Investing for Your Kids (Trump Account, 529, Basic Trusts) and Preventing Silver Spoon Vibes

Level 2 - Value Investor

Welcome Avatar! If you haven’t read our prior post on basic Tax Savings strategies you should. (Source)

This one will be a bit simpler and high level related to kids. In addition to that, you can actually use some of this if you’re an adult. So. We’ll just jump right in from kids to teenage to later work years.

Part 1: Trump Accounts

There is really nothing negative to say about these accounts. Left winged people will hate the name and that’s about it. If you can get a free $1,000 worth of the S&P 500 for your child, just click sign up.

This will not make your kids rich, it will not make them spoiled. Even if you invest $200 a month you’re probably looking at ~$100,000 when they turn 18.

What It Is Not For: This is not a 529 plan. It is not an account where education based expenses can be paid for tax free. Instead it is (in simple terms) an IRA that starts at age 0 and grows until they are 18. At this point the Child now decides what to do with it.

Good Summary But Note 10% penalty on 529 if not used for education.

Simplistically How to Use It

Since the absolute max is $5,000, assuming you can afford ~$416.67 a month, you just max it out. When the child turns 18 it is a traditional IRA anyway. This means you sit down and tell them “This is your pre-funded retirement account, don’t touch it unless extreme emergency. This allows you to take more risks and worry less about old age”.

Just max it out and forget it exists until the child turns 18. Only thing you should double check is the investment options. In general just dumping into the S&P 500 for 18 years is good enough.

For the Intense People

If you really want to get into the weeds. You could plan to roll this IRA into a ROTH IRA in the future. We’re not even sure what the rules will be in 18 years but we’re just making it up for now.

If this is allowed, you would set aside the taxes for that event. If you Have $100,000 in it and $40K is gains, then just assume that will be the amount taxed. You would then roll it, pay the tax and let it grow in a roth instead.

Since the Gain is not going to be millions of dollars, you can easily cover the tax bill with standard gift exclusion.

You send $19,000 to Jane/Jack and they roll it over. They take the $19,000 and pay the tax bill on the $40K of income they earned. Problem solved.

Final Note: No one can predict tax rates, retirement account rules or anything like that in 18 years. Just too difficult. Best to keep assumptions the same “It will just be a gifted IRA” and move on.

Part 2: 529 Education Plans

Every situation is different. If you’ve read us for a long time, you can imagine that we don’t think the 529 plan is as cool as others do. Why? We have our doubts related to the education system in general.

However, we’ll play ball and explain the way to maximize this.

The first rule is simple, you can roll over about $35,000 into a ROTH IRA completely tax and penalty free.

What This Means: Even if you have little faith in the education system (like us), it makes little sense to have less than $35,000 in the account by the time the child turn 18. If they decide to skip college and become your degenerate WiFi money protégé, they won’t need it.

That said, if you have $35,000 in the account with them as the beneficiary, you can just roll it over to a ROTH. Think of this as a small bonus on top of the IRA you build with the Trump accounts.

Small Money Planning: Since this would be much smaller, all you do is buy some boring bonds and line up the date to have $34,999 by the time the child is 18. Login, start transferring to the ROTH (Note: you’re subject to ROTH max limits, so you’d be clicking send $7K every year for five years)

TL;DR: This is what we’re planning. If you want to play the beneficiary game, you can do that as well which is below. For the majority baseline move is above, get it to $35K at 18 and move on. We’re treating it like another retirement account product.

If you are certain your child will need tons of education (trade, PHD programs, doctor, private K-12, etc.) then of course max it out. That’s the entire point of the product (tax free for education).

For Intense People

Many Beneficiaries: If you have a lot of kids or you want to play the beneficiary game, you can. This is where you slowly move the money out into various ROTH IRAs. The rule is you can move $35K per beneficiary. This means you could continue rolling down this money to grand kids.

Take a weird case where there is $100K in a 529. A child decides to have kids at age 22 after graduation. You know this is coming and simply move the beneficiary to their future two kids (just a simple example).

Private School: If you know that you’ll be using nothing but private schools then you would absolutely go wild for this. You can use the 529 plan for K-12. This means it is truly the best possible vehicle for education spending.

Life is messy so it’s hard to solve for exact education spending. Try to do your best to estimate and reduce your tax burden.

