Why Rates Trend to Zero, Short E-com Note and Lifetime Subscriber Option Explained

Level 1 - NGMI

Welcome Avatar! We’re going to write out a simple explainer for why rates trend to zero long-term and why you should bet on governments printing money long-term. Please read that sentence closely. While rates can go up temporarily and printing can be paused temporarily, the long-term trend is quite different.

Part 1: Long-term Interest Rates Trend to Zero

Since the Fed is the topic du jour for 2023, we figured it would be a good time to explain *why* interest rates trend to zero. There is a reason why wealthy individuals are so hyped about the recent interest rate hike.

They (unlike most) recognize that the chances of rates being high forever is next to nothing. Over the long-term governments are forced to print and run lower interest rates due to debt burden. For that we’ll go ahead and explain starting with the annoying doomer debt clock.

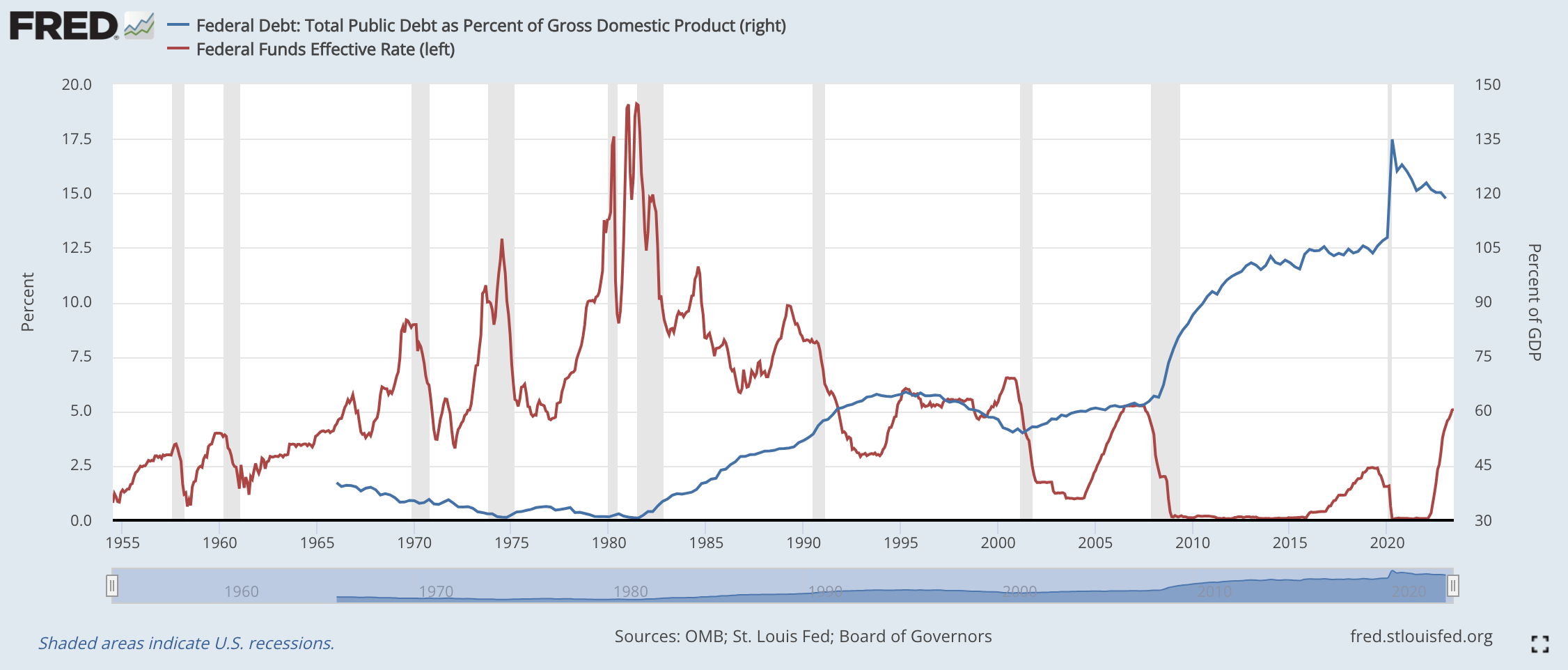

Classic Doomer Debt Clock Website

While doomers are losers, there is always a little bit of truth in what they are trying to convey. The truth is that the USA is racking up tons and tons of debt. Higher and higher over time as evidenced by the long-term Debt to GDP ratio.

