 5mph to 10mph and you can’t get off it for the next 20+ years.

General Concept

A lot of high earning people develop large egos. They worked hard through college and “deserve” the best. While they earn a lot of money on paper, the fixed costs eat into their ability to really get ahead.

This creates a rough set up. They are *too* dependent on their W-2. Not only are they not saving money, they are too scared to start something else. Worried it might impact their work quality at the W-2 they desperately need.

Part 2: Look at the Quick Math

If this sounds crazy it’s likely due to limited exposure to high cost of living areas. In that case, you’re working remote or you have WiFi money. An outrageous head start. Likely 20% additional buffer room due to cost of living alone.

Either way here is how the corporate grinder sets you up to run on that treadmill forever.

In Your 20s: They pay you around $200-300K. We’re using a wide band because it includes 21 and 29. Some people will be above this, some below. The general “average” over the mid 20s bracket ends up being somewhere in the $230K-$260K range or so.

Your outlay looks like this on a monthly basis.

Rent Needs to Be Close to work: $4,000

Utilities, Internet etc.: $500

Going Out Related Expenses: $1,200 ($300 per weekend)

All Food Related Items: $2,000

Vacation Cost: $1,000

Gym, haircuts, general wellness: $500

Clothing, Weddings, other stuff always comes up: $1,500

Taxes Eat Up about 1/3 of everything (most in high tax states like NYC/CA)

Now you can get to: $240,000 - $80,000 = $160,000 per year.

$13,333 - $4,000 - $500 - $1,200 - $2,000 - $1,000 - $500 - $1,500 = $2,633.

Go ahead and round up and you’re saving around $3,000 a month. Half of that goes to stocks half of that goes to your eventual downpayment on a home.

30s Clamps Come Down: Now that you’ve got about 10 years of experience you should have somewhere around $200,000 set aside for a home. We’ll make it larger and just say $300,000 to adjust for investment gains etc. You’ll see quickly that this doesn’t matter much at all.

Now that you’re in your 30s, living cheap isn’t really an option. You’re stressed out quite a bit and normally people have life events. You also likely went through at least one layoff or extremely rough year at work.

We’ll give a high and generous number of $400,000 as an average here. This is quite good despite what people on X say who think everyone works as an early employee at NVDA or B-lines to MD at Goldman Sachs at age 34.

Some good years ($550K), some bad years ($300K) especially in a recession if no bonuses hit. If this sounds impossible just remember First Republic, Silicon Valley bank and the entire 2008 Global Financial Crisis.

Housing: $9,000 (Plug in $300K down on a $1.5M place and you’re basically here)

Cars + transport: $2,000 typically a large uptick due to more meetings/events etc

Childcare: $2,000

Food + Restaurants: $3,000

Travel Vacation/Weekends: $1,000

Healthcare/Services/Entertainment: $2,000

Clothes/Other: $1,000/month

The big change here is largely the decision to have a family. If you are not in this camp the math changes and you end up being a low 7-figure person in middle age (emphasis middle age).

$400K - $150K for Tax is around $250K

$20,833 - $9,000 - $2,000 - $2,000 - $3,000 - $1,000 - $2,000 - $1,000 = $833.

Whoopsie! Actually saving less money unless we calculate in your mortgage pay down! Now you understand the below table ***completely***

Easy to become house rich and other asset poor for a long period of time (unless you’re one of the smart ones who builds out WiFi money and gets into the $10M+ camp)

Employment Designed This Way: A lot of you will see a big dispersion in your late 30s. We’ve stated that the dispersion is *larger* than what you see post college/post high school. Yes. We are dead serious.

It happens due to the following reasons: 1) around 30 give or take a lot of people get cut as they can’t make the jump in the W-2 world, 2) people who were building a secondary income stream/business quit or become financially successful, 3) life choices to become a parent or not - huge dispersion in where you live, what you think and how your day operates and 4) 15+ years of investment/saving decisions show up - rough knee in the curve for many people.

