City Guide: Toronto and Another Take on Canada RE

Level 2: Value Investor

Welcome Avatar! As you know we’re heading into Winter soon and this is the perfect time to do the quick Toronto City Guide. Once again it is free so you can already guess the conclusion. Just in case someone enjoys pain, we’ve purposely waited until now. You’ll check the weather for Toronto in the Winter and immediately press the escape button. We’ve done you a favor anon.

Part 1: City Guide Toronto

There are really two big pluses: 1) the city is quite nice/clean compared to a large number of major cities, 2) there are a ton of sightseeing items if you ever get bored and 3) the food is on par with major cities in the USA. Outside of that, it’s “okay” to visit once but there is no chance we’d stay there particularly with New York City a stone’s throw away.

General Way the City Works

It’s pretty rough out there due to: 1) lower compensation compared to the USA - so we have heard, 2) higher relative tax rates - so we have heard and 3) what we know for sure - not great unless you’re a made man in his 30s… In which case, why would you live here? You’d leave.

On the first two points, we’ve only done basic checks on the comp packages and our understanding is that the numbers are lower and something closer to what people in Europe make. Not exactly great. For taxes, the tax rate goes to around 50% if you make over $250,000 a year (add the federal and province). Apparently, the capital gains tax is around 50% of your effective rate (so if you are paying 50% cap gains is 25% by our understanding)

Before moving on we’re using the phrase “as we understand it” because we’ve luckily avoided going to Canada for about 8-9 years now. Don’t even remember the last time to be honest. The reason for pointing this out is that it paints the following picture: terrible city living if young.

Need to be a Made Man: Usually we don’t start any city guide with the tax brackets but it was needed for this one. Canada is basically set up so that young people have a ridiculously hard time saving. Many are forced to live at home and the ones with good paying positions still don’t save all that much money. Some make it to the USA on some sort of Visa and the real sharp ones find a way to start a company and simply bolt entirely.

If you are well to do the city is actually fine. You just realize that the crowd will *generally* trend older. The only people really going out with money to spend tend to be in their 30s to 40s. The good news here is that the city is practically forced to have a wide range of dining options that are up to par for people with high incomes!