Certain on College: You’re sure that your child will need some wildly specific school/college for their unique talents, once again, max that thing out.

Super Fund: If you’re in this weird camp, you’d superfund it up to $95,000 once you know the bill is coming. Or. If life changes and you realize you will be paying for college this also applies. You can put up to $95,000 (today) with a super fund exemption. Usually the rule is $19K per person per year (gift tax rule), however, for this product you can put in 5x that amount.

Part 3: UTMA Accounts

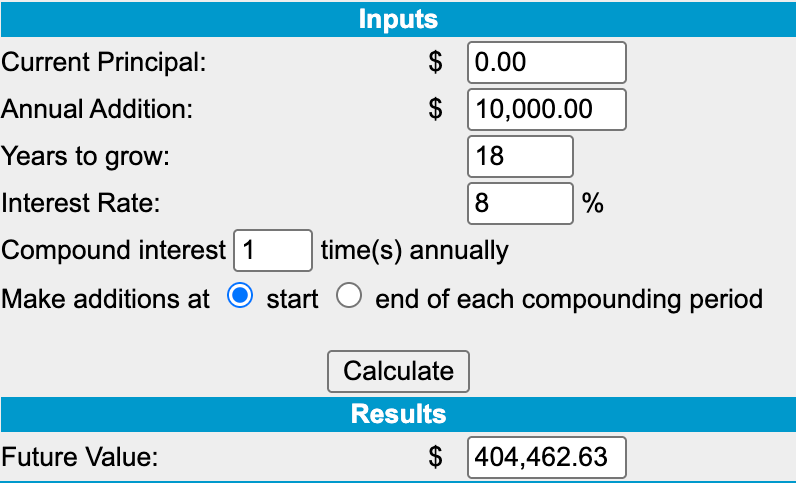

Ah yes finally something more real. This is basically a brokerage account for your kids. Keep it simple and say you put in $10,000 a year into it. You can just invest in whatever you like and let it grow. We’ll once again use some boring S&P rules.

At this point you can see the math we’re running. We assume the gift tax rule is $19K and stays there. We’re assuming you’re not married (if you’re married its $38,000) and you want to optimize it.

It would look as follows: 1) Trump account $5K, 2) ~$2K for 529 per year and 3) Remaining $10-12K to UTMA. Adds up to $19K. This a pretty good upper middle class saver set up. It means that when the Child turns 18 they will have: 1) ~$200,000 in IRA, 2) $35,000 in a Roth IRA and 3) ~$400,000 in a brokerage account. Sum total of $635,000 and can’t even legally drink!

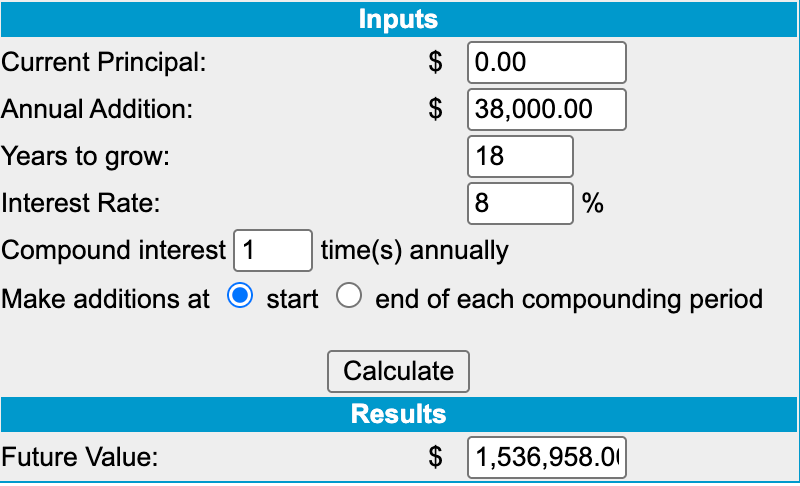

Hidden Problem with UTMA

Much like the 529 plan, unless you have as serious long-term plan with it, you might overfund it. You do not want it to grow exponentially to outrageous amounts of money. As an example take a married couple who maxes all $38K into the UTMA.

As you can see… this probably isn’t wise. Once the child turns 18 you have no access and it is entirely turned over (for the nitpickers 21 in some states but we’re keeping it simple as usual - source).