Set Up For the Majority

By the time most people hit middle age they are making too much money to take a risk. They are sapped of their energy from their 20s that would allow them to burn the candle on both ends. And. Their savings are nowhere near where most would expect them (because most have never lived in high-paced, high competition, high cost of living environments - not a knock it’s just how the math works).

Late 30s hit and the two big separators: 1) deciding if you want kids and 2) if you made the right risks/decisions to escape this general treading water trap.

For those that really think this isn’t possible, even the frugal types (yes Asians are known for being frugal) explain how their own colleagues get hit in this area

The below person went viral a few months back and explained how it works in tech as well. (source).

Mental Metrics to Avoid This

Even if you don’t want to bet on yourself (***shivers in disappointment***), at least go through this general lifestyle creep list and avoid the major ones.

Housing payment should assume your income can take a 33% hit. This could be combined with a spouse, could just be you, doesn’t matter. Make sure you’re not buying based on peak earnings or a big revenue year with a big bonus attached

Assume your car is worth nothing. You can drive something nicer if you want but its not an asset as you have to trade it in for another one anyway

No discretionary items should be financed under any situation. The only time you should finance something is if it is going to increase in value. IE. get a positive return

Monthly burn can increase as you earn more, however, the percentage changes needs to be lower than the income growth. This helps: 1) fund your escape plan, 2) invest to help escape or 3) at least give you breathing room to avoid the constant stress and pressure at work

Spending capacity isn’t wealth. Wealth is when the assets cover your annual fixed spending

Your scoreboard is how much you’re making when you’re asleep. How much equity you’re building and how quickly you could replace your current income. That’s wealth, power and strength.

Part 3: Onto the Implications

Resentment. This is probably the best word we could come up with to describe what we’re seeing. A lot of people are going into a cycle of resentment. Humans place a lot of identity around being useful and feeling valued.

A chunk of the college educated pool were told “just work hard get degree and you’ll be fine”. That’s drying up. In addition to that, the people who were in the meat grinder for a decade or so are realizing the ladder has been pulled up in a ton of industries. They see what is happening. They are being asked to learn all the new tools, do it with less people and send that product to the “big boss” who then earns a multiple of what they are getting as he/she is the relationship manager.