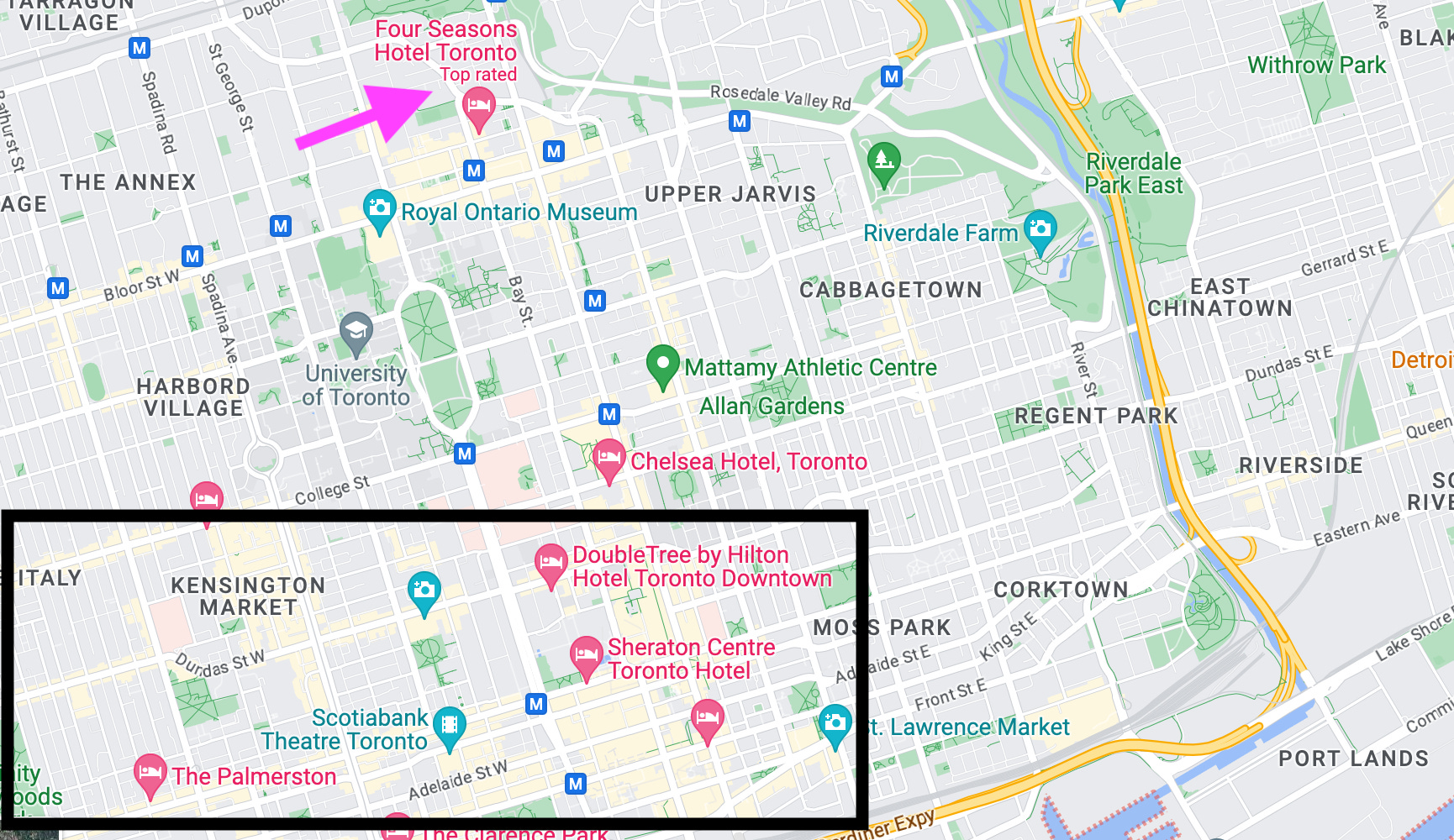

Quick Map

Generally speaking, if you’re going to go out at night (a ton) you want to be around this general area of the black square. Since the nightlife isn’t great you’re probably going to want to stick to something luxury and avoid the whole debacle in the first place (stay at the Four Seasons).

This section is the bottom left black square if you were to search for luxury bars/nightclubs etc. (No it’s not a perfect line up with the black square). Generally good enough.

Making the Best of It

One quick “tip” or “nugget” is that you’re better off meeting people at the restaurants. This is strange to an American who is used to go going to any venue and simply meeting people at the bar, club or lounge. If you’re going to dinners it’s actually pretty easy to talk to the people next to you.

This is pretty much your best option to avoiding a terrible night out.

Essentially (we’re guessing) the people going out to dinner do not have a plan to go out that night. Read that again. This is entirely different from the way the USA works. If you have a group out at dinner there is some 95% chance you’re going out to party, drink etc right after. This is why people have small amounts of food and then save some calories for inevitable bar hopping.

Toronto is Not the Same.

While there are exceptions to the rule, the trend is more likely: 1) just going out to dinner or 2) drinking with friends at some house/apartment and going out - save money by drinking a bunch at home first. (see economic overview at the start!)

If you’re able to figure this out, you can meet people at dinner with ease and when you say “sure we can all go out I got it covered no worries” it’ll be the easiest sale of your life. The problem is that even if you do have a great night, you’ll realize it just doesn’t compare to NYC, Miami or Dallas (not even close to be honest).

Better Solution: To make the best of it, just do the following: 1) make a decision to stay near the night-life or the 4 seasons, 2) check out the CN Tower, Royal Ontario Museum, the Art Gallery and maybe the hockey hall of fame since you’re in Canada after all and 3) really do serious vetting of the restaurants. Choose nice ones where it is not some sort of 5-course meal or extremely formal setting. You want a crowded spot and then hope things work. Go in the Spring!