Quick Math: If inflation is 4% for 18 years, this means it will be worth half as much in 2044. Still ugly. Imagine handing $750,000+ to an 18 year old with no strings attached today. Wouldn’t end well.

To be clear on this. We’re happy to say the same thing about ourselves. At 18 if handed this type of money it would be non-stop nonsense and likely a death spiral of hedonism. Not great.

Summary

The simple set up is this: 1) max out the trump accounts have long convo about it being retirement only, 2) go up to $35K minimum for the 529, more only if you know you will spend it - don’t overfund in our opinion and 3) dance with the devil on how much you want the child to have at 18 years old in a brokerage.

Part of this game is psychological (beyond numbers on a screen). There is no guarantee you have grand kids. There is no guarantee your kid even goes to college or needs further education in 18 years. No one knows.

The best move is to typically max out the ideal benefits and move on. No different than our view of “401K plans”. You get the company match to the highest level and move on (typically 5% of whatever you make).

Part 4: Trust Planning Ideas

In the other post on tax strategies (source) we explained the basic mechanics. If you’ve gotten this far we’re pretty sure you already understand why gifting early to the trust is important. Instead we’re shifting now to esoteric trust fund “problems”

Jane and Jack: You have two kids who are fully funded with their Trump account, $35K Roth IRA money and make it up $100,000 in a brokerage account each (after inflation).

Since Jane and Jack are magically exactly 18 (fraternal twins). Both have their own talents and skills but 18-30 is a wild time of extreme changes. Many go off the rails, others become outrageously successful entrepreneurs.

How do you set up the trust correctly?

Step 1

If you’re wealthy, our basic opinion is you can give them either: 1) the down payment or 2) a basic 1bedroom condo in the city they will reside. This is a pretty fair deal. When you’re 21-29 trying to build businesses, rent is one of the biggest line items. If you can get rid of that, Jane and Jack will feel rich but it’s extremely hard to downward spiral off the savings. It’s possible but hard.

Step 2 - Contingent Distribution

If you’re still trying to get rid of money over time, you will need to set up standards and events to encourage good decisions. This is much more personal than it is a financial statement. Here are some ideas

If they have a child they instantly receive a percentage of the trust fund. Would cover all the baby items, some nursing help and all the chaos that comes with having a baby

You can do age based ones as well: 30, 35, 40, 45, 50. If you’ve done your research, you know that most Trust Funds are set up with a 35 year old cliff. We’re not sure why and don’t have anything for or against this arbitrary number. It’s an option

You can try to match salary increases or business success. If they want to become vets or doctors, you could add a 20% performance bonus on their annual salary for each year of completion. Basically encouragement for making good decisions

Annuity type trust, if you’ve learned that Jane and Jack don’t really save money you can give them an annuity. You covert the amount to a steady stream that never gets a sudden spike in wealth. IE. They get paid out $5,000 a month for 20 years instead of the lump sum

Write in an emergency contingency. Anything health related is instant access

Come up with something related to starting a business, if it is profitable and they need a loan, the trust can come in and keep the vultures out (outside money!)

Step 3 - Legacy

Basically Ego stuff. If you’re thinking beyond the kids and grand kids, you’re likely trying to play a bit of God. Life really doesn’t work like that. You can try to set up all these structures to set up 10+ generations of wealth.

In reality, there are too many changes to forecast 200+ years in the future.

We’ll definitely try. You’ll try. We’ll all fail. Good news is, none will be alive to see it happen!

On that note, go out there and start doing your math! Once you get past the 529 items, the questions get real serious. Enjoy the ride!

We’re always here to answer paid sub questions. As long as not abused we’ll be on the look out for anything related to these topics.

Disclaimer: None of this is to be deemed legal or financial advice of any kind. These are *opinions* written by an anonymous group of Ex-Wall Street Tech Bankers and software engineers who moved into affiliate marketing and e-commerce.

Old Books: Are available by clicking here for paid subs. Don’t support scammers selling our old stuff

How ETH is Staked: Covered (here)

Crypto: The DeFi Team built a full course on crypto that will get you up to speed (Click Here)

Crypto Taxes: We have a suggested Tax Partner and 25% discount code, for information see this post.

Security: Our official views on how to store Crypto correctly (Click Here)

Social Media: Check out our Instagram in case we get banned for lifestyle type stuff. Twitter will be for money