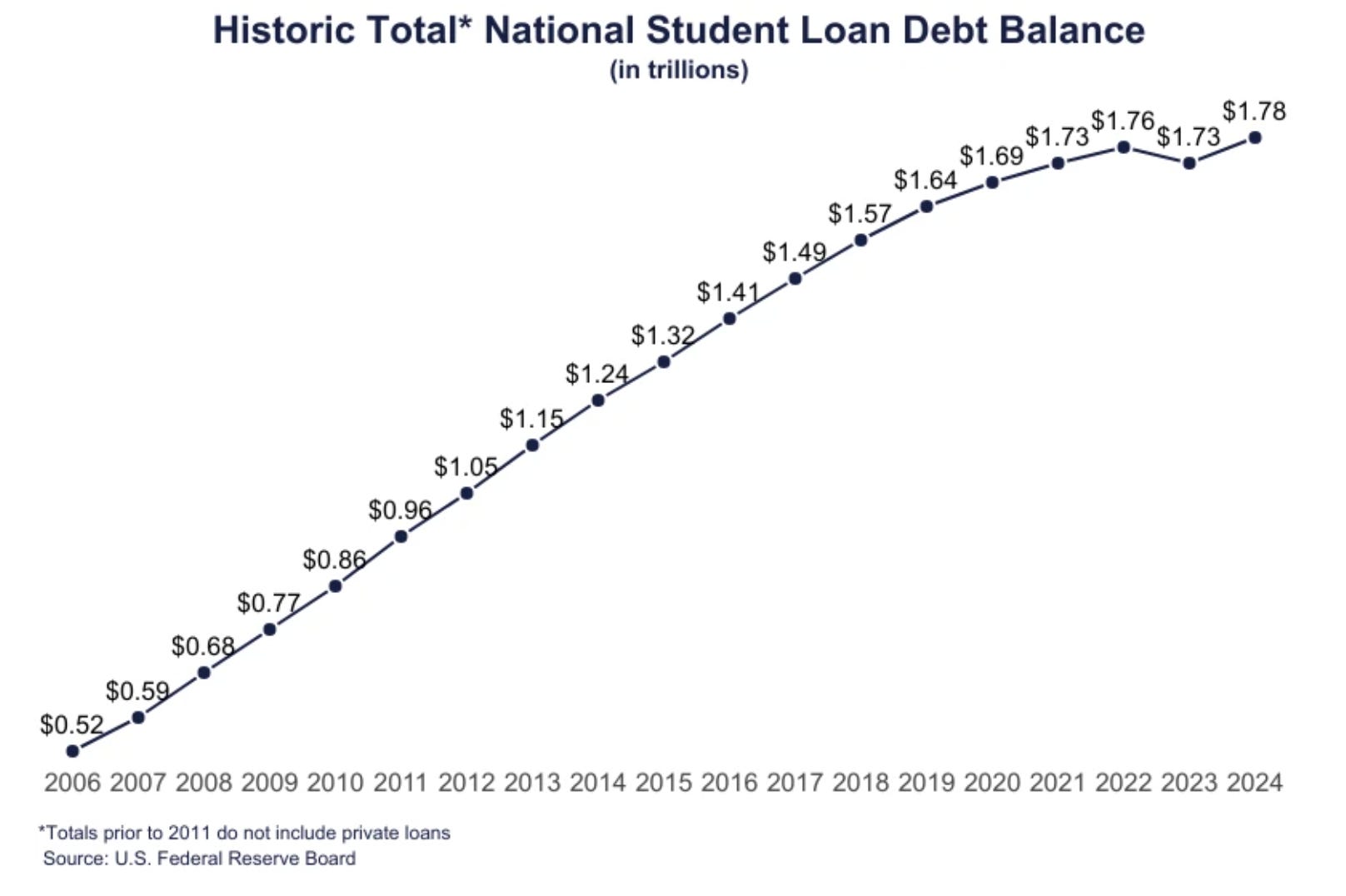

Nearly $2 Trillion Funded this “Work Hard” Mantra

Now that the carrot isn’t showing up for a large chunk of the population and the generation above them is forced to downsize… it’ll lead to even more social isolation.

Move to the Revenue

We’ve been saying this for over a decade, but now it is essentially a survival tactic. You need to get closer to the revenue this would mean

Person responsible for selling the product in sizable amounts - bigger customers bigger sales

Person evaluating the end design and marketing - will it actually be a hit

Deep domain knowledge that will not show up in a search

Those three items will be requirements for survival for the recently cut people making $200K-500K per year. If you’re in that position (currently) you want to steer your career into one of those three directions. Fighting this will just lead to disappointment and despair.

Value Shifts More to…

Hilariously? Office politics. If you thought that AI would make it easier to pick out the producers, it’ll probably have the exact reverse impact. The person who is most likable and most personable within the firm will be seen as a future revenue generator. Besides, if the head of sales loves the guy, it likely means he will be likable to the same clients they speak to on a day to day basis (logically this adds up a lot better vs. someone who was “super fast and error free in excel”)

This also shifts a lot to the looks-maxxing trend (yes we’re serious). If the safest positions are interpersonal skill based and face to face, it means you want to be “eye candy”. Invest time into your appearance and throw away the elastic band supported clothing.

Dead Zone of Interpersonal Skills + AI Tools Knowledge

This we’re certain of at this point. If you live on X and are constantly looking at the latest and greatest, you feel far behind every 1-3 weeks. Despite implementing every single tool ands seeing revenues go up double digits you feel behind because a new item from Claude got released or a new funnel was discovered.