Note: if you’re into nature items and want to see Niagra Falls then that is a completely different experience probably an 8/10 trip. Nothing really bad to say there. Just don’t think that’s enough of a draw to go all the way out there vs. many other natural beauties in the USA.

Conclusion

Yep that is really it. Zip in go for a weekend to see a few of the spots and zip out. You’ll realize that compared to NYC, Dallas and Miami it just doesn’t make any sense at all to be there. Perhaps if you’re into hockey there is another angle? Not sure on that front. Either way, make the most of it and you don’t need more than a weekend.

You’ll realize the nightlife is significantly older and begin to understand why income taxes on young people isn’t great! Good socioeconomic experiment our neighbors in Canada are having.

For Those Interested in The Better Cities Be Sure to Subscribe and Stay Toon’d

Part 2: Canada RE Update

The prior post (source) was not written by us. This section is *also* not written by us.

Another reader was pretty adamant about important points being missed so we’ll hand it over to BowTiedFullStack

BowTiedFullStack on Canada RE

First, thank you to Bull for the opportunity.

I’m not an expert, but I’ve been following Canadian RE closely for a while (will not elaborate).

Below, I’ll share what I’ve observed, primarily with a focus on Toronto and Vancouver markets. None of this is investment advice.

By the end, you should be able to come to more informed conclusions on the state of Canadian real estate.

Let’s dive in.

Scratch that, we’re talking about Canada, let’s go for a rip.

Brief Primer on Canada

Before jumping into real estate north of the 49th, let’s cover some basic context.

Keep these heuristics about Canada in mind:

~10% of the population of the US (38M vs 340M)

2nd largest country by land mass (only Russia is larger)

Over 70% of population lives within 100 miles of the US border

Over 80% of people live urban/suburban around big cities (Toronto, Vancouver, Montreal)

77% of Canadian trade is with the United States

The media stereotype of Canadians as perpetually apologizing, Tim Horton’s coffee drinking, hockey playing, igloo inhabiting, eskimos is dated. While still pushed hard by government propaganda, it falls flat.

Some argue that the Canadian identity, in practice, is simply “not American”.

Yet, when you look around the urban sprawl around Toronto, it sure looks a lot like an American suburb.

Cookie cutter 2200 sqft+ homes

Sprawling maze of neighbourhood roads

Strip malls

Poor public transit (vs Europe or Asia)

Crumbling infrastructure

Broad 6–12 lane highways

Rising property taxes

Extensive red tape for zoning and building codes

Generally center-left politics

You get the picture.

If you squint, most of the Canadian population lives a suburban, blue state, USA-lite existence.

Canadian RE up to 2010

Despite looking like the US in many ways, Canadian RE has taken a different path over the past 30 years.

Like the US, population growth in Canada has increased since liberalization of immigration laws in the 1970s.

Like Japan, Canadian RE last crashed in 1989–1991 when rates hiked into a recession. RE prices tanked 30% in Toronto and stayed down for the rest of the decade.

Unlike the US and Japan, since the bottom in 1996, Canadian RE has been on a nearly uninterrupted 30 year bull run.

Most Canadians have no memory of the 1989 crash.

Most Americans still remember the 2007 crash.

At this point, many if not most, of the home buyers today will not have even been alive or in Canada for the 1989 crash.

While the US saw an average price decline of 30% in 2007 and over a decade for prices to recover, Canada skated by with a 12% decline and 6 month recovery.

Then, rates went to 0%. The ZIRP party began.

Riding the Waves

There have been many long running trends impacting Canadian RE.

Below, those factors are split by whether they contribute to a bull or bear market. They are also tagged by whether they impact the demand or supply side.

If you can aggregate the weighted impact across all trends, and predict how they continue, you will have a good sense of where prices may go next.