While there are some dips (no doubt about that), the general trend is up and to the right. This is no different than you borrowing more money relative to how much you make. For example if you make $100,000 a year and borrow $20K, then $40K then $80K then $120K your ratio of $120K/$100K would match the USA at 120% debt to income (GDP).

What Does This Mean? No different than an individual. As you borrow more money, your interest outlay eats up more of your spending power. If you borrow $120K and only make $100K, with interest going from 5% to 10% that would be a $6K payment (6% of take home) vs. a $12K payment (12% of take home).

The government is no different. Interest rates trend down because we cannot balance a budget and constantly run a deficit. This means the income cannot keep up with spending. Just like your local Instagram flexer who can fit all their belongings into their $800 Gucci backpack but miss rent payments (no one rich wears a backpack daily)

Solution to the Trend

Note: Rates can be extremely high in the mid 1970s to early 1980s since debt to gdp was low at ~30%. It would be like having a 10% interest rate but you are only borrowing $60,000 when you make $200,000 a year. It wouldn’t impact you in a significant way

Pretty wild overlay here. As you can see in 2008-2009 when the banks were bailed out we had massive debt accumulation similar to COVID (percentage basis). This caused a decade long golden bull run in stocks unlikely anything we’ve really ever seen. Now we’re finally taking some medicine with rates spiking.

Unfortunately, we have a ton of debt so they needed to raise the debt ceiling to infinity for the next 2 years. (allows them to keep rates as high as they like for a couple years with no recourse)

Long-term: No real doubt about it. Governments will eventually print money. This is the only “solution to the trend”.

Interest rates have to go to zero eventually unless we find some sort of way to start paying down the debt (going from 135% to 120% debt to GDP is not enough if we’re increasing interest payments from 0-1% to 4-5%)

The second thing to realize is that the opportunity to make money in Bonds is extremely narrow. You have to jump on the chance since you know the peak interest rates will trend downward over time (ignore a particular quarter or month where rates are 0.25% above prior peaks, look at the bigger long-term trend of lower rates due to high debt load).

When rates get cut they get cut dramatically which leads to a spike in bond prices.

Creating a Framework to Avoid Historical Traps

1980s Back? Nope: In the 1980s the USA was experiencing incredible population growth which drives GDP up. If you have more people producing and consuming items, that naturally leads to GDP rising. Also. As you can see in the prior chart, debt to GDP at the time was 0%. This means no shot we get anywhere near 1980s rates or gdp growth comparable to that time frame since debt levels are massively higher and population growth is slowing (sadly dogs and cats can’t add to the GDP!)

Sudden Zero? Also unlikely. The only chance you’re suddenly going to zero in a single day? With a tail event like COVID. It is more likely that there is a single rate drop (say 1%) *after* unemployment has picked up. Can’t do it before. The risk of entrenching inflation like the 1970s is high if you cut before unemployment goes up

Lowering Rates is Not the Same as Printing $: They are not the same. If you print money it means a certain cohort gets the benefits. This could be COVID printing where we traded $1,200 for near double digit inflation. This could also represent the classic “government subsidies” for various innovations. So on and so forth

Lowering rates doesn’t do much immediately since it doesn’t mean that everyone qualifies. Money printing on the other hand is an instant injection.

Typically the only people who get extremely low rates are already wealthy with high incomes. Outside of COVID where they handed out 0% loans for free, the general trend is that a decline in rates would only benefit people who still qualify.

Most won’t qualify by the time interest rates get cut. As said more bluntly on twitter “Rates drop when you don’t have a job”. IE. won’t qualify when it happens

Big Picture Conclusion

Unless you have a strong and convincing reason that we will pay down debt aggressively, it means countries will move to lower interest rates long-term. This is due to the math behind higher debt loads and a goal of having some amount of inflation.

Having *small* inflation is generally healthy. At small amounts you encourage spending and economic growth/innovation since people won’t stuff money under a mattress knowing prices will be lower in 2-3 years

If you have a large net worth, it is best to avoid splitting hairs on small interest rate changes. If you can lock in enough to cover basic costs, go ahead and buy that 10-30 year. These pumps in rates are unsustainable if debt load remains the same. We might even go full Looney Tunes like Europe with negative rates in the future

You can ignore the full doomer scenario the debt clock guys pose. This is because the USA is the reserve currency for the foreseeable future. As long as that is the case, it will be difficult if not impossible to “go after the USA for a loan”. This is due to the massive defense and military budget

Governments have to resort to printing money. This makes inflation (long-term) the likely conclusion. Just don’t get caught swimming naked on the rare years when there is deflation due to a credit crunch. Also. Be sure to plug in a real expectation for what things will cost in 2053 since your 401K doesn’t reflect this (source)

Part 2: UPS Strike?