But guess what, you’re in the top 1% already if you understood all that and are paying attention!

eCom AI Playbook, February 2026 Edition

We’ve got CryptoMouse here with an update on E-com + AI integration. In addition we’ll have our own comments segmented out at the end.

Over the next year or two you’re going to see a new hybrid role at the vast majority of companies. Someone in charge of integrating AI tools and explaining them to people. In addition, a hybrid style AI tool explainer + sales teach in.

Both of those slots will be the new “middle manager” but they will be indispensable. You will get paid to stay on top of the AI tools + generate more revenue + test new products only available to major enterprises.

As usual, you can either accept new technology or complain about it on the internet hoping for a “return to the past”. Not hard to see which decision is right for you.

The saddest man in America is not going to be the poor person who never had a shot at escape. It’s going to be the people who spend like this will last forever, get displaced by AI and fumbles the ball at the one yard line.

You’ve got a golden ticket ahead even in W-2 land. Survive the round, become the go to guy for AI tools and you’ll end up with that paid off house + $3-4M to never worry about this stuff again.

The goal is freedom, not despair or spending due to psychological ego problems.

Part 4: Bonus Asset Side

We realize the spending habits of the upper middle/upper class W-2 worker may shock some of you. The reality will start to hit in the coming 6-9 months though. Instead of seeing a lot of extremely high paying slots of $500K to $1M? You’re going to see the majority of industries switch to a cap of around $300K-350K.

That looks about right to us as a typical high paid corporate worker at a place like Coca-Cola is going to make that type of money. There are only a few ultra rare seats that pay north of $500,000.

Think of a standard pyramid and make it a bit thinner. That’s what you’re looking at in the future.

You Have the Price Cap: If you take our $300,000 number at face value vs. the typical $500,000 high paid W-2 you can back into the products that this type of family would afford without absurd leverage. A single person on $300,000 is likely sticking to a townhome/well located condo. A person with a family would likely get to around $450,000 if we assume one person earns double (highly unlikely they earn the same)

This would net you to a max of a $2,000,000 home or so.

Now you have your rough line in the sand for luxury in the future. If someone is living in a place that requires them to earn north of $450,000 in combined income? It is likely a luxury area in that High cost of living region.

Why does this matter? It matters because any flip/fixer you decide to buy cannot go above that price point under any circumstances. Go through your neighborhood (we’re just doing HCOL for you) and figure out where the price per square foot breaks. Now you know where the maximum value is for that area to flip.

Since we know the majority of White Collar workers do not save significant amounts of money, you can back into what their decision making process will look like.

Again. You shouldn’t care about this as it pertains to your life. You should care about it as it pertains to how you invest and see your social circle evolve.

On that note, you’ll see a lot of these high cost of living blow ups in the next few months. You’ve got the rough math in front of you.

In addition to that, on a brighter note, next Monday we have an update from NOBs on what happens when you actually bet on yourself. You go from a simple e-com enterprise, to a larger e-com enterprise to… Big Time in Target and mainstream consciousnesses

There will be a fun competition in there as well so stay toon’d!

PS: Start that WiFi Biz Anon.

Disclaimer: None of this is to be deemed legal or financial advice of any kind. These are *opinions* written by an anonymous group of Ex-Wall Street Tech Bankers and software engineers who moved into affiliate marketing and e-commerce.

Old Books: Are available by clicking here for paid subs. Don’t support scammers selling our old stuff

How ETH is Staked: Covered (here)

Crypto: The DeFi Team built a full course on crypto that will get you up to speed (Click Here)

Crypto Taxes: We have a suggested Tax Partner and 25% discount code, for information see this post.

Security: Our official views on how to store Crypto correctly (Click Here)

Social Media: Check out our Instagram in case we get banned for lifestyle type stuff. Twitter will be for money