Bull Factors

Demand: Extended ZIRP

Like most of the world’s central banks, the Bank of Canada followed the US Federal Reserve and kept interest rates between 0% and 2% from 2009 until 2022.

Mortgage rates fell from 5% in 2010 to under 2% during COVID.

Low rates saw increased demand from both families and investors.

Demand: RE as an Investment

Canadian company stock performance was dismal for the 2010s. The S&P/TSX 60 Canadian Index had a CAGR of 6.16% vs. the S&P 500 with a CAGR of 13.76%.

Instead of Canadian companies, many investors turned to real estate.

With low rates, investors could get stellar returns applying leverage to houses, apartments, condos, to rent or flip.

By 2022, over 25% of homebuyers were investors, and 20% of homes were owned by investors, often crowding out or pushing prices above what consumers could pay.

Demand: Foreign Investors

Real estate is a valued asset class for foreign nationals who want to stash their gains from abroad, out of the hands of their government.

Or for money laundering and other illicit purposes.

For example, foreign purchases of real estate in Canada, by just Chinese investors, reached 33% in Vancouver and 14% in Toronto in 2015.

Obviously, this is not unique to Chinese investors, and many other countries have private wealth ending up in Canadian RE.

This is a global trend. Foreign RE ownership in most major cities worldwide has increased in the past decade. Some parts of London, UK are now up to 9% foreign owned.

Yet, even pointing this out as a factor risks getting cancelled. Canadian state media has since 2015 reminded citizens that blaming rising prices on foreign investors is racist. (Is it?)

Governments at all levels, after denying its role for years, eventually took some action with vacancy taxes, temporary foreign purchase bans, and other measures announced from 2017 to 2023. Temporary price drops followed in some cities.

Notably, most measures retained large loopholes. Purchases now are slightly more difficult or costly, but still possible for foreign buyers.

Demand: Immigration

Canada’s legal immigration has generally increased annually since 1989, from 225k immigrants per year to over 400k in 2021.

The current government now targets 500k per year until 2025.

These numbers may not seem high. But remember, Canada has a population of 38m people.

By contrast, the US takes in 1m immigrants per year (2x Canada) with a population of 340m (10x Canada).

This translates to Canada having roughly 5x the immigration of the US, on a population adjusted basis.

All those immigrants need to live somewhere.

Demand: Foreign Students

Up from 275k in 2012, Canada took in over 800k foreign students in 2022.

The US in that same period accepted between 380k and 650k foreign students per year.

Adjusted for population, Canada takes in 19x more foreign students than the US.

All those students need to live somewhere.

And notably, some buy luxury cars and real estate, pushing demand higher.

Canada also makes it easy for students to transition from student visa to permanent residency (PR).

In many cases, rejected immigrants choose to go “back to school” and can gain a PR faster using a student visa, instead of waiting and re-applying for their PR.

This has contributed to net population growth much higher than the legal immigration quota.

Supply: Green Belt, Mountains

To prevent urban sprawl, Toronto has a strictly enforced “Green Belt” of farmland surrounding the city on all sides.

Vancouver is limited by the Rocky Mountains.

Montreal is on an island in the St. Lawrence River.

Whether by natural geography or regulated green space, Canada’s biggest cities have limited land to build on, contributing to limited supply.

Supply: Zoning, Regulation, Taxes, Rent Control

Canadian provinces (US readers: states) and cities have a myriad of layered zoning rules, regulation, and taxes which continue to limit what supply builders can profitably bring online.

Housing starts have remained roughly flat, fluctuating around 200k per year since 2000, while the population has grown 21% in that same period.

Rent control, slow landlord tenant boards, and other mandates on new buildings have also discouraged new apartment developers.

Supply: Running out of Labor to Build

Whether for commercial projects or even small job renovations, Canada’s construction labor market has grown increasingly tight with prices rising and delays mounting.

Even if more housing starts were approved by cities, the question remains: would there be enough labor to build?

Demand: Canadians Never Mail in the Keys

A visceral image from the US in 2007 was the homeowner mailing in their house keys to the bank for their underwater mortgage.