This is a bit of a last second note. We heard this rumor a week ago as well.

Ideally someone can comment here to confirm if it is true or not. If you’re shipping via UPS we would suggest switching providers for August (when there is smoke there is typically fire)

Since we’re not 100% sure on this, figured it would be worthwhile to put it in a free post to see if there is anyone who works at UPS (or close to UPS) commenting here.

Probability is actually quite high given the subscriber base we have.

As you know, if you’re slow at shipping or you are stuck in “out of stock” (for real) that means hundreds, thousands or even millions in lost profits that are unlikely recoverable.

We’re in an instant gratification world particularly due to the behemoth that is Amazon. At minimum, have a secondary option if a strike occurs so you don’t have to deal with the worst two words in E-commerce: Customer Service.

Part 3: Lifetime Option Explained

Here is how it works:

Lifetime subscription is $600 it goes up to $700 on May 1 to make sure we capture anyone who has been with us since the beginning at the 50% minimum discount price

We plan on writing through 2035 at minimum so that would be ~12 years or a ~50% discount assuming prices never go up

It’s a *one time* payment. However, Substack auto renews. All you have to do is click “don’t renew” at the end, we have your email saved so you’ll be set. Any issues just email us, we have the record for all transactions

Benefits of Lifetime

One time payment at 50% min discount with no more recurring

For the fun of it, we’ll give the first 25 people a copy of BowTiedBroke’s upcoming book on RE/Amazon and his general life (this will be released to the first 25 after he launches - not before to avoid piracy). As a guess this should be all set by end of today/tomorrow.UPDATE ALREADY HIT 25!Assuming we get around ~100 people (our estimate) we would use those 100 people to determine what to do with treasury funds we’ve built, ~$25K so far since incentives would be aligned. If we’re at a lower number than that we’d do a mix of asking them and polling the paid subs on any use of funds

Other Options

The other two options of $100/yr and $10/month are still around. No change

As stated there is no pressure at all, we’re just adding this since we got several people who prefer lump sum. It’s a reasonable request since some people don’t like recurring payments

Collect a Subscription For Free via BowTiedBum

As many of you know, BowTied Bum runs a credit card churn operation netting 6-figures. He has an outline on how to pick up the lifetime for free.

Once again, you don’t have to to any of this. This is not an affiliate link, just an option.

BowTiedBum Summary

There are two credit cards that will cover the entire cost of your $600 lifetime BowTiedBull membership. One business card and one personal card.

I highly recommend applying for the business card. For those unsure about applying for a business card, read the "What if I don’t have a business?" section here:

The business card I recommend is the Chase Ink Cash, which currently has a $750 signup bonus after hitting the minimum spend requirement in 3 months and has no annual fee.

The personal card I recommend right now is either the Chase Sapphire Preferred or Citi Premier Card which both currently have a $600 signup bonus and small annual fee. These are both great cards and highly profitable each year if you follow my methods. However, if you wish, you can downgrade either one to a no-annual fee card after one year to avoid paying an additional annual fee.

For those that don't know me. I have a Substack and Slack community that teaches newbies how to earn $10K+ WiFi money each year through credit card churning and manufactured spending. I offer a step-by-step plan that is broken down by each quarter, that anyone can simply follow along and earn money. I encourage everyone to ask questions in the Slack community to ensure their success, and no question is off limits.

Additionally, I have a guide that teaches you how to easily and quickly cover the cost of your yearly membership here

Good luck, and please feel free to DM me on Twitter with any questions!

Old Books: Are available by clicking here for paid subs. Don’t support scammers selling our old stuff

Crypto: The DeFi Team built a full course on crypto that will get you up to speed (Click Here)

Security: Our official views on how to store Crypto correctly (Click Here)

Social Media: Check out our Instagram in case we get banned for lifestyle type stuff. Twitter will be for money

Think of government spending like a credit cards.

Since revoking the gold standard in 1971, governments have been maxing out their cards, then opening new ones to pay off the old ones.

And unlike Bowtied bum, they aren't getting any reward points for churning!

Can comment on the UPS situation, it’s a vital aspect to my job for receiving product I sell. If the situation isn’t resolved by 11:59 pm 7/31 it’s going to get ugly.

Spoke to someone at UPS about it last week and they were optimistic for a solution to be reached this week.