Statistically, Canadians do not mail in the keys.

Canada has dramatically lower mortgage delinquency compared to the US. While there are bankruptcy law differences, the bigger factor is a consumer mindset to keep their house at any cost.

From 2012 to 2023, US mortgage delinquency ranged from 1.72% to 10.45%.

In Canada, mortgage delinquency was 0.15% to 0.38%.

This translates to less selling pressure.

When times get tough, Canadians try to stick it out in their home for longer, taking on non-mortgage debt instead of mailing in their keys.

Demand: Government Incentives

Under the guise of “making housing more affordable”, governments at all levels have unleashed many incentives for homebuyers.

These incentives include:

RRSP HBP: withdrawing from your retirement portfolio

FHSA: investing tax-free for your house

Land transfer tax refunds

Primary residence capital gains tax exemption

A reduced downpayment scheme where the government takes equity in your house

As expected, this only shifted the demand curve. Affordability has remained dismal, but with higher prices.

Demand: Government Backstops for Mortgages

On top of incentives, the government and central bank backstop mortgages in many ways.

CMHC is the government run mortgage insurance agency. Any mortgage with a downpayment less than 20% is insured for a small premium.

CMHC also has a program where the government will cover part of your downpayment in exchange for equity in the house.

The Bank of Canada during COVID purchased over $9b in mortgage bonds to keep the mortgage securitization pipeline flowing.

Many more programs limit the mortgage risk to the “big five banks” (a government charter monopoly), reducing their skin in the game. Banks and B-tier lenders in recent years been reprimanded by regulators for the resulting overly loose lending practices.

Demand & Supply: COVID Measures

In response to COVID in 2020, Canada made numerous changes to Canadian RE markets, some still in effect, to protect borrowers and renters, at a cost to banks, CMHC, and landlords.

CERB: up to $8k stimulus cheques

Infinity mortgages instead of increasing mortgage payments

While preventing a collapse of demand, these policies, years after COVID and now under higher interest rates, are leaving Canada’s biggest banks with huge and growing losses.

Demand: Interest Rates Follow the US

The Bank of Canada sets interest rates, like the US Federal Reserve.

With 77% of exports going to the US, Canadian exporters rely on currency exchange rate stability.

So, regardless of what the Canadian economy is doing, you can generally bet that where President Powell goes with rates, Prime Minister Macklem will soon follow, in order to keep the exchange rate stable.

Demand: Currency Devaluation and Printing

The Bank of Canada has followed a similar playbook to the US Fed, monetizing government deficits with printing.

The federal deficit in 2019 was $20B. Since then, deficits surpassed $200B from COVID spending and continue at almost 4% of GDP.

In response, the central bank printed and bought government debt.

The money supply ballooned by 5x. Recent tightening has brought it down to 3x the 2019 baseline.

With 3x the dollars in circulation, asset price inflation, including in real estate, is an expected outcome.

Demand: Infinity Mortgages

Three of Canada’s five biggest bank have mortgage portfolios where 20%, over $130B of loans, have monthly payments that don’t even cover the interest.

Yes, that means infinity mortgages.

Borrowers with variable rate mortgages but fixed payments, soon had their payment entirely go to interest, and then their amortization rising.

Some borrowers have gone from 24 years remaining to over 90 years left in their mortgage.

Canada is much closer to the US in mortgage length expectations, unlike Europe where multi-generational mortgages are a more seriously considered concept.

90 year mortgages in Canada are not serious.

Like the US Fed propping up banks long past insolvency, many Canadian banks and borrowers are insolvent and at the mercy of current policy remaining in place.

If the Bank of Canada or regulators switch course, like they did in Japan to pop their bubble, a lot could unravel for banks and borrowers.

Until then, selling pressure is reduced as the central bank keeps the music playing.

Demand: Mortgage Fraud

There are increasing reports of mortgage fraud.

Real estate agents, B-tier lenders, and buyers have been caught in recent years bending income or government Mortgage Stress Test requirement to get mortgages approved.

For now, this has increased demand. Long term, those mortgages are likely at higher risk of selling or default.

Bear Factors

Demand: 5-Year Fixed Mortgages & High Rates

Unlike the US, Canada does not have a fixed 30-year mortgage product.

At best, borrowers can fix their rate for up to 5 years. Instead, many choose fully variable mortgages with rates updated monthly according to the central bank.

This means by 2026 if rates stay high, all borrowers will have renewed at higher rates than they’ve seen in 15 years.

Almost 2 years in, the pain continues to increase and it’s unclear when or if Canadians will crack.

On the other hand if rates drop, the pressure is off, and the party starts again.

Stagnant economy and wages

The Canadian economy is led by RE, which drives over half of GDP growth.

A country with bright future and thriving, innovative, diverse economy does not usually rely on RE as the top sector.

And Canada is no exception to that rule.

Productivity of the Canadian worker has consistently lagged the US by almost 30%. GDP per capita has been flat or down since 2016.

Brain drain to the US, especially in the tech sector, continues as Canadian wages remain low. The average IT worker makes $74k USD in Canada vs. $145k USD in San Francisco, $133k USD in NYC, or $117k USD in Denver.

Unfortunately, the lower wages don’t correspond to lower cost of living. Canadian cities like Vancouver, Toronto, and Hamilton have topped the least affordable cities in North America, worse than NYC or LA.

Government incentives to innovate have failed for decades to change the dreary performance.

The future of the Canadian economy does not look bright.

Demand: Immigration Slowing

While immigration quotas from the government remain at 500k per year, applications in 2023 were down 51% year over year, and 1 in 5 are considering leaving in Canada within 2 years.

Less immigration would reduce demand for housing.

Yet, even if immigration rates returned to 1989 levels of 250k per year, the cumulative backlog in housing starts could mean that the impact of this drop isn’t felt for many years.

Demand: Consumers Capitulate

This post has been data heavy.

If you want personal anecdotes, you can find them on Reddit: r/PersonalFinanceCanada, r/CanadaHousing, r/CanadaHousing2, and others.

Too many stories to read of over-leveraged max-pain hitting families.

Those not in the RE market, seethe that they can never buy if price and wage trends continue.

If consumers capitulate, selling at a loss or choosing to “lie flat” in despondency, prices could be impacted.

Real Estate in Canada: Today & Tomorrow

So, where does all of this leave Canadian RE today?

Depending on the city, prices dropped an average of 10.7% from the peak in May 2022.

Since the bottom in February 2023, prices have rebounded, now only 3% below ATH. Given the above trends still at play, who knows where prices will go from here.

As for me, I’ll keep chipping away at the walls of my W2 prison with a sharpened spork, inching closer to my escape, and sharing tactics so you can do the same.

Back to the cell.

Fullstack out.

BowTied Fullstackis on Substack, Twitter, Instagram, TikTok

Disclaimer: None of this is to be deemed legal or financial advice of any kind. These are *opinions* written by an anonymous group of Ex-Wall Street Tech Bankers and software engineers who moved into affiliate marketing and e-commerce. We’re an advisor for Synapse Protocol 2022-2024E.

Old Books: Are available by clicking here for paid subs. Don’t support scammers selling our old stuff

Crypto: The DeFi Team built a full course on crypto that will get you up to speed (Click Here)

Security: Our official views on how to store Crypto correctly (Click Here)

Social Media: Check out our Instagram in case we get banned for lifestyle type stuff. Twitter will be for money.

We have a saying on the east coast of Canada that more or less goes "Toronto is fun as long as you are continuously spending money". Will take going to Montreal 10 outa 10 times. Better food, better city, better people

Article hits the nail on the head. Need a hard crash in Canada or else there’s no future for most young people in the country, unless they’re smart enough to get out. Kudos to BTFullStack for the accurate